L’argent, le moteur des marchés

US deposit distortion confirmed

11 février 2026 par Simon Ward

US demand deposits surged by 17% between October and December. A previous post argued that this was likely to reflect a reporting change, rather than a flow of money between accounts. The Fed’s Public Affairs office has confirmed this interpretation in response to a query:

“The large swings in demand deposits and other liquid deposits in November and December 2025 on the H.6 were due to a reclassification of deposits.”

The reclassification has not affected the official M1 and M2 aggregates, which include both deposit categories. It has, however, distorted the M1A measure tracked here – comprising currency in circulation and demand deposits – as well as narrow money indicators constructed by other analysts.

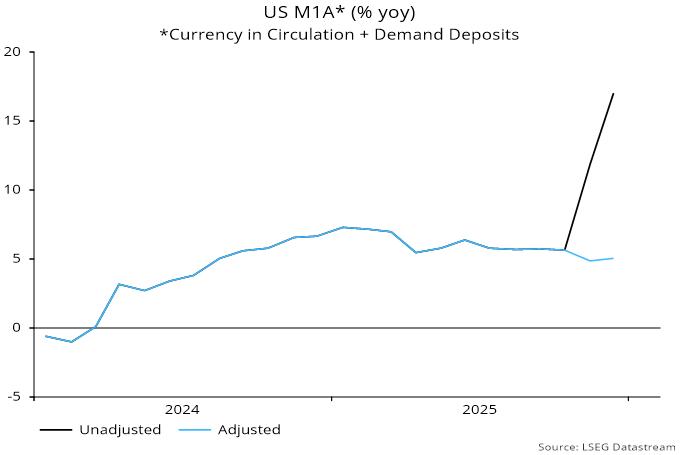

The procedure adopted here has been to “correct” the M1A numbers by assuming that growth of demand deposits in November and December would have equalled that of total liquid deposits in the absence of the distortion. Chart 1 compares annual growth rates of the unadjusted and adjusted series.

Chart 1

Claims have been circulating that US narrow money growth surged into end-2025, feeding narratives of excess liquidity and dollar debasement. Such claims appear not to account for the deposit data distortion and should be discounted.