L’argent, le moteur des marchés

Surprising January monetary news

25 février 2026 par Simon Ward

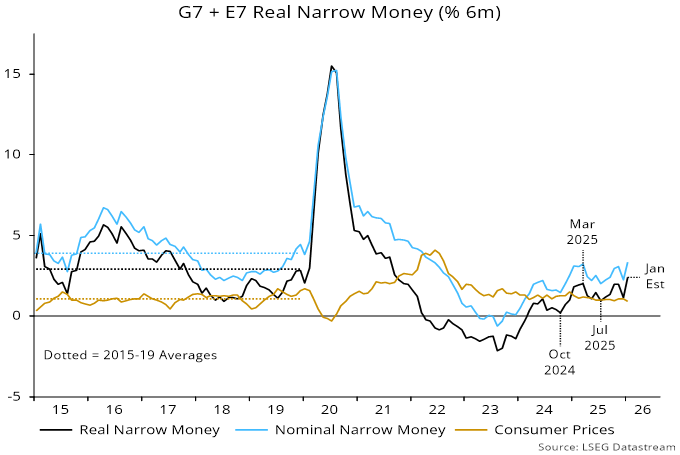

Global six-month real narrow money momentum is estimated to have rebounded from a sharp December fall to reach a new high in January, based on monetary data covering three-quarters of the G7 plus E7 aggregate tracked here – see chart 1.

Chart 1

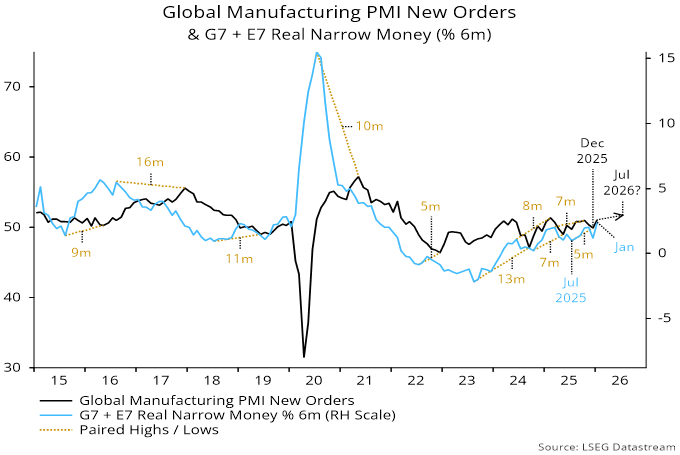

The December drop was the basis for an earlier forecast that a rise in global manufacturing PMI new orders would fizzle out in Q2, with a relapse into Q3. The January monetary news suggests that the current upswing will be sustained into H2 – chart 2.

Chart 2

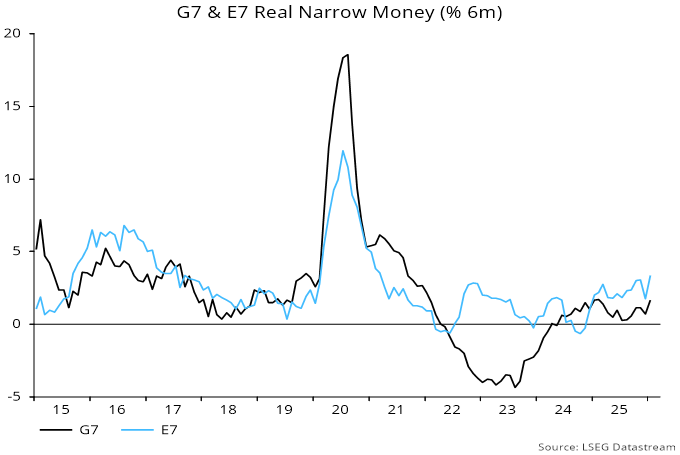

Both G7 and E7 components contributed to the January rise in real money momentum, but the G7 series is estimated to have remained below a February 2025 peak, whereas E7 momentum reached a new high – chart 3.

Chart 3

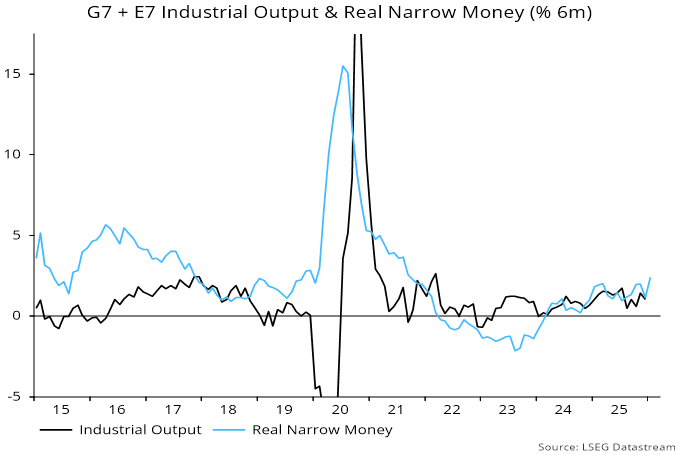

The rebound in global real money growth has likely restored a positive differential with industrial output momentum, suggesting “excess” money support for markets – chart 4.

Chart 4

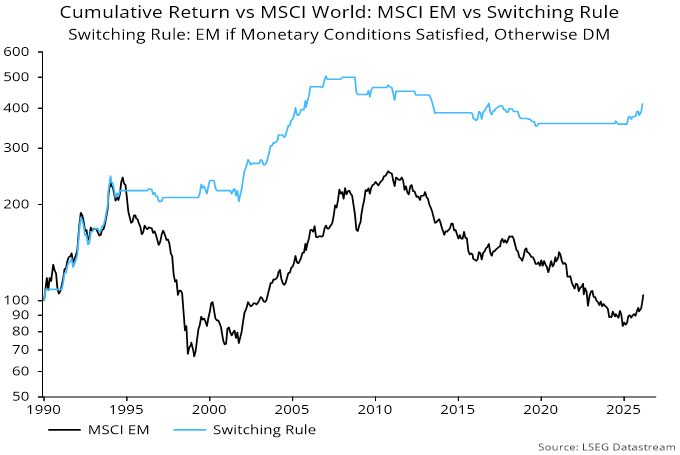

Previous posts noted that EM equities outperformed DM on average historically in months following positive readings of this differential and the E7 / G7 real money growth gap (allowing for reporting lags). The joint condition was in place in nine of the last 12 months. Chart 5 shows the performance of a monthly switching rule that prefers EM only when the joint condition is satisfied, otherwise reverting to DM. The latest news implies that the rule will continue to favour EM in March and, probably, April.

Chart 5