L’argent, le moteur des marchés

Japan’s QT disaster

09 juillet 2026 par Simon Ward

Why are Japanese longer-term government bond yields continuing to trend higher, in contrast to range-bound trading in other major markets?

The conventional explanation is that monetary policy remains too loose. Inflation is back and the Bank of Japan is “behind the curve”. Investors are reluctant to buy bonds until a rate peak is in sight.

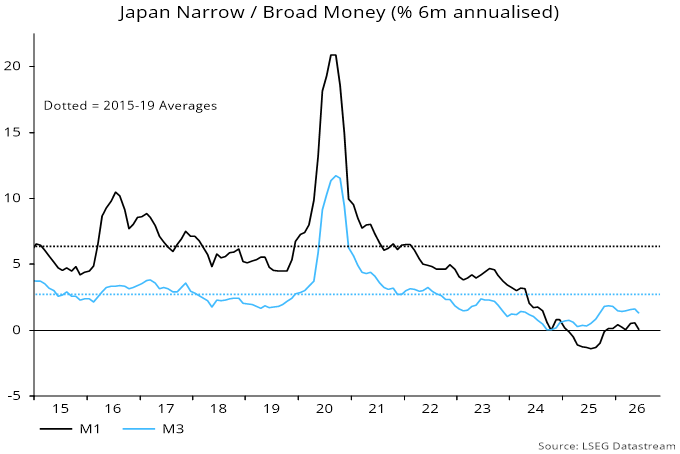

The “monetarist” view is opposite. Bonds are selling off because monetary conditions are restrictive. M3 and M1 grew at annualised rates of just 1.3% and 0.1% respectively in the six months to June – see chart 1.

Chart 1

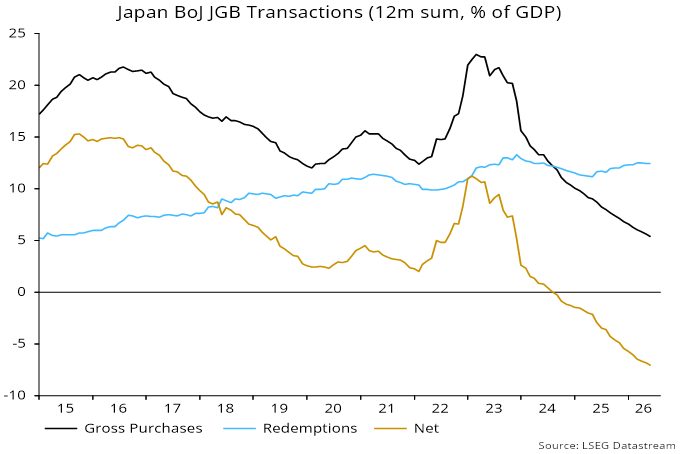

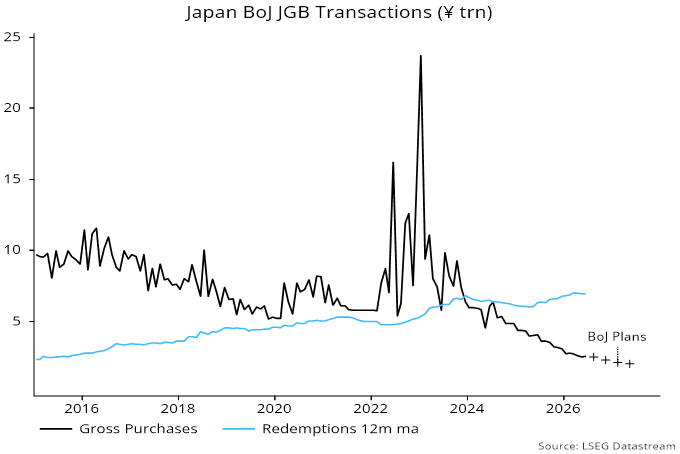

Money growth is being crushed by massive and still-rising QT. The BoJ’s net disposal of JGBs amounted to 7.0% of GDP in the year to June. Plans to reduce monthly purchases further imply an increase to c.8.5% by mid-2027 – charts 2 and 3.

Chart 2

Chart 3

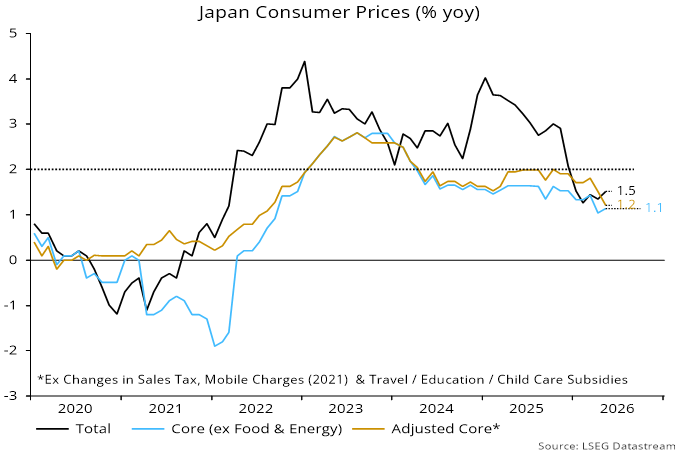

Consistent with the monetarist view, annual core CPI inflation is below 2% and falling even adjusting for government subsidies, despite upward pressure on import prices from the weak yen – chart 4.

Chart 4

Real yields may be reaching an attractive level but potential buyers are understandably reluctant to fight the BoJ “whale”. With JGBs off-limits, available money is being directed towards equities and foreign markets, contributing to the yen’s slide.

Stopping QT would probably trigger a surge in demand for JGBs, including by foreigners. Lower yields would ease concerns about fiscal sustainability. Capital inflows would strengthen the yen and add to the lift to money growth from ending the QT drag. Stronger money growth would support medium-term achievement of the inflation target without reliance on currency depreciation.

Continued QT on the planned scale, by contrast, promises sustained monetary weakness and an eventual return to deflation.