L’argent, le moteur des marchés

Another central bank policy mistake?

24 mars 2026 par Simon Ward

The Gulf War III energy shock has been compounded by a dramatic repricing of interest rate expectations, partly reflecting hawkish central bank communications, particularly from the ECB and Bank of England.

The central banks fear a repeat of the inflation upsurge around the Russian invasion of Ukraine, their accepted wisdom being that higher energy prices destabilised inflation expectations, resulting in significant “second-round” effects.

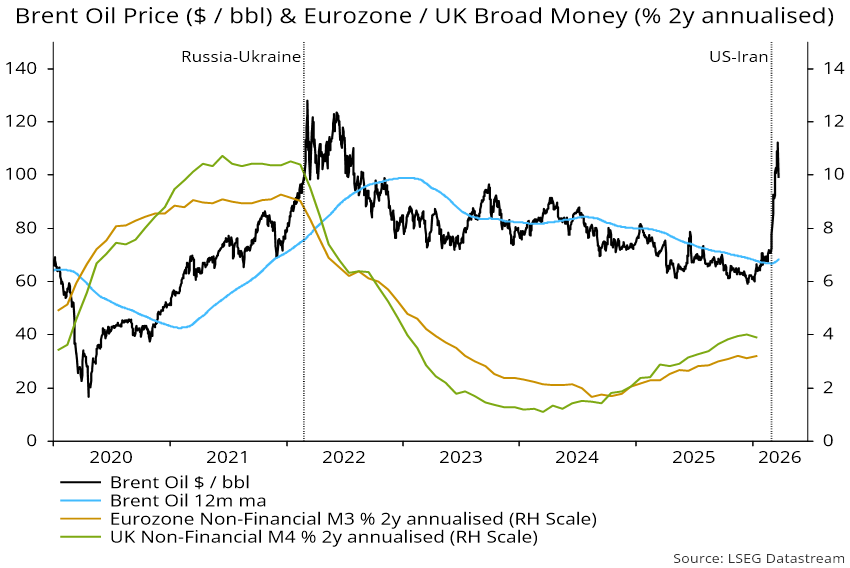

The “monetarist” view is that the impact of a shock on price- and wage-setting depends on the prevailing monetary environment. The Russia-Ukraine shock generated large second-round effects because it occurred against a backdrop of strong money growth. Eurozone and UK broad money – as measured by non-financial M3 and M4 – rose by 9.1% and 10.5% annualised respectively in the preceding two years – see chart 1.

Chart 1

The latest two-year growth rates, by contrast, are 3.2% and 3.9%, with little sign of acceleration in shorter-term data. Money to nominal GDP ratios have returned to around end-2019 levels. Unlike in 2022, there is no monetary “excess” to accommodate a sustained inflation rise.

Policy tightening against this backdrop would likely result in much more serious economic weakness than in 2022-23, with attendant risk of a medium-term inflation undershoot.

One caveat to a relaxed view of second-round effects is that political pressure to respond to a new cost-of-living shock could trigger a fiscal / funding crisis, forcing a return to QE that results in another money growth surge. Still, the suspension of central bank independence implied by such a scenario will be more likely if officials compound their 2021-22 policy error by making the opposite mistake now.