Strategic Exchange

How markets defied concerns – 2024 Year in review

January 20, 2025 by Peter Muldowney

Coming off a good year for markets, we entered 2024 with geopolitical risks and high inflation at the forefront of investors’ minds and a myriad of concerns about what could go wrong. Despite some turbulence along the way, markets defied the concerns with US and global equity markets delivering particularly strong returns for 2024. This review delves into how the various key asset classes performed, as well as considerations for 2025 and longer term.

Equities – the technology titans charge on

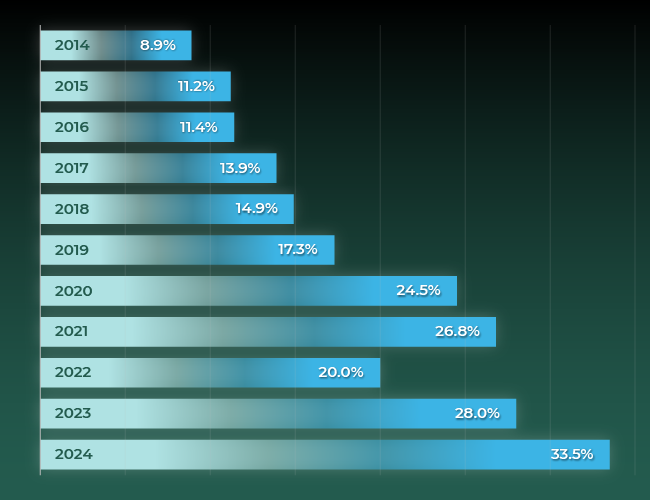

Once again, equity return headlines were dominated by US technology stocks with the Magnificent 7 stocks – Alphabet (Google), Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla – continuing to drive US and global equity markets higher with investor exuberance around the merits of artificial intelligence. Over the last decade, the market capitalization of these seven stocks has significantly grown, with their representation in the S&P 500 Index more than tripling from a decade ago (Figure 1).

Figure 1 – Growth of the Magnificent 7 as a percentage share of the S&P 500 Index

Source: Bloomberg & S&P

US equities represent the largest individual component of most investors’ portfolios, so with the increased level of concentration, portfolio risk management should remain a key focus for investors heading into 2025. This is not to say the US technology sector will not continue to perform well, but 2022 was a reminder of how technology stocks can materially underperform in less favourable environments. The Magnificent 7 dropped from almost 27% of the share of the S&P 500 Index at the end of 2021 to 20% at the end of 2022.

Equities overall deliver good returns

Figure 2 summarizes 2024 calendar year CAD returns for several major equity indices.

| Figure 2 – 2024 equity returns (%) | ||

|---|---|---|

| Canadian Equity | S&P / TSX Capped Composite Index | 21.7 |

| US Equity | S&P 500 Index | 36.4 |

| International Equity | MSCI EAFE Index (net) | 13.2 |

| Emerging Markets Equity | MSCI Emerging Markets Index (net) | 17.3 |

| Global Developed Equity | MSCI World Index (net) | 29.4 |

| Global Equity | MSCI ACWI Index (net) | 28.1 |

| Global Equity Small Cap | MSCI World Small Cap (net) | 18.0 |

Source: Bloomberg, S&P & MSCI

The US equity market was well ahead of the rest of the major developed markets and followed a 22.5% return in 2023. For context, 1997 – 1998 was the last time the US stock market closed out a second straight calendar year with a leap of at least 20%. The strength of the US equity market has also resulted in its increased representation in global equity benchmarks, such as the MSCI World Index. The international equity market trailed other major markets in 2024, impacted by weaker returns from the UK and Europe offsetting the strong returns from Japan equities. While emerging markets delivered 17.3% for the year, China equities was a standout performer within the region, up over 30%.

Fixed income – duration drag

In 2024, the headlines for fixed income markets were focused on how global central banks would react to reducing interest rates in tackling higher inflation. The economic conditions led to several rate cuts throughout the year. However, at various times during the year, fixed income yields rebounded amid concerns about the level of inflation. Figure 3 summarizes 2024 calendar year returns for several fixed income indices.

| Figure 3 – 2024 fixed income returns (%) | ||

|---|---|---|

| Cash | FTSE Canada 91 T-bill Index | 4.9 |

| Universe Bonds | FTSE Canada Universe Bond Index | 4.2 |

| Long Term Bonds | FTSE Canada Long Term Overall Bond Index | 1.3 |

| High Yield Bonds | Merrill Lynch US High Yield Cash Pay BB Index | 10.5 |

Source: Bloomberg, S&P, Merrill Lynch & FTSE

High yield strategies led public fixed income calendar-year returns. Despite the decline in short-term rates over the year, cash markets delivered healthy returns with the FTSE Canada 91 Day T-bill Index up 4.9%. Within the fixed income component, investors such as Indigenous Trusts, endowments and foundations are typically invested across the maturity spectrum in a combination of short-, medium- and longer-term fixed income investments, such as strategies benchmarked to the FTSE Canada Universe Bond Index. The Universe Bond index returned 4.2% for the calendar year.

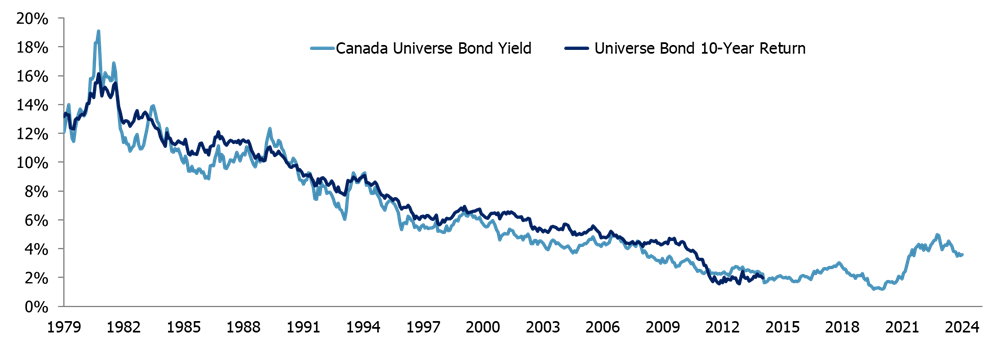

Lower longer-term return on the horizon

The current yield of the Universe Bond Index provides a reasonable indicator of expected long-term returns. Figure 4 shows the universe bond yield over time (light blue line), as well as the actual subsequent absolute 10-year returns, represented by the dark blue line. There is a strong correlation between the two lines, suggesting the end of 2024 yield of 3.6% is a reasonable indicator of the expected return of universe bonds over the next 10 years.

Figure 4 – Universe Bond yields versus subsequent 10-year returns

Source: Bloomberg & FTSE

From a return perspective, given the potential for a lower longer-term Universe Bond Index return, higher yielding strategies, such as high yield debt, emerging market credit, commercial mortgages, and private credit may see increased interest from investors who are looking to enhance fixed income returns.

From a risk management perspective, we expect to see continued interest in absolute return fixed income solutions. These are designed to deliver returns above cash without being subject to the volatility that universe bond strategies experienced in 2024 (as well as in the prior two calendar years); they are not beholden to a benchmark level of duration and associated fluctuations with changes in yields.

Defined benefit plan dynamics

It is a different story for defined benefit (DB) pension plans whose fixed income consideration is inclined to be more on risk management than return generation. DB plans will typically have a significant allocation to long-term fixed income assets to hedge interest rate risk associated with changes in the value of their liabilities. Factors driving longer-term yields are less influenced by central bank policy and in 2024 experienced much lower returns than cash and Universe Bonds due to longer-term yields slightly increasing over the year.

The significant improvement in the funded position of DB plans over the last several years has seen many increase the level of interest rate risk hedging to reduce funding level fluctuations. The specific actions have depended on the type of DB plan (e.g., corporate, university or public), actuarial liability measures that drive risk assessments, factors such as whether the DB plan is open or closed to new members and plan maturity (e.g., percentage of active members versus retiree and deferred members).

Another risk management trend that continued at a strong pace in 2024 with corporate plans was de-risking through annuity purchases from insurance companies. Increasingly referred to as “pension risk transfer” (PRT), the purchase of annuities allows a company to reduce the dollar liability on its balance sheet by transferring assets and liabilities to the insurance company. Estimates for the Canadian PRT market in 2024 are that it will be greater than the 2023 record, which was just shy of CAD 8 billion. The PRT market has evolved significantly since being personally involved with the first modern annuity buy-in by a Canadian pension plan in 2009. Back then, the yearly value of the group annuities market was about CAD 1 billion with most transactions being for pension plans that were winding up and using annuities to settle their retirement benefit liabilities rather than as a risk transfer solution popular today.

Mixed experience from private markets

Over the past 10 years or so, private markets have experienced significant inflows from institutional investors. According to PwC, global assets under management (AUM) is expected to top USD 145 trillion in 2025, nearly double the almost USD 84.9 trillion in 2016.1 The same research predicts that alternative investments will reach above USD 21 trillion by 2025, representing 15% of all AUM.

For private markets, it is difficult to generalize since the returns and outlook are heavily influenced by the specific strategy in which you are invested. However, 2024 saw another mixed experience for returns across the various private markets. Private credit and infrastructure strategies delivered decent returns. Infrastructure continues to gain interest from investors due to its critical role in global efforts to address climate risk through clean energy projects, as witnessed by an increased number of strategies focused on energy transition. Private credit is also expected to play a growing role in the financing of energy transition projects.

Commercial real estate and private equity were the laggards within private markets, although sentiment is improving. In times of market stress and lower valuations also comes opportunities, which was the case within commercial real estate and the launch of various opportunistic strategies.

Hedge funds are the often-overlooked alternative investment option. There are many different strategies, so again it is difficult to generalize. Few hedge funds would have been able to keep up with the S&P 500 Index return in 2024. The combination of higher public equity returns, the greater complexity and higher investment management fees associated with hedge funds can make it challenging for many investors to consider them for their portfolio. However, equity markets will not always be so strong and hedge funds can provide important portfolio diversification in certain challenging environments.

Canadian investors benefited from currency and commodities

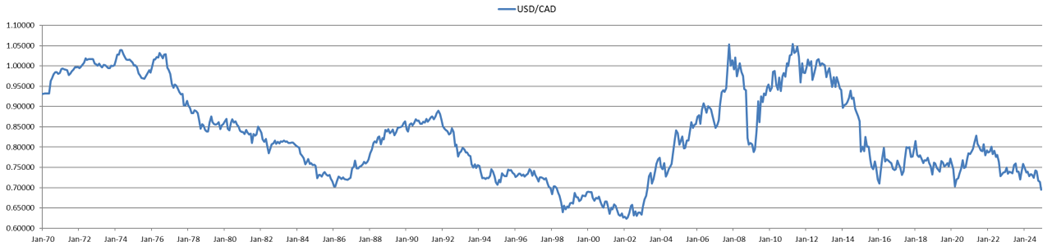

The Canadian dollar declined more than 8% over the year relative to the US dollar, which helped to boost US equity returns for unhedged Canadian investors. Figure 5 shows the history of exchange rates from 1970, capturing the modern-day experience with respect to the Canadian dollar versus the US dollar relationship. Over the period there have been three major declines in the value of the Canadian dollar, which from peak to trough were each down a little over 30%. The first two declines took around 10 years, while the most recent experienced the fastest decline, which was in part due to the swift collapse in oil prices.

Since the last trough in 2016, the Canadian dollar has moved in a relatively narrow range, even accounting for the uncertainty associated with the COVID-19 pandemic and the elevated levels of inflation. The Canadian dollar was valued at 69.53 cents (US) at the end of 2024, creeping closer to testing the 68.68 cents (US) level that was previously thought to be the low point for the most recent peak-to-trough.

Figure 5 – History of USD / CAD Exchange Rates

Source: Bloomberg

While currently not a popular investment with institutional investors, bitcoin saw a dramatic rise in value. Helped by rates coming down, it had a particularly big boost following Donald Trump’s US election victory. Bitcoin ended the year at over USD 90,000, which compares with being below USD 16,000 just two years ago following the collapse of crypto exchange FTX.

Wars around the world have helped drive demand for investments seen as a safe haven, like gold. Also benefitting from the Fed cuts in interest rates, gold returned 27% for the year. With a higher allocation to the gold sector compared to other major equity markets, the Canadian equity market was a beneficiary of the strong gold return.

Déjà vu for 2025?

As we enter 2025, several of the concerns and uncertainties that were present at the start of last year are still looming. There are also potential distractions of a second Trump term as US president and Canada with no formal leadership at the helm of the country. Despite the uncertainties entering 2024, the outcome was a positive experience. As we roll into 2025, it is important to remember that markets are difficult to predict over the short term, so investors should not overlook the importance of portfolio risk management, including disciplined rebalancing and consideration of additional sources of portfolio diversification to optimize portfolio performance.

1. PwC report ‘Asset & Wealth Management Revolution: Embracing Exponential Change’