L’argent, le moteur des marchés

US money update: balance of payments drag

30 mai 2025

US money growth is slowing, suggesting less support for the economy and improving prospects for rate cuts.

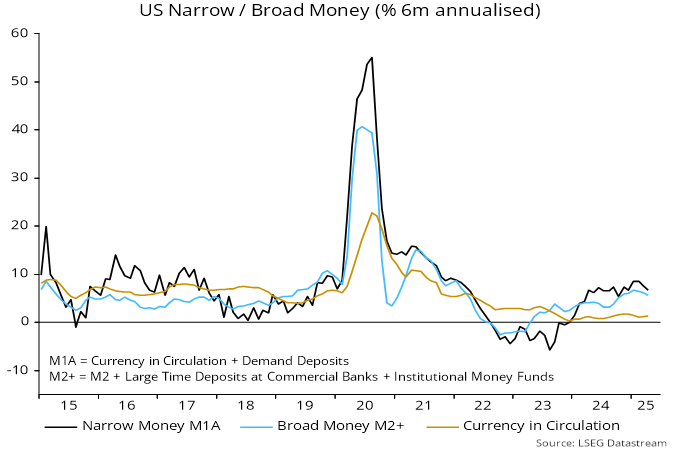

Six-month growth of the preferred narrow and broad aggregates here fell to 6.6% and 5.6% annualised respectively in April, down from recent peaks of 8.6% and 6.7% – see chart 1.

Chart 1

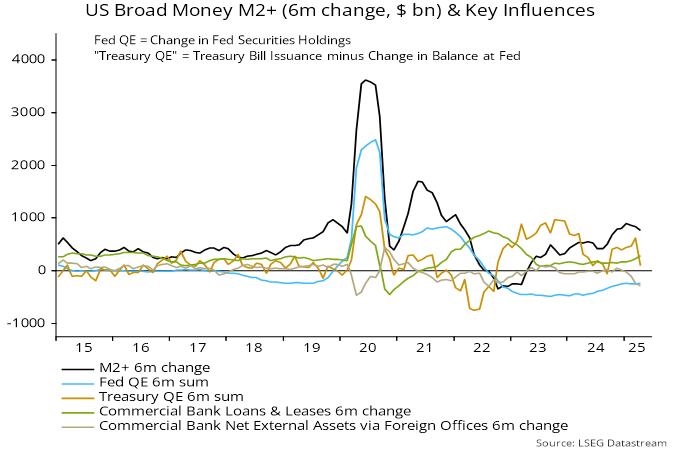

Chart 2 shows key influences on broad money expansion. Strength in late 2024 / early 2025 was driven by monetary deficit financing initiated by the Treasury (“Treasury QE”). The six-month running total of such financing, however, fell sharply in April, reflecting a recent reduction in the stock of Treasury bills coupled with a rebound last month in the Treasury’s cash balance at the Fed.

Chart 2

Another significant contributor to the monetary slowdown has been a decline in commercial banks’ net external assets. Changes in such assets are the counterpart of the basic balance of payments position. This position has weakened as tariff front-running has boosted the trade deficit, while negative and chaotic policies have discouraged portfolio capital inflows.

Fed QT has remained a drag on broad money growth but the six-month impact is moderating, reflecting the April taper.

The monetary slowdown has also been mitigated by a pick-up in bank loan growth.

A consideration of prospects for these influences suggests that money growth will moderate further.

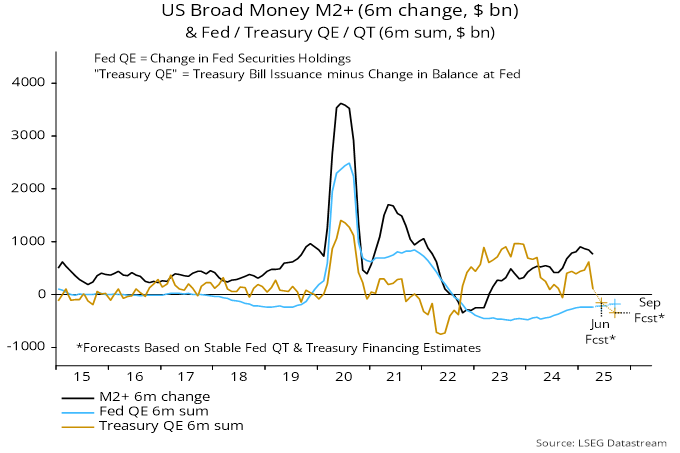

As previously discussed, the Treasury’s financing plans, based on a lifting of the debt ceiling, imply a sizeable negative impact in the six months to September as issuance resumes and the Treasury’s balance at the Fed is restored to its prior level – chart 3.

Chart 3

The Fed could taper QT further to ease associated pressure on bank reserves but may not fully offset the Treasury drag.

The basic balance of payments may remain weak as foreign investors diversify away from US exposure.

The recent pick-up in bank loan growth, meanwhile, partly reflects tariff-related stockbuilding and may slow as this moderates. Acceleration was signalled by the Fed’s senior loan officer survey but corporate credit demand balances fell back in the latest (April) report.