L’argent, le moteur des marchés

Cyclical vulnerability

13 mars 2026 par Simon Ward

The long-standing forecast here has been that the three key global economic cycles – stockbuilding, business investment and housing – would enter downswings by 2026-27.

In the event that the downswings were synchronised, the result would be a major recession, on the scale of 1974-75 or 2008-09.

If the downswings occurred successively, the result would be a long period of rolling weakness including a less severe recession – the early 1990s scenario.

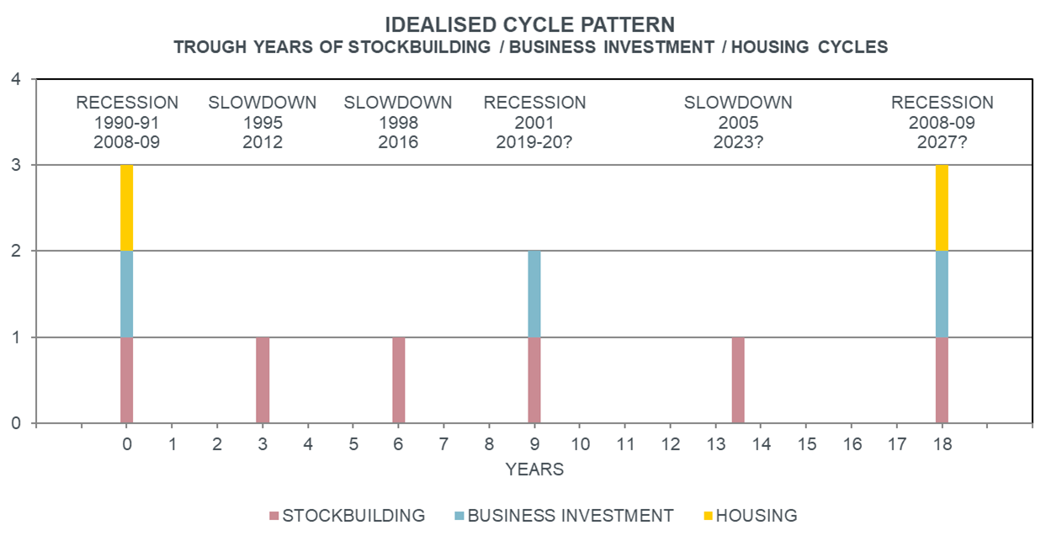

Chart 1 is an exhibit used in 2018, suggesting – based on average cycle timings – a recession bottoming in 2019-20, a slowdown into 2023 and a major recession around 2027. The former two played out.

Chart 1

The housing cycle is already in a downswing, the stockbuilding cycle is at or close to a peak, while the business investment cycle is well-advanced. The Gulf War III energy price shock could be the trigger for synchronised weakness.

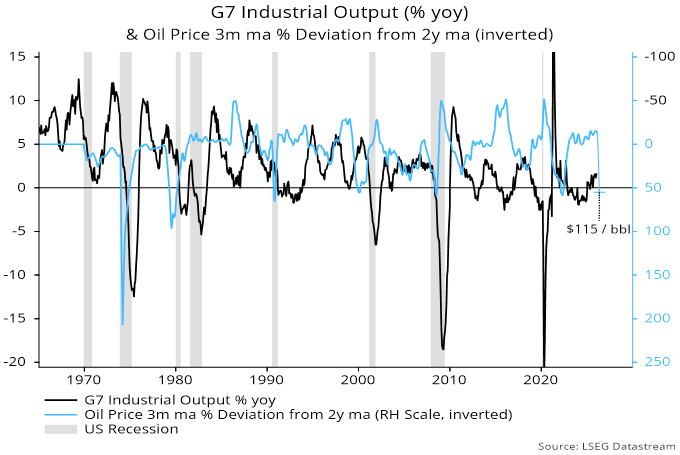

There have been six oil price “shocks” since the 1960s, defined here as episodes in which the spot price rose 50% or more above its two-year moving average for at least three months. All were followed by a significant contraction in G7 industrial output and five were associated with a US recession, as determined by the NBER – chart 2.

Chart 2

Spot Brent of $100 per barrel represents a 37% premium to the two-year moving average. Oil would have to be sustained at about $115 for three months for the current spike to qualify as a “shock”.

The oil intensity of GDP has fallen dramatically since the 1970s, suggesting less vulnerability to shocks. This could explain why the most recent shock – in 2022 – did not involve a US recession.

An alternative view is that a recession was avoided because the cyclical backdrop was less unfavourable and there was pent-up demand due to pandemic disruption, reflected in a large monetary overhang. The stockbuilding cycle turned down in 2022 but the housing and business investment cycles were in late upswing and recovery phases respectively.

The prior shocks caused short-term inflation spikes and were associated with upward pressure on interest rates, contributing to a fall in nominal narrow money momentum. G7 real money contracted ahead of maximum economic weakness. Real money data will be key for assessing the extent of current economic damage.