L’argent, le moteur des marchés

What would the historical Fed do?

11 juillet 2024 par Simon Ward

An analysis of the Fed’s historical behaviour suggests that the conditions for policy easing are in place.

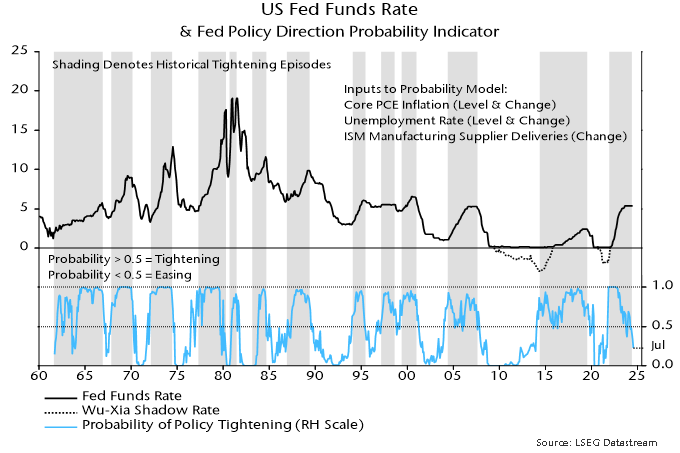

Chart 1 shows the fitted values and current prediction of a logit probability model for classifying months according to whether the Fed is in policy-tightening or policy-easing mode.

Chart 1

The model’s determination for a particular month depends on values of annual core PCE inflation, the unemployment rate and the ISM manufacturing delivery delays index known at the end of the first week of the month (i.e. after the release of the employment report for the prior month).

The model can be thought of as an approximation of the Fed’s “average” reaction function over the last 60+ years. It correctly classifies 87% of months over this period, i.e. the estimated probability of being in policy-tightening mode was above 0.5 in tightening months and below 0.5 in easing months.

There is no memory effect – the model ignores whether the Fed was in tightening / easing mode in the previous month, only considering the above data series (with no dummy variables for “shocks”).

The dependent variable takes the value 1 from the month of the first rate increase in a tightening phase until the month before the first cut in a subsequent easing phase, and 0 otherwise. So a rate plateau before an easing is still classified as part of a tightening phase (and a rate floor before the first hike part of an easing phase).

The tightening / easing phases were identified judgementally and are shown by the shaded / unshaded areas in the chart. The Wu-Xia shadow rate informs the dating of phases during zero-rate periods since the GFC.

The model estimates the probability of the Fed being in tightening mode this month (July 2024) at 0.23, the lowest value since September 2021. Equivalently, the probability of a start of an easing phase is 0.77.

A fall in the tightening probability from 0.62 in March reflects a 0.2 pp rise in the unemployment rate over the last four months (from 3.9% to 4.1%) and a 0.3 pp fall in annual core PCE inflation (from 2.9% to 2.6%).

The Fed is unlikely to announce a rate cut at the conclusion of its next meeting on 31 July, as this would be at odds with recent communications (although the probability may be higher than the 0.05 implied by market pricing on 11 July, according to CME FedWatch).

The model’s shift, however, suggests a strong chance of a dovish statement teeing up a September move.