L’argent, le moteur des marchés

Misplaced ISM optimism

11 mars 2026 par Simon Ward

A rise in the ISM manufacturing new orders index was expected to be short-lived even before the outbreak of Gulf War III.

The index jumped from 47.4 in December to 57.1 in January, with a small retreat to 55.8 in February. The January reading was the strongest since 2022.

The ISM rise, along with a parallel increase in global manufacturing PMI new orders, boosted hopes of a sustained industrial upswing with an associated earnings-driven broadening of equity market gains.

The interpretation here, by contrast, has been that the ISM / PMI rises reflect the global stockbuilding cycle moving into a peak. The cycle was expected to begin a downswing by mid-2026 into a H1 2027 low.

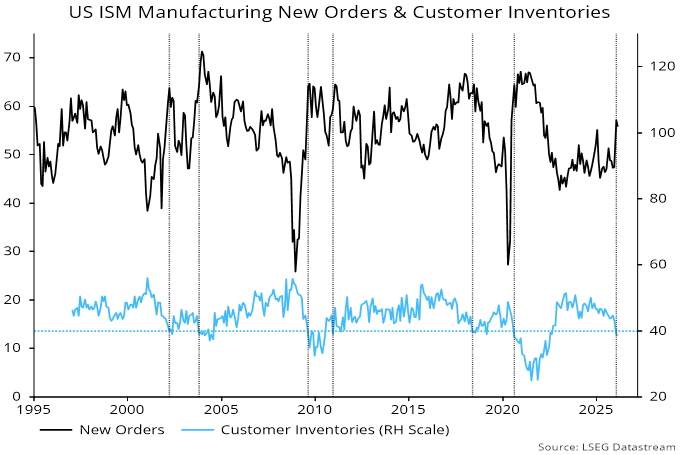

The ISM customer inventories index supports this interpretation. The jump in new orders has been accompanied by a sharp fall in customer inventories to below 40. Previous declines to sub-40 occurred around peaks in new orders – see chart 1.

Chart 1

This seems, on first consideration, perverse. The customer inventories index is a gauge of whether stock levels are too high or low. Falling / low readings might be expected to signal future restocking, resulting in a rise in new orders.

The explanation for the opposite relationship is that, by the time they report lower inventories, customers are already placing restocking orders, i.e. the additional demand is reflected in current not future new orders. The next phase of the cycle involves customers reducing demand as inventories return to a comfortable level. This phase marks the new orders peak.

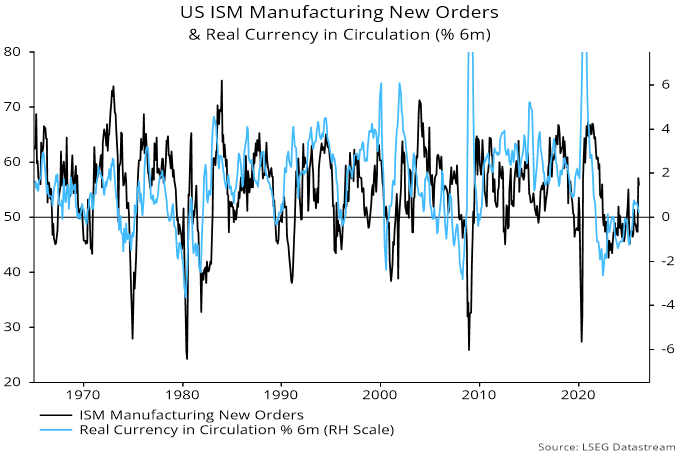

An imminent ISM new orders reversal is also implied by a recent decline in six-month growth of real currency in circulation, which has led the orders index by an average eight months historically and peaked most recently in August – chart 2.

Chart 2

The suggested explanation for this relationship is that currency demand is influenced by retail spending plans, with such spending driving orders placed by retailers / wholesalers. The currency slowdown may indicate that spending prospects were deteriorating before the energy price shock.