L’argent, le moteur des marchés

Global money update: US rebound

26 mars 2026 par Simon Ward

Monetary trends suggest that US economic prospects were improving relative to the Eurozone before the Gulf War III energy shock.

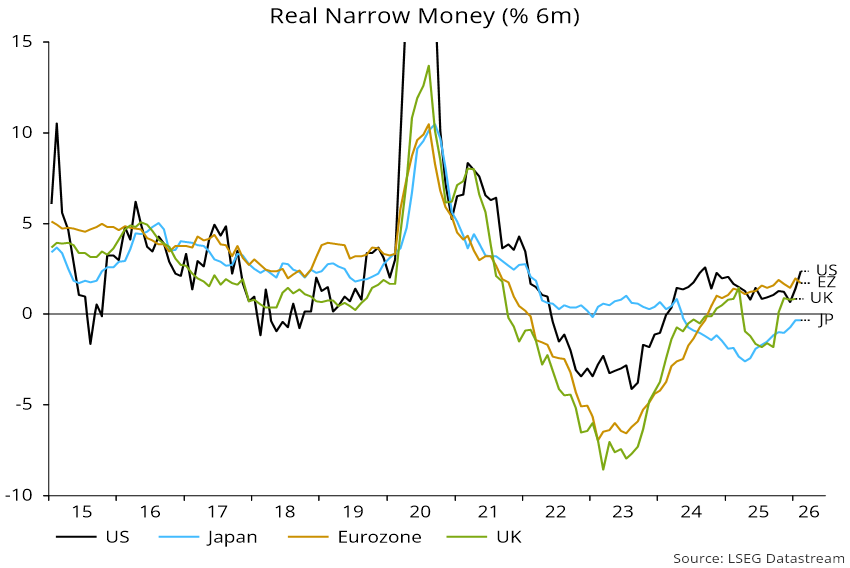

US six-month real narrow money growth rose to its highest since September 2024 last month – see chart 1. (The M1A aggregate used here – comprising currency in circulation and demand deposits – has been adjusted for a previously discussed distortion to November / December deposit data.)

Chart 1

Comparable Eurozone growth, by contrast, eased slightly, resulting in the US taking the lead for the first time since June. Japanese momentum was stable in negative territory, while UK February money numbers have yet to be released.

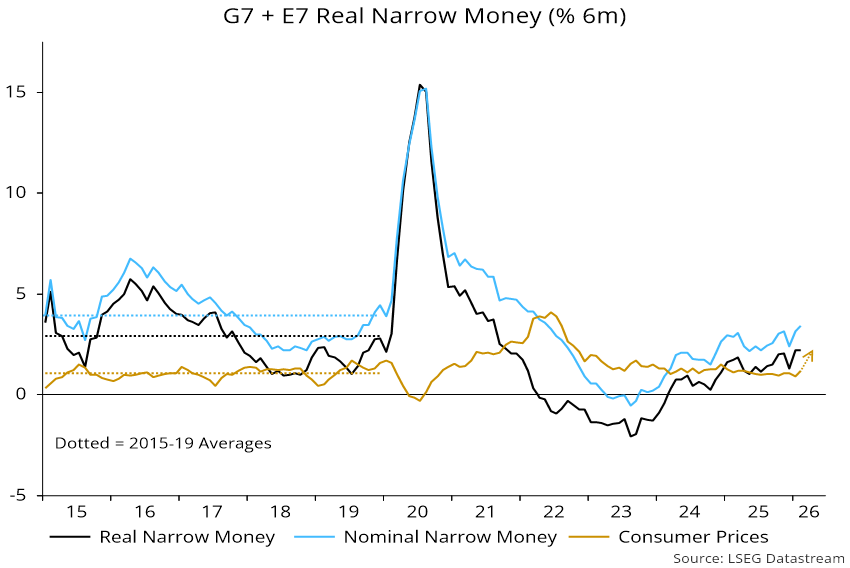

Global – i.e. G7 plus E7 – six-month real narrow money growth is estimated to have been little changed from January’s high, based on monetary data covering 88% of the aggregate – chart 2. So global economic momentum appears to have been on course to hold up through Q3 before the Gulf War III shock.

Chart 2

An early, sharp reversal in real money growth is in prospect, however, as the energy shock boosts six-month consumer price momentum. Higher interest rates, meanwhile, will likely slow nominal money expansion.

Real money trends, therefore, may be moving into alignment with a forecast based on cycle analysis of significant economic weakness in H2 2026-2027.