L’argent, le moteur des marchés

Liquidity improvement delayed

22 février 2023 par Simon Ward

The two measures of global “excess” money tracked here remain negative, arguing for a cautious view of equity market prospects.

Excess (or deficient) money refers to the difference between the actual money stock and the demand for money to support economic transactions. According to “monetarist” theory, a surplus is associated with increased demand for financial / real assets and upward pressure on their prices, assuming no change in supply.

Excess money is unobservable so two proxies are followed here: the difference between six-month rates of change of global (i.e. G7 plus E7) real narrow money and industrial output; and the deviation of 12-month real narrow money growth from a slow moving average.

Historically (i.e. over 1970-2021), global equities outperformed US dollar cash on average only when both measures were positive. Unsurprisingly, average performance was worst when both were negative (underperformance of 8.9% pa). These results allow for reporting lags in monetary / economic data.

The second measure turned negative in October 2021, which was known by end-November. The first measure followed in November, which was known by end-January 2022 (a longer lag because industrial output numbers are released after monetary / CPI data).

Previous posts noted a recovery in global six-month real narrow money momentum during H2 2022*. With industrial output expected to weaken, it was suggested that the first measure would turn positive, possibly by December.

The second measure – based on 12- rather than six-month real money momentum – was deeply negative in late 2022, with a switch to positive deemed unlikely before mid-2023.

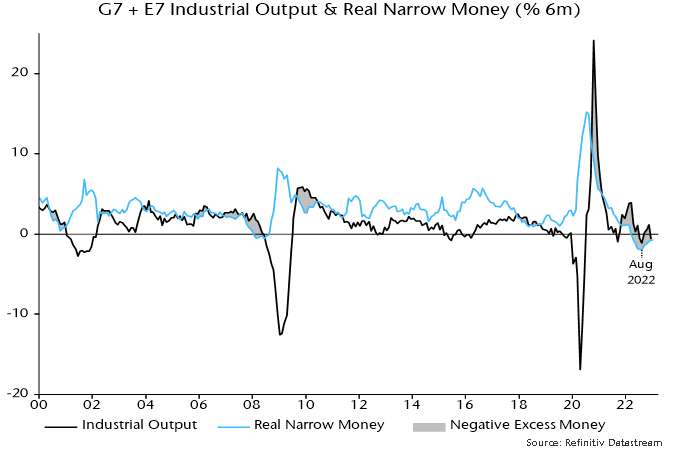

The suggested switch positive in the first measure has yet to occur. The six-month rate of change of industrial output crossed below zero in December but remained just above real narrow money momentum – see chart 1.

Chart 1

Will a cross-over have occurred in January? Partial data suggest that the recovery in real money momentum stalled last month. A reliable January estimate of industrial output won’t be available until mid-March. A reopening bounce in China could offset weakness elsewhere.

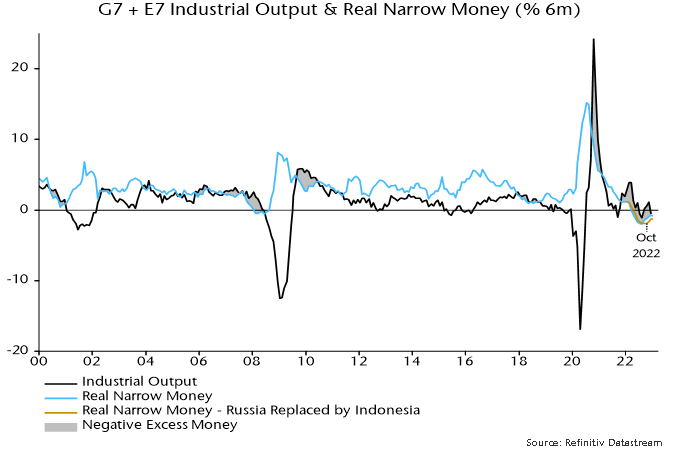

A further point is that the recovery in global real narrow money momentum since mid-2022 partly reflected a strong pick-up in Russia, which may be of limited global relevance given the country’s enforced economic and financial isolation.

Chart 2 shows the result of replacing Russia with Indonesia in the G7 plus E7 real money calculation from January 2022, before the February invasion of Ukraine**. The trough in real money momentum is placed in October rather than August, with the subsequent recovery even more anaemic.

Chart 2

*The trough in real money momentum originally occurred in June but is now placed in August, partly reflecting revisions to US CPI seasonal adjustments.

**The other E7 countries (as defined here) are Brazil, China, India, Korea, Mexico and Taiwan.