Commentaires

Steady drip feed of policy support continues in China

13 septembre 2023

Summary

- The MSCI EM Index was down -6.13% in US$ terms for August, led by a negative month for Chinese equities.

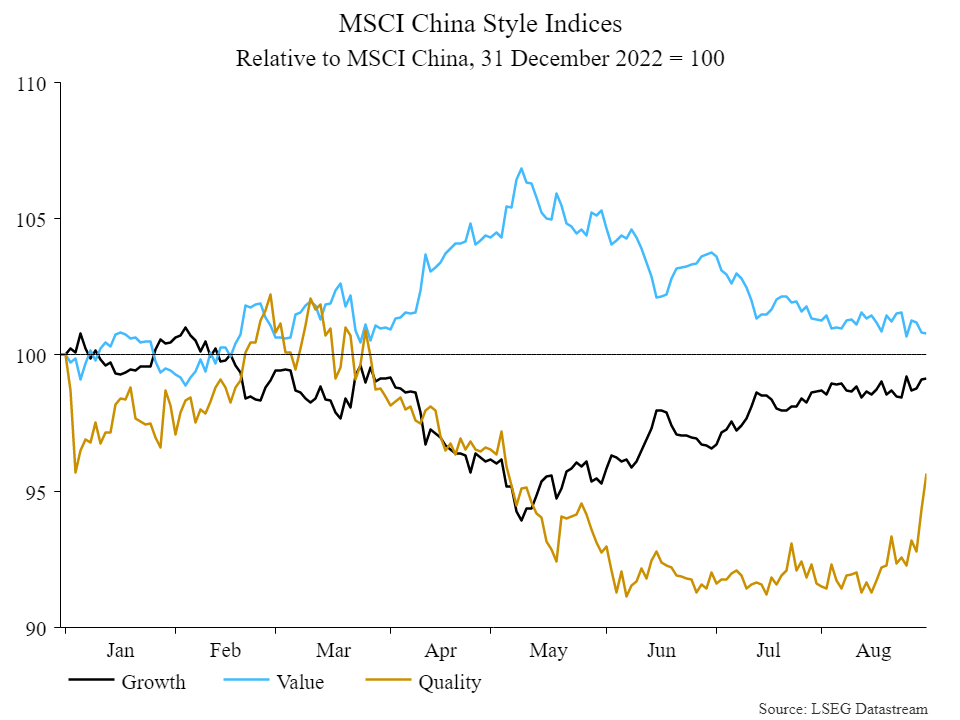

- Stock picking in China was positive for the portfolio, as value stocks in China pulled back and quality stocks bounced following a run of poor performance through most of 2023 (chart below).

- The Materials sector had a down month on softer economic data globally, reflected in the performance of markets with heavy exposure to commodities, including Brazil, Chile and South Africa.

- Tech in Korea and Taiwan cooled following a strong run in 2023, fuelled by surging sentiment for AI.

India’s moon landing marks its rise

Stock picking in India was again a contributor for the portfolio, with our Indian equities flat over the month (MSCI India down nearly -2%). India celebrated a successful landing on the moon, a marker of the country’s rapid ascension – it’s the first nation to land a rover to explore the moon’s southern polar region (and on a budget of less than US$74 million). Just days earlier, Russia failed in a similar attempt.

Does BRICS+ matter?

The 15th BRICS summit took place this month, with Russia’s Putin notably absent. As a member of the International Criminal Court (ICC), South Africa would have theoretically been required to arrest Putin over ICC accusations of Russia’s alleged deportation of Ukrainian children.

The concept of the BRICS was expanded with the inclusion of Saudi Arabia, Iran, Ethiopia, Egypt, Argentina and UAE. While the idea of a body to represent and promote the interests of the “global south” is logical, some claims of what this group can achieve are wildly overstated.

Indeed, calls that this meeting marks a coherent challenge to Western predominance of international relations is overstated given the divergent economic and political interests of member states. Of the core members, only the giants China and India – strategic competitors and at times outright adversaries – offer meaningful economic and political heft to the group, while Russia, Brazil and South Africa have all gone backwards since former Goldman analyst Jim O’Neil coined the term “BRICS” in 2001. The introduction of a number of states with equally divergent views risks making the BRICS concept even more amorphous.

Early signs of recovery in China’s quality stocks

Our decision to lift portfolio exposure to a modest overweight in China last year as the economy reopened favoured higher-quality names. This reflected the view that China’s reopening would not be a V-shaped boom like what we saw in the West. Money numbers were positive and better than the rest of the world, but not especially strong in absolute terms. The authorities had also refrained from turning on the fiscal and monetary taps through lockdowns and reopening for fear of sparking the inflationary boom we have experienced in the West. Hence, we added primarily to high-quality names with robust and sustainable returns on capital as opposed to more cyclically geared stocks, given the likelihood this recovery would be fragile.

However, as the chart below illustrates, it is quality in China which has been abandoned by foreign investors over the past year. Despite the majority of our holdings posting solid results through the period, investor fears over economic malaise in China and further deterioration of Sino-US tensions saw investors sell indiscriminately as it became clear China’s path to recovery would not be so straightforward.

The chart also illustrates the divergence between performance of quality and value stocks in China, which became particularly stretched in Q2. Their outperformance since early April appears to coincide with the announcement of an SOE reform drive. Beijing is launching yet another push (one of dozens going back decades to Deng Xiaoping’s time as leader) that aims to boost the sub-par returns of these often bloated and highly inefficient companies.

In the absence of other positive stories in China, momentum-oriented domestic mutual fund managers piled into SOE stocks. While this was difficult from the perspective of relative performance for the strategy, we remain happy holders of some very strong franchises that have been posting robust results and now trade at very attractive valuations. In addition, we remain sceptical that the latest reform drive for SOEs will close the wide productivity gap between state firms and private enterprises in any meaningful way.

We remain focused on owning businesses with high returns on invested capital, low debt and management aligned with minority shareholders. This is especially important in the testing economic environment that China is in today. Our businesses should be well-positioned to weather a soft economy, while SOEs inevitably face the risk of being called up for national service by Beijing.

While only over a very short period, it was pleasing to see quality stocks in China bounce sharply in August as policies supporting the economy continue to trickle through.

Steady drip feed of policy support continues in China

Last month’s commentary covered Beijing’s slow and reactive economic management, while noting signs that authorities are steadily getting a policy response into gear. Investors running for the exits may find themselves whipsawed back into China should authorities accept economic reality and act decisively. For us, while sentiment and news flow are undoubtedly poor, we remain focused on the alpha opportunity that lies between expectations and reality. A shift in the narrative from dire to very bad could be enough to spark a rally given how badly beaten up Chinese equities have been this year.

With this in mind, policy trends through the month were positive (although not exactly decisive) in August:

- It appears that property stimulus is gathering steam on the demand side, with the PBoC lowering the minimum down-payment ratio for first and second-time homebuyers to 20%/30%, respectively.

- The PBoC also cut key policy rates for the second time in three months, which appears to support our analysis that authorities are acting to reverse their misguided policy tightening in late 2022 and early 2023.

- This is translating into lower rates for home loans and should provide some support to the property sector – will this help tier 1 city transactions pick up more meaningfully and move the needle for homebuyer sentiment?

- Providing some support on the supply side (i.e. struggling private property developers like Country Garden) would also help to shore up confidence, but we are yet to hear anything concrete.

- The State Council announced increases in personal income tax deductions for infant and children’s education and elderly care, to help ease the cost of living burden for the middle class.

None of these measures are the policy bazooka that we think can draw a line under China’s slump, but the direction of travel is positive and additional measures to address local debt challenges and ease fiscal policy should emerge in the coming months.

Thailand’s Move Forward blocked from forming government

Former real estate mogul and Pheu Thai party member, Sretta Thavisin, was sworn in as Thailand’s prime minister, having formed a 10-party coalition which includes several pro-military leaders that were previously rivals of the party. The confirmation comes hours after ousted PM and the founder of Pheu Thai’s precursor party, Thaksin Shinawatra, returned to Thailand following a 15-year exile, having fled corruption charges that have now been watered down by the monarchy.

This follows the parliament’s failure to confirm Move Forward’s leader, Pita Limjaroenrat, as the new PM in July. Despite having won the election in May, Limjaroenrat’s confirmation bid to become PM was rejected twice by parliament, driven by opposition to Move Forward’s proposal to reform laws banning criticism of the monarchy. Thaksin’s return appears to signal that a deal has been done with the monarchy to keep Move Forward out of power.