Commentaires

South Korea rocked by president’s attempt to impose martial law

12 décembre 2024

Deeply unpopular South Korean president Yoon Suk Yeol committed a monumental act of executive overreach with his declaration of martial law on the 3rd of December. The decree was a wild strike against the opposition Democratic Party, which had effectively paralysed his presidency since taking power in parliament earlier this year.

The move set off a chaotic few hours of street protests with deployment of the military in the streets of Seoul and politicians of all stripes, including the head of the president’s own People Power Party, denouncing the declaration. The drama culminated in a unanimous vote by the country’s legislature (including members of the president’s party) to reverse the failed coup attempt.

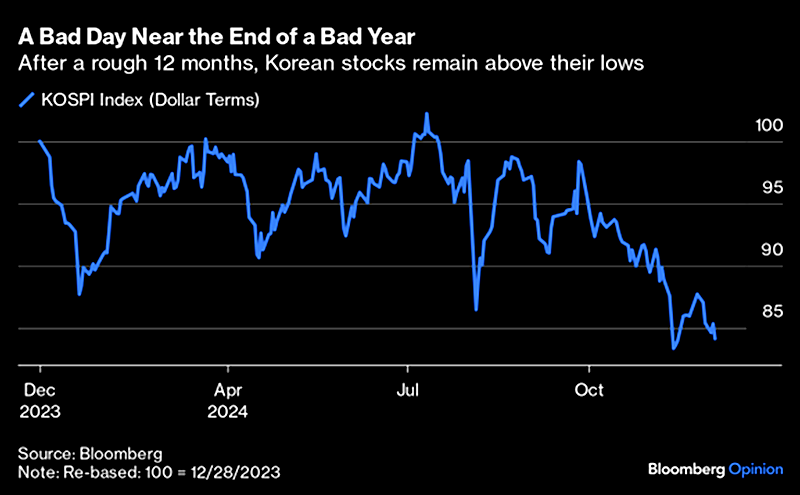

Big moves in the Won and Korean equities

Source: Bloomberg Opinion, December 4, 2024

Yoon now faces the threat of impeachment, but that is probably the least of his worries. Around half of South Korea’s living former presidents are sitting in prison, and Yoon may be set to join their ranks.

Is it too rose-tinted a view to argue that the legislature’s swift move to strike down the declaration is a positive demonstration of institutional checks shifting into gear? Almost certainly, as the People Power Party has said that it will seek to block any impeachment motion in the legislature (the motion requires a two-thirds majority of the 300-seat parliament). It is safe to say that this political crisis is set to grind on for some time yet.

Sitting tight

We have been underweight South Korea, with low exposure to the domestic economy through bank KB Financial, Kia and Hyundai, partly reflecting weak monetary trends. DRAM export giants SK Hynix and Samsung Electronics make up two-thirds of our holding.

Earlier this year we wrote to investors on the prospects for the Value-Up corporate reform program promoted by the Yoon government to boost perennially cheap Korean equities (Super-cheap Korean equities rally on market reform talks). At the time we had shifted to a significant overweight, favouring likely domestic reform beneficiaries.

However, a landslide win for the opposition DPP in the legislature in April made it less likely the program would be implemented in full. The political shift occurred against a weakening economic backdrop globally, and also in South Korea’s highly cyclical domestic economy.

Following a downgrade to our country rating, we reduced exposure to Kia and Hyundai. We also took some profits from our position in SK Hynix after strong performance on its monopoly as a high-bandwidth memory supplier to Nvidia.

Given the above, we are not tempted to try and catch a falling knife by doubling down in South Korea.

Samsung Electronics is cheap, but is that enough?

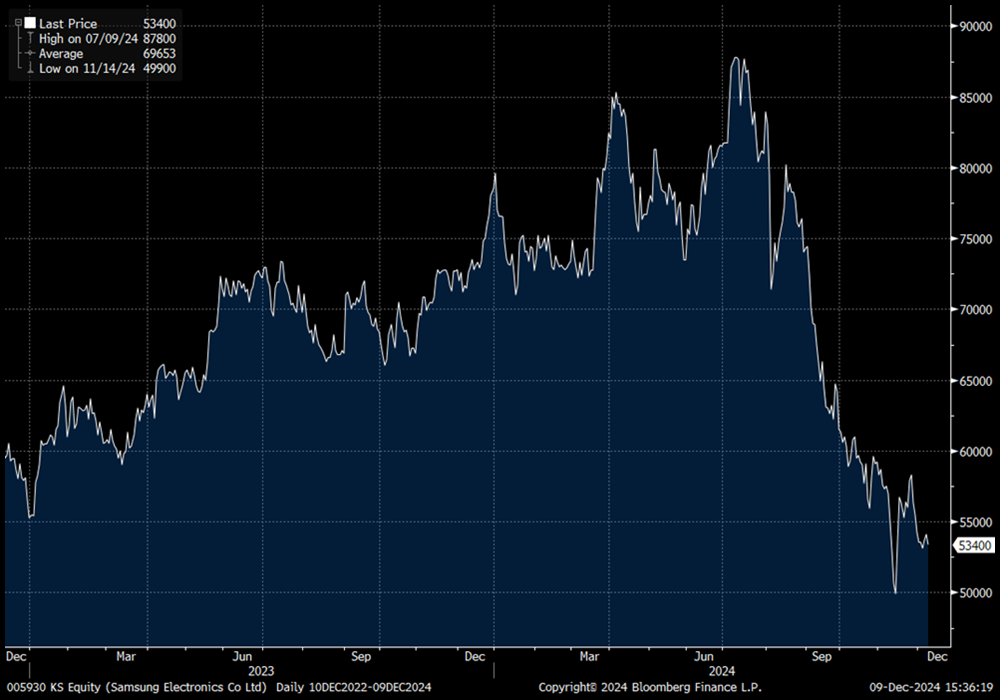

Following a strong start to the year, Samsung Electronics fell sharply since July and now ranks as one of the worst performers year-to-date in our portfolio. What happened?

Sell-off for Samsung Electronics since July

Source: Bloomberg

Investors fear that management missteps have cost the company its technological edge in chipmaking. Indeed, we have been surprised by how badly Samsung has lagged SK Hynix in high-bandwidth memory. It ranks as a distant second to Hynix as a supplier of HBM3E memory to Nvidia and it is uncertain whether the company can close the gap in the next generation of HBM products.

In addition, the long hoped-for demand recovery in commoditised DRAM products is yet to arrive. More bearish analysts fret over the rise of Chinese memory and what this could mean for the Samsung-Hynix-Micron oligopoly, which has kept supply in check over the past decade.

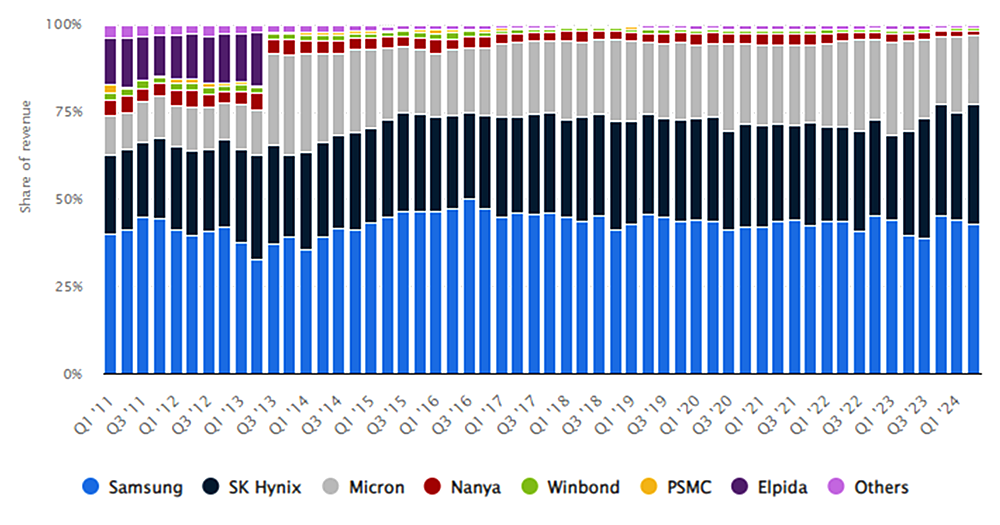

Samsung Electronics, SK Hynix and Micron have maintained an iron grip on DRAM supply

Source: Statista 2024

Source: Statista 2024

Major Chinese DRAM players like CMXT are yet to register in global market share, but risks to the oligopoly may emerge down the road.

All of the above paints a pretty sorry picture for Samsung, reflected in valuations that are at the bottom of historic ranges.

Buying at these levels has historically been a good bet – Samsung Electronics Price/Book

Source: Bloomberg

Management is desperate to turn this around through deep restructuring, boosting R&D spend and buying back shares. Samsung has a history of pivoting out of trouble, and the valuation is incredibly cheap for one Asia’s most successful tech behemoths.

We are not tempted to double down at these levels, but plan to maintain the current weighting. Moving forward, we will look to see whether Samsung can reassure investors by gaining qualification as a HBM supplier for Nvidia’s leading-edge products. Not only would this boost earnings, it would also signal that it can close the tech gap with SK Hynix.

Mindful of “success bias” in US equities

Investors in emerging markets are going against the grain. Today the herd is stampeding into US stocks. The drivers for the dominance of US equities are compelling, propelled by better economic performance, higher productivity growth and innovation.

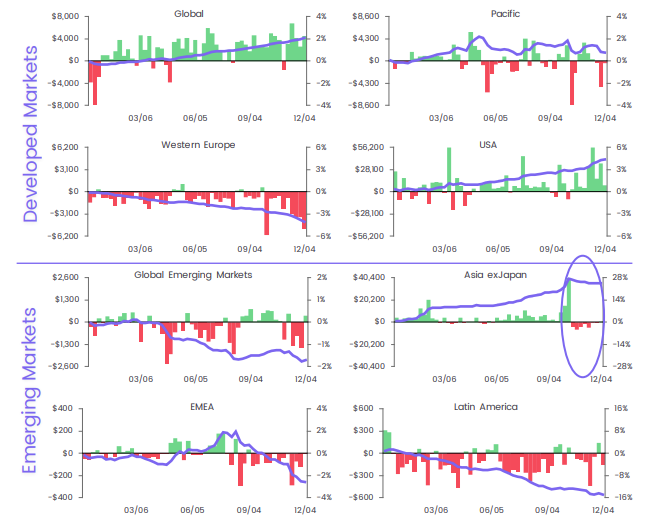

Equity flows by region

Source: EPFR

And yet, making money as an investor is all about the delta between reality and expectations. Investors myopically fixated on market narratives about US exceptionalism as justification for extreme outperformance versus the rest of the world risk overstaying their welcome, along with missing opportunities in unloved markets.

Ruchir Sharma’s Financial Times article The Mother of All Bubbles opines on just how dominant the United States has been as an investment destination:

- Global investors are committing more capital to a single country than ever before in modern history.

- And the dollar, by some measures, trades at a higher value than at any time since the developed world abandoned fixed exchange rates 50 years ago.

- The US now attracts more than 70 per cent of the flows into the $13tn global market for private investments, which include equity and credit.

- America’s share of global stock markets is far greater than its 27 per cent share of the global economy.

- Thoroughly dominating the mind space of global investors, America is over-owned, overvalued and overhyped to a degree never seen before.

UBS just published some excellent charts illustrating just how stark this dominance has been:

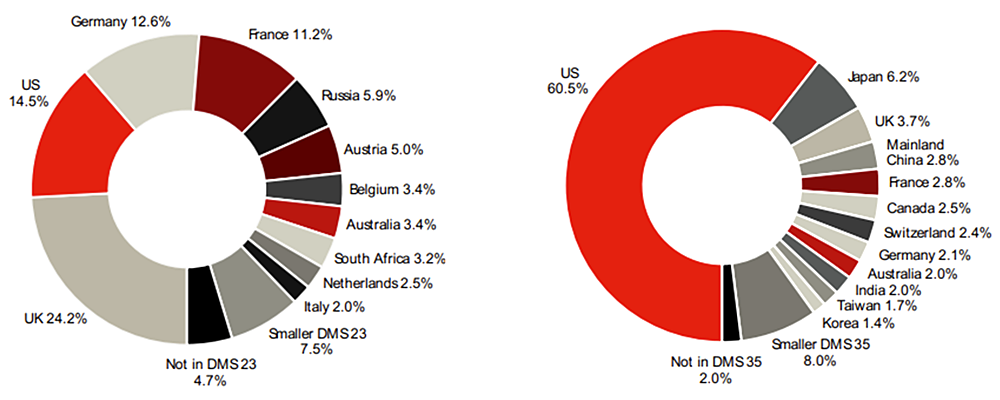

Relative sizes of world stock markets, end – 1899 (left) versus start – 2024 (right)

Source: Global Investment Returns Yearbook 2024, UBS

Investors adding to US exposure at the expense of the rest are making a bet that such scorching outperformance can continue.

While it seems unlikely, author of liquidity theory and bubble expert Gordon Pepper said that to work out the duration of a bubble, take your best analysis to work out how long it will go, double that, and then subtract a month. In other words, extenuated bull markets (or bubbles) have a habit of going on longer than we could ever imagine before ending abruptly (and often brutally).

We believe it is a fool’s errand to attempt to predict when equities ex-US will be back in vogue. However, what we know for sure is that less competition among buyers in unloved emerging markets tilts the odds of unearthing value-creating businesses at attractive prices in our favour.