L’argent, le moteur des marchés

UK money update: corporate liquidity squeeze

10 décembre 2024 par Simon Ward

Monthly UK money growth was boosted by households scrambling to dispose of assets ahead of the Budget, with a reversal likely and corporate liquidity trends worryingly weak.

The narrow and broad money measures tracked here – non-financial M1 / M4 – rose by 0.9% in October, in both cases representing the largest monthly increase since 2021, when the Bank of England was still conducting QE.

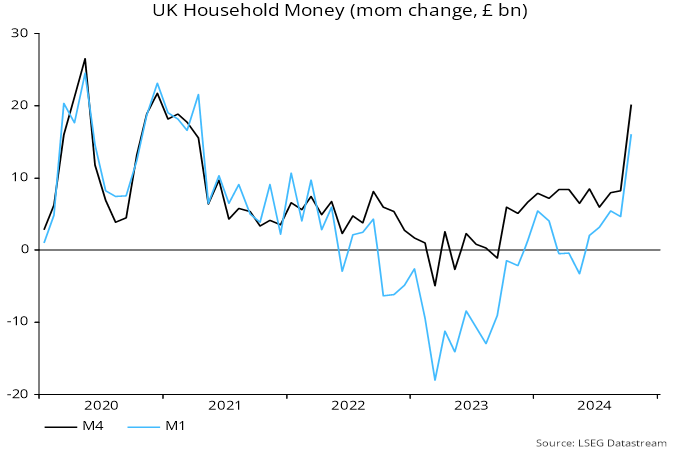

Strength was focused on the household sector, with a monthly rise in M4 holdings of £20.2 billion (1.1%) versus a £7.6 billion average over the previous half-year – see chart 1.

Chart 1

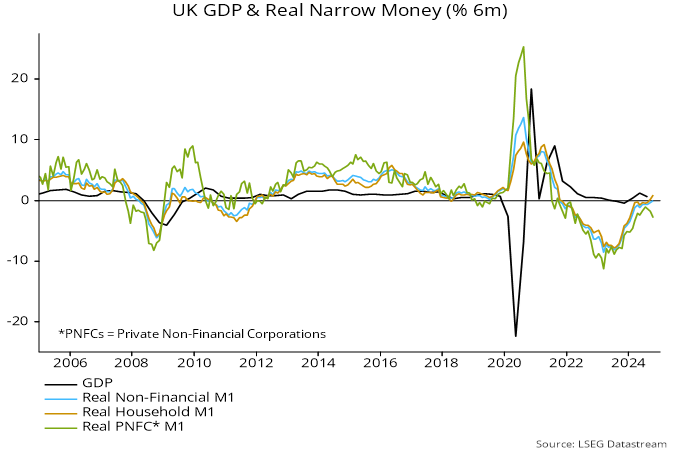

Six-month momentum of household real narrow money, which had edged into positive territory in September, rose to a three-year high. Corporate real narrow money momentum, by contrast, was the most negative since March, suggesting that firms were facing a financial squeeze before the Budget national insurance grab – chart 2.

Chart 2

Corporate broad money holdings contracted at a 1.7% annualised in nominal terms in the six months to October, while M4 lending to the sector grew by 5.6%. The corporate liquidity ratio, therefore, fell at a 6.9% pace.

Households crystallised capital gains, accelerated property transactions and withdrew cash from pension funds to avoid mooted Budget tax hikes. Retail savers sold £5.9 billion of investment funds in October, the most since September 2022, according to the Investment Association. The number of residential property transactions rose by 10% on the month, with non-residential deals jumping 40% to a record.

An increase in asset turnover has no monetary impact where transactions are between UK residents and involve offsetting changes in the bank balances of buyers / sellers. A monetary boost occurs when UK-owned assets are sold to overseas residents and / or when transactions are associated with an increase in bank lending.

Non-financial M4 lending (i.e. to households and private non-financial corporations) rose by £7.2 billion in October versus a prior six-month average of £4.1 billion.

UK buyers of assets, moreover, may have made room for purchases by reducing demand for gilts, requiring an offsetting rise in bank lending to the public sector. Gilt sales to the UK non-bank private sector slowed to £6.1 billion in October versus a prior six-month average of £12.3 billion. The credit counterparts analysis shows a positive public sector contribution to the change in M4 of £11.0 billion (0.4%).

Sales of assets to overseas investors, meanwhile, may have been significant, judging from a £9.1 billion monthly fall in non-resident net sterling deposits.

Sellers of assets for tax reasons are unlikely to wish to retain permanently higher money balances. “Excess” funds may be used to repay bank lending, increase gilt purchases and buy assets from non-residents, resulting in a reversal of the monetary boost.

The suggestion is that the pick-up in household money momentum should be discounted, with greater weight given to deteriorating corporate trends.