L’argent, le moteur des marchés

Magical thinking on tariffs

28 février 2025 par Simon Ward

Reciprocal tariffs represent an indirect tax rise on cross-border trade in goods.

The US might be expected to suffer less damage from a global rise in tariffs than China and the EU because trade is a lower share of GDP.

Such logic, however, does not apply currently because conflict is occurring in US bilateral relationships rather than globally. So the share of GDP potentially affected by tariffs is larger for the US than China / the EU.

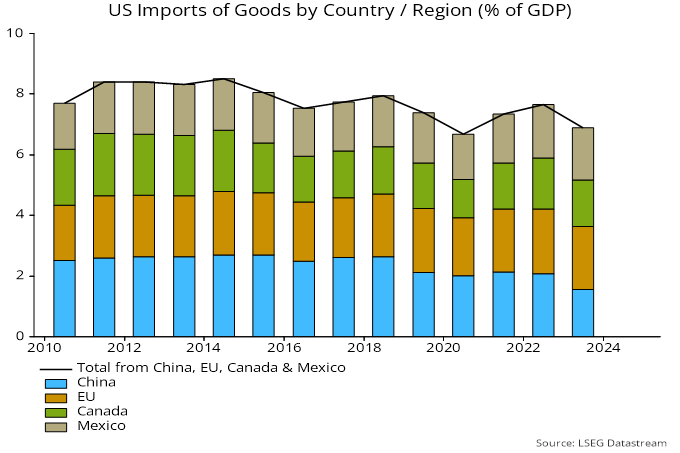

Goods imports from countries currently on President Trump’s tariffs hit list represent about 7% of US GDP, with a suggested 20% blended hike implying an effective tax rise of 1.4% of GDP ($410 bn) – see chart 1.

Chart 1

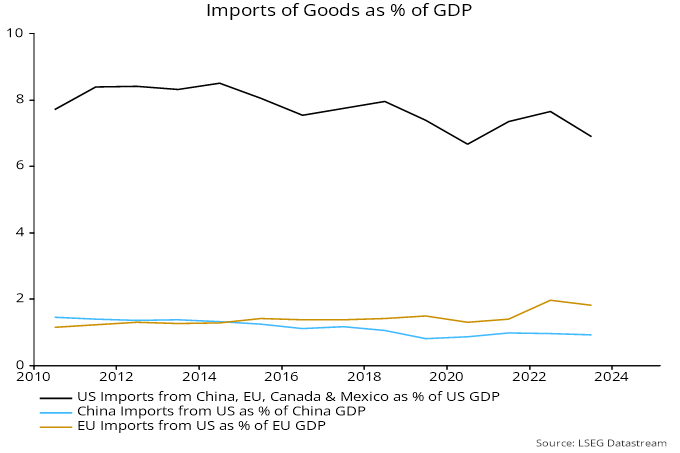

Assuming full reciprocity, Chinese and EU tariffs will affect imports accounting for less than 1% and less than 2% of their GDPs respectively – chart 2.

Chart 2

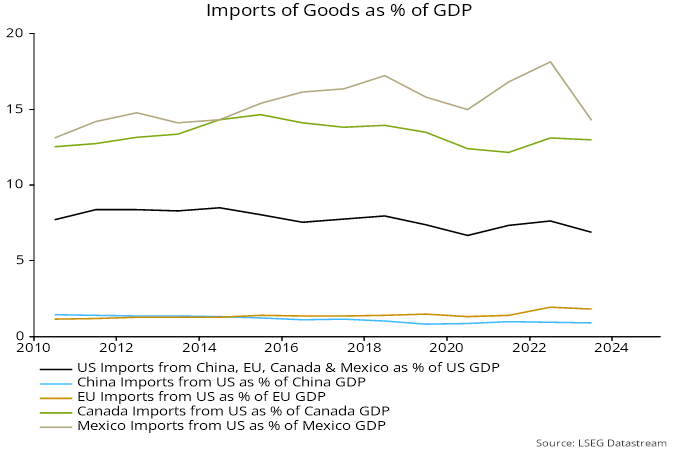

By contrast, Canada and Mexico will impose a much larger effective tax rise than in the US if they reciprocate Trump’s tariff rates (which is why they won’t) – chart 3.

Chart 3

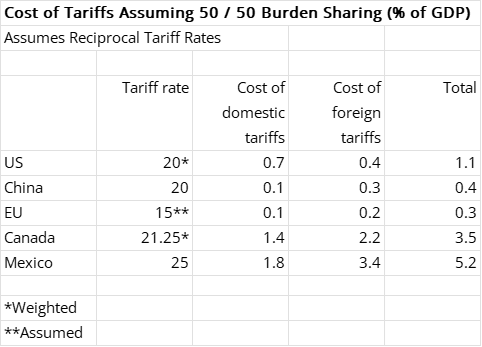

A reasonable baseline assumption is that tariff burdens will be shared equally between domestic consumers and foreign producers. Assuming full reciprocity, the US would suffer more than China / the EU (but much less than Canada / Mexico) – see table.

Advocates of tariffs claim that their imposition will boost the dollar, resulting in an improvement in the terms of trade that offsets the effective tax rise on consumers. Tariff revenues will be available to cut taxes or reduce the deficit, for a net economic gain.

This is magical thinking and begs the question of why tariff-raising has not previously been recognised as an optimal economic strategy. Equally plausible is that tariffs will undermine US economic outperformance and weaken the dollar / terms of trade, compounding the hit to domestic purchasing power.