L’argent, le moteur des marchés

Monetary tremors

06 février 2026 par Simon Ward

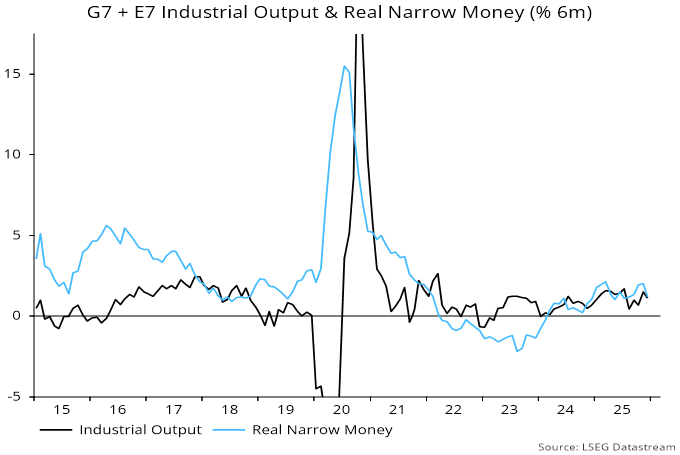

A January post noted the possibility that global six-month real narrow money momentum had crossed below industrial output growth in December, suggesting less favourable monetary conditions for markets. Recent dramatic sell-offs in some speculative assets could reflect such a shift.

The suggestion is still tentative: additional – but not yet complete – December data indicate that the two series converged rather than intersected – see chart 1.

Chart 1

Will a cross-over be confirmed soon? Monetary prospects are uncertain but stronger January manufacturing PMI results suggest a rise in six-month industrial output momentum in early 2026.

In data since 1970, global equities outperformed US dollar cash significantly on average in months following a positive reading of the gap between real money and output momentum (by 12.0% annualised). (The calculation allows for reporting lags.)

By contrast, negative gaps were associated with average underperformance in the following month (of 5.5%).

Needless to say, these averages conceal frequent “misses” in both directions.

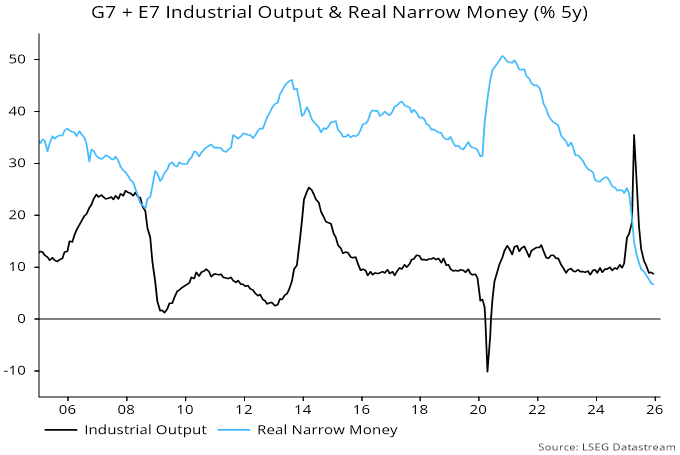

The six-month real money / output momentum gap was positive in most months in 2025. It was, however, negative in 2023 and much of 2024, when equities rallied strongly.

As previously discussed, the six-month gap was a misleading guide to “excess” money over this period because of a large monetary overhang from the money growth surge in 2020-21.

A simple way of illustrating this overhang is to compare five-year growth rates of real money and industrial output. Real money growth was still much higher in 2023 – chart 2.

Chart 2

The five-year gap turned negative last year. It last closed in the early stages of the GFC bear market.

Back then, the six-month gap had been negative for more than a year. The closing of the five-year gap was followed by an acceleration of the market decline.

With the five-year gap already negative, a negative shift in the six-month gap could be reflected in more immediate market weakness than in 2007-08.