L’argent, le moteur des marchés

More slowdown signals

09 juin 2026 par Simon Ward

OECD leading indicator data and survey evidence on stocks support the forecast of a H2 loss of industrial momentum.

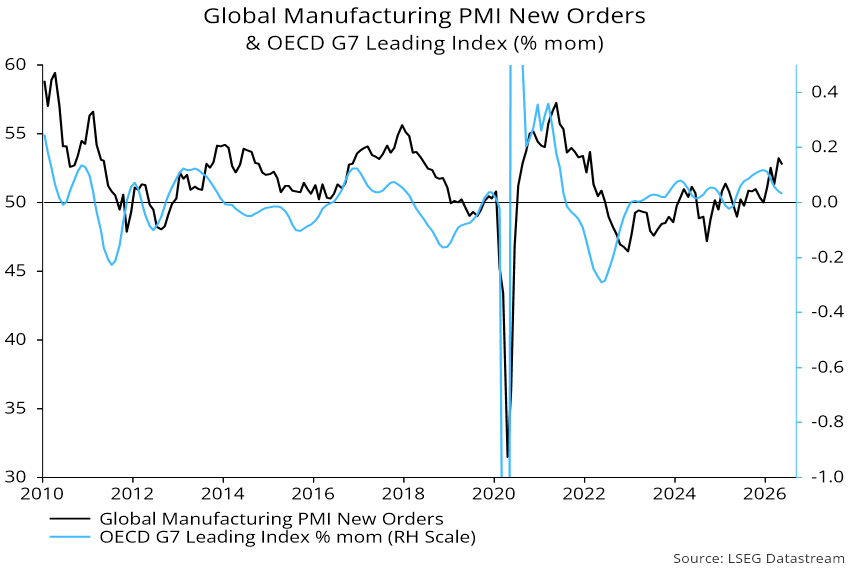

Global manufacturing PMI new orders edged down in May from April’s four-year-plus high. The expectation here has been for a further decline in H2, reflecting a slowdown in global six-month real narrow money momentum from a February peak – see previous post.

Two recent releases support this forecast. First, one-month growth of the OECD’s G7 leading indicator fell again in May. Growth peaked in December and has led PMI new orders by three months on average historically, suggesting that April’s orders high will prove lasting – see chart 1.

Chart 1

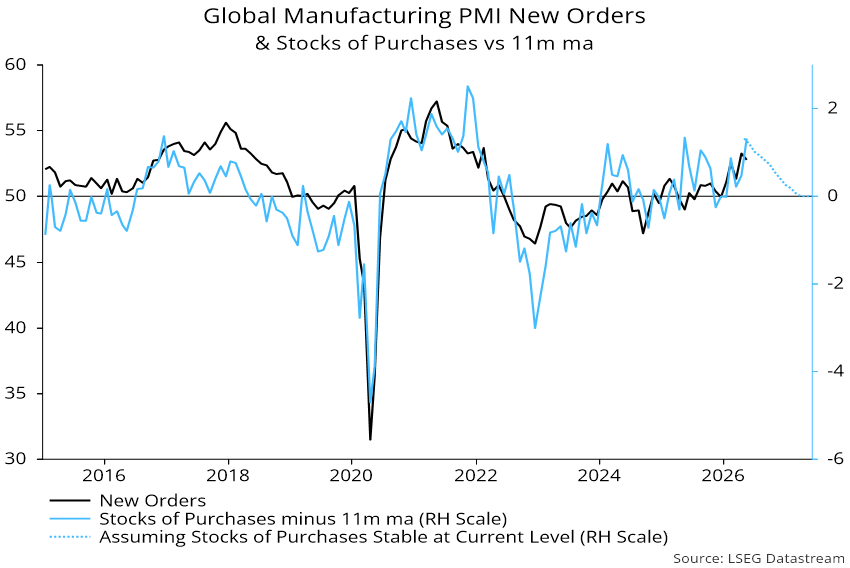

Secondly, the PMI stocks of purchases index indicates that stockpiling of inputs accelerated further last month, likely marking a cycle peak – chart 2.

Chart 2

Growth in new orders is related to the rate of change of stockbuilding, implying a slowdown even in the unlikely event that the stocks of purchases index remains at its current extended level – chart 3.

Chart 3