Insight

CC&L Private Capital’s fourth-quarter financial market report and outlook

January 19, 2021

Markets overview

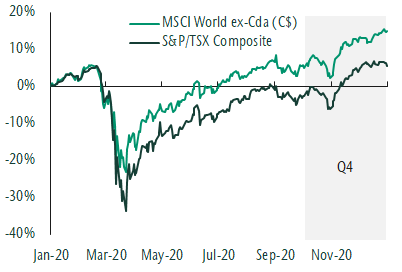

Equity market returns were strong this quarter as the global economy continued to show signs of healing in the face of rising virus cases and more shutdowns. The S&P/TSX Composite Index was up 9.0% and the MSCI World ex Canada Index (C$) advanced 8.8% this quarter. The start of November marked a significant inflection point for markets. The US election resulted in some short-term market volatility which subsided. This was followed by the clearly positive news of an approved COVID-19 vaccine. A better vaccine that is available to people faster than previously expected provides a boost to the economic outlook, even if it does take many months to distribute widely. This has allowed investors to look beyond near-term economic uncertainty to a more normal environment. A shift in market leadership followed as investors bought companies that were most negatively affected by lockdowns and stood to benefit the most from an eventual end of the pandemic. In addition, assets that are more sensitive to the economic cycle began to outperform. This includes cyclical sectors like energy and financials as well as asset classes like global small cap stocks.

Equity markets reach new highs in Q4

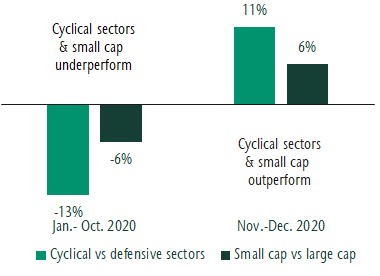

Significant shift in market leadership

Sector returns are for the MSCI World. Cyclical sectors include materials, energy, consumer discretionary, financials and real estate. Defensive sectors include consumer staples, health care and utilities. Small cap returns are based on the MSCI World Small Cap Index and large cap returns are for the MSCI World Index. All returns in Canadian dollars. Source: Refinitiv

Bond returns were mixed this quarter. Government and provincial bonds were modestly negative and corporate bonds generated positive returns. The net result was that the FTSE Canada Universe Bond Index returned 0.6% for the quarter. High yield bonds, like equities, benefited from an improved investor outlook. Despite default rates remaining elevated, demand for these investments has been strong and yields have tightened.

Our thoughts

We have been seeing a recovery in the economy unfolding for some time and have positioned portfolios accordingly. We have maintained an overweight to equities with a bias to global stocks. We have increased our weight to asset classes that tend to do well in a recovery such as small cap stocks. This quarter we sold core bonds and bought high yield bonds as credit conditions improved. This is consistent with the beginning of a new business cycle which historically coincides with improving returns for high yield.

Overall our equity teams continue to own resilient, stable businesses that have higher earnings growth than the market. Through the recovery we have selectively added more cyclical companies standing to benefit from an improving outlook and the start of a new business cycle. Within Canada this means increasing exposure to banks and energy companies. Within our global strategy we remain overweight emerging markets and have reduced the underweight to financials and increased positioning in select leisure companies. Within fixed income we are overweight credit and inflation-protected debt. Our positioning has benefited clients well this quarter and year.

From the desk of Jeff Guise, Managing Director, Chief Investment Officer, CC&L Private Capital.

This post is for information only and is not intended as investment advice. The views expressed are those of the author at the time of publication and are subject to change at any time.