Commentaires

LatAm’s rightward political shift is fuelling a continent-wide bull market

13 janvier 2026

Venezuela and the arrival of the “Donroe Doctrine”

Trump gunboat diplomacy in the Caribbean has culminated in the seizure of Venezuelan leader Nicolás Maduro on January 3, 2026. The move has been widely touted as part of a revived Monroe-style foreign policy doctrine in the United States which aims to assert regional hegemony by shaping political trajectories through the region.

More muscular regional foreign policy from the United States under President Trump reinforces a rightward political shift across the region. Economic instability, corruption and crime have been the fuel for voters to favour conservative and far right candidates in elections across Argentina, Bolivia, Chile, El Salvador and Honduras. The United States has signalled in recent months that it is prepared to strengthen the hand of conservative political actors aligned with its strategic aims (e.g., the US Treasury’s $20 billion currency swap line with Argentina’s central bank).

Maduro’s capture sends a clear message – particularly to Latin America’s left-wing politicians – with respect to the lengths to which Washington will go to protect its economic, geopolitical, security and ideological interests in the region.

The rise of economic conservatism with a backstop from the United States has already stoked optimism in regional equity markets on hopes for pro-business reforms, deregulation and fiscal discipline. While LatAm’s equities markets were buoyant in 2025, we think there is potential for positive momentum to pick up as the continent embraces fiscal conservatism.

As we have written previously, Brazil remains the largest market that can move the dial for EM equities should voters go with an economic moderate over incumbent President Lula in this year’s presidential elections. Below, our LatAm portfolio manager Luis Alves de Lima provides an update on prospects for the market.

Will Brazil be the next domino to fall in LatAm’s shift to the political right?

With the FIFA World Cup and presidential elections looming, 2026 shapes up as a big year for Brazil. While my Brazilian compatriots and I remain as passionate as ever about football, I think that politics is poised to steal the spotlight from the pitch.

In my view, the « Hexa » (Brazil’s longed-for sixth World Cup win) remains a distant national dream reflected in rather long odds among the bookmakers. The better bet is for a market-friendly political shift and subsequent bull market in Brazilian stocks.

However, it would be foolhardy to call time on a political operator as wily as Lula da Silva. We have written in previous commentaries about the potential for a conservative moderate such as Sao Paolo governor Tarcísio de Freitas to win the presidency. He remains the markets’ preferred candidate, being a technical, pro-market leader capable of bridging the gap between the Bolsonarista base and the moderate right. However, recent data from the December 2025 Quaest polls suggests a more complex reality.

Senator Flávio Bolsonaro, the son of the former president Jair Bolsonaro (now in prison for a botched coup attempt), has reached parity with Tarcísio in presidential vote runoff simulations, both trailing President Lula in a 46% to 36% split. This shift has emboldened the Bolsonaro family to prioritize their own political legacy, seeing an opportunity for Flavio to inherit the mantle of right-wing standard-bearer rather than coalesce around a moderate more likely to garner wider public support.

Critically, and much to the consternation of investors, Governor Tarcísio has said he will not run for president if Flávio Bolsonaro maintains his candidacy. Driven by a deeply held sense of loyalty and a desire to avoid fracturing the conservative base, Tarcísio has essentially signalled that he will remain in São Paulo if the « heir apparent » proceeds.

This is the worst-case scenario and would leave voters with a choice between two populists who feed on political polarisation. President Lula would welcome the prospect of Flávio’s candidacy, where he can home his narrative for the candidacy in on the threat to institutions of a Bolsonaro presidency.

Political sands will continue to shift as 2026 unfolds

These recent developments are no doubt a knock to the short-term bull case to Brazilian equities. However, getting overly fixated on this « nightmare scenario » would be a mistake. The field is deeper than current headlines suggest.

Even if Flávio remains the standard-bearer for now, there is potential for alternative candidates to grow in the polls should the electorate favour administrative results over populist chaos.

Figures like Governor Ratinho Júnior (Paraná) and Governor Romeu Zema (Minas Gerais) have built formidable reputations for fiscal discipline and efficiency.

The emergence of Renan Santos and the MBL’s « Missão » party represent a youth-driven movement prioritising fiscal conservatism, anti-corruption and law and order, which could disrupt the duopoly between Lula’s PT party and the Bolsonarismo right as we approach the March 2026 deadline for candidate clarity.

Market implications

There are two primary reasons for constructive optimism in thinking about the outlook for Brazilian stocks:

First, Brazil is not an island; it is part of a decisive continental swing to the right. In December, we saw José Antonio Kast’s victory in Chile, this on the back of President Javier Milei’s strong showing in Argentinian legislative elections, and recent conservative momentum in Ecuador.

This regional « blue tide » creates a powerful tailwind for market-friendly policies, and we argue that this will place some moderating pressure on Brazil’s political elite.

As its neighbours demonstrate the success of radical deregulation, the appetite for a « rational right » candidate in Brazil will only strengthen.

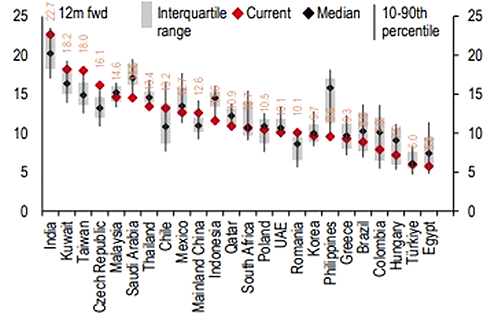

Second, valuations remain exceptionally attractive. Despite the noise, the Brazilian equity market continues to trade at a forward P/E of roughly 10x – well below historical averages and global peers.

EM market valuations vs past 10 years – Brazil the cheapest of the major markets

Source: FTSE Russell, Factset, HSBC

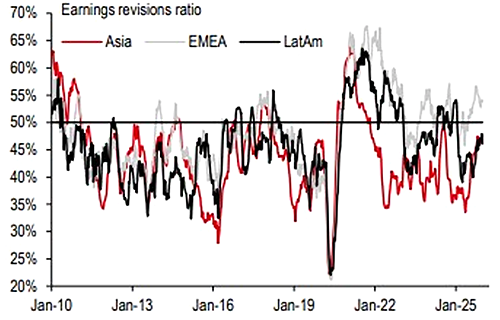

Momentum in earnings revisions ratios is broadly turning higher

Source: FTSE Russell, Factset, HSBC

The « election premium » is already being priced into assets, meaning that any pivot back toward a Tarcísio-led ticket or a credible centrist surge would trigger a massive re-rating.

Historically, when Brazil shifts toward a pro-market administration, the subsequent rallies can exceed 200% in dollar terms.

In summary, while we expect continued volatility through the first half of 2026, the fundamental investment case for Brazil remains intact. We are navigating a period where political pessimism provides a rare window to build positions in high-quality companies at distressed prices.

We remain vigilant but confident that the broader regional trend and the sheer attractiveness of local valuations will ultimately win out over the electoral circus.