L’argent, le moteur des marchés

Will the UK join the double dip?

02 octobre 2024 par Simon Ward

Monetary trends suggest that UK economic performance will converge down to a weak Eurozone.

A post in June argued that Eurozone monetary trends were too weak to support a sustained recovery. The composite PMI output index peaked in May and fell below 50 in September (flash reading of 48.9), confirming an ongoing “double dip”.

The UK economy has outperformed year-to-date: GDP grew by 1.2% between Q4 and Q2 versus a 0.5% rise in the Eurozone, while the composite PMI has moved sideways above 50 (September flash reading of 52.9).

This outperformance, however, follows relative weakness in H2 2023, when GDP contracted in the UK but eked out a small gain in the Eurozone. Q2 year-on-year GDP growth rates are similar, at 0.7% and 0.6% respectively.

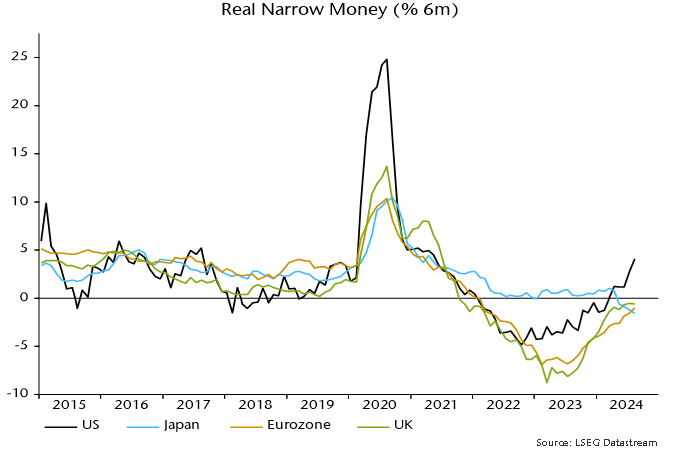

This pattern – of UK underperformance in H2 2023 followed by a catch-up in 2024 – had been signalled by monetary trends. Six-month real narrow money momentum was weaker in the UK than the Eurozone in 2022 through Q2 2023 but UK momentum recovered faster last year and had opened up a lead by Q1 2024 – see chart 1.

Chart 1

The lead, however, has been narrowing since April and almost closed in August, partly reflecting a recent stalling of the UK recovery. With momentum still negative, the suggestion is that UK and Eurozone economic performance will be similarly weak through early 2025.

As well as supposed UK relative economic strength, the expectation that rates will be slower to fall in the UK than the Eurozone incorporates a belief that inflation will prove stickier. This is also at odds with monetary trends.

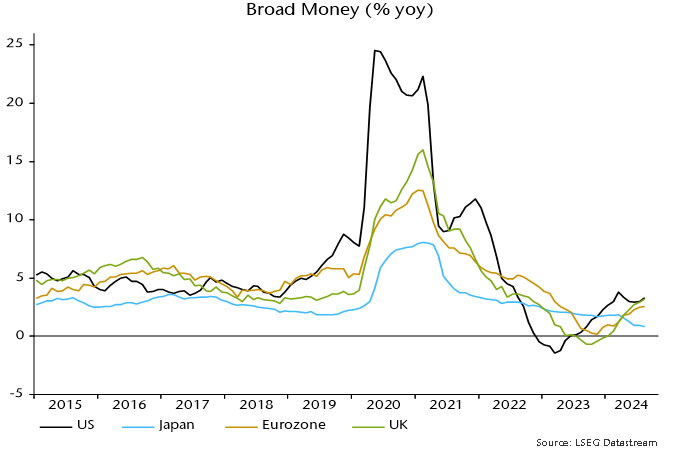

Inflation rates are tracking the profile of broad money momentum two years earlier, in line with a simplistic monetarist prediction. Annual broad money growth was lower in the UK than the Eurozone in 2022 and 2023, suggesting that an undershoot of UK annual CPI inflation versus the Eurozone over May-July will resume in 2025 – chart 2.

Chart 2

A UK double dip would be blamed partly on the confidence-sapping impact of the new government’s gloomy fiscal pronouncements. The MPC’s failure to deliver timely easing would carry much greater responsibility.