L’argent, le moteur des marchés

Rising Eurozone recession risk

29 avril 2026 par Simon Ward

The April bank lending survey signals an “endogenous” tightening of monetary conditions, which the ECB should – but won’t – offset with policy easing.

A previous post suggested that the Gulf War III shock would interact with concerns about private credit exposure to cause banks to tighten lending standards. April Fed and ECB lending surveys were flagged as important markers.

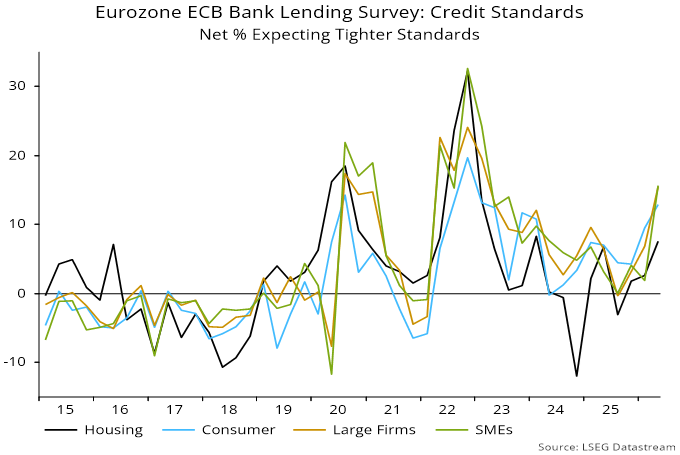

The ECB survey confirms the thesis, showing significant rises in reported and expected credit tightening balances across loan categories – see chart 1. (The Fed survey is expected next week.)

Chart 1

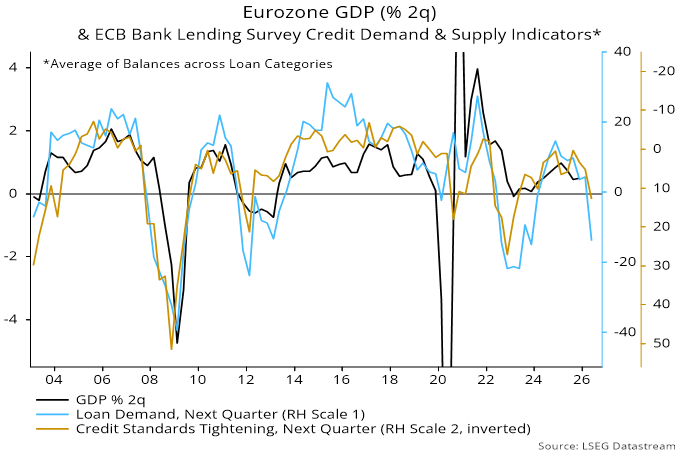

The shock, however, appears to have had an even greater negative impact on the risk appetite of borrowers. An average of expected demand balances fell to a level historically consistent with GDP contraction – chart 2.

Chart 2

With both supply and demand weakening, loan growth may slow sharply, in turn threatening a fall in meagre broad money expansion. Non-financial M3 rose by only 3.3% in the year to March.

Prospective monetary weakness argues for pre-emptive policy loosening but the ECB, following new Keynesian convention, is focused on upside risk to inflation expectations. Expectations measures, unlike money trends, failed to give timely warning of the 2021-22 inflation surge, contributing to policies remaining excessively loose. An opposite mistake may be brewing.