L’argent, le moteur des marchés

Is Eurozone “recovery” aborting?

28 juin 2024 par Simon Ward

Eurozone money trends remain too weak to support an economic recovery. A relapse in the latest business surveys could mark the start of a “double dip”.

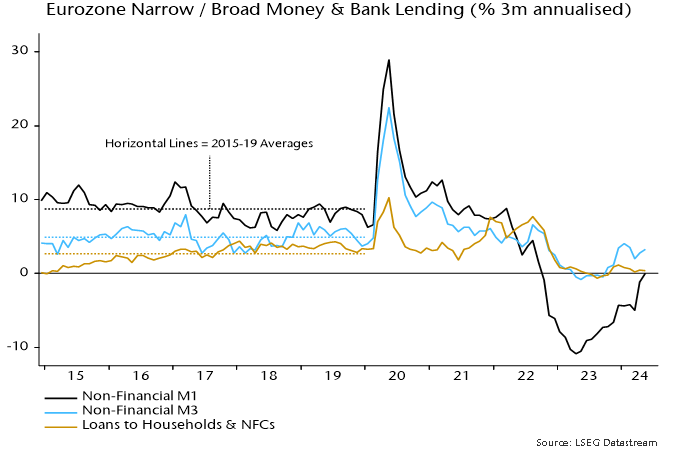

Three-month rates of change of narrow and broad money – as measured by non-financial M1 and M3 – were zero and 3.3% annualised respectively in May. Current readings are well up on a year ago but significantly short of pre-pandemic averages – see chart 1.

Chart 1

May month-on-month changes were soft, with narrow money contracting by 0.1% and growth of the broad measure slowing to 0.1%.

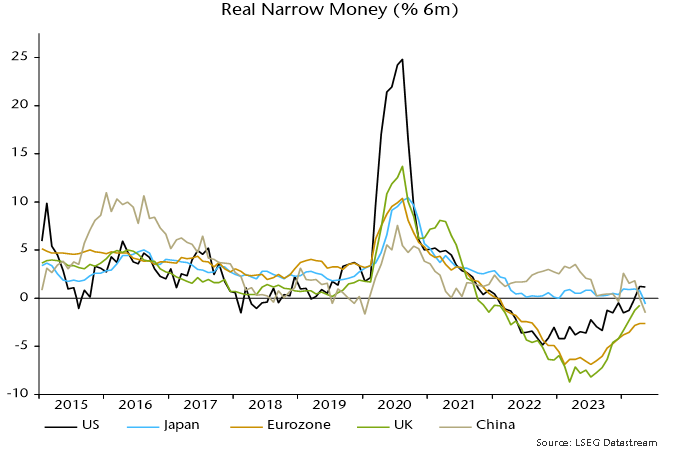

Six-month real narrow money momentum – the “best” monetary leading indicator of economic direction – moved sideways in May, remaining significantly negative and lower than in other major economies. (The latest UK reading is for April.)

Chart 2

June declines in Eurozone PMIs and German Ifo expectations may represent a realignment with negative monetary trends following a temporary overshoot – chart 3. A recent correction in cyclical equity market sectors could extend if Ifo expectations stall at the current level – chart 4.

Chart 3

Chart 4

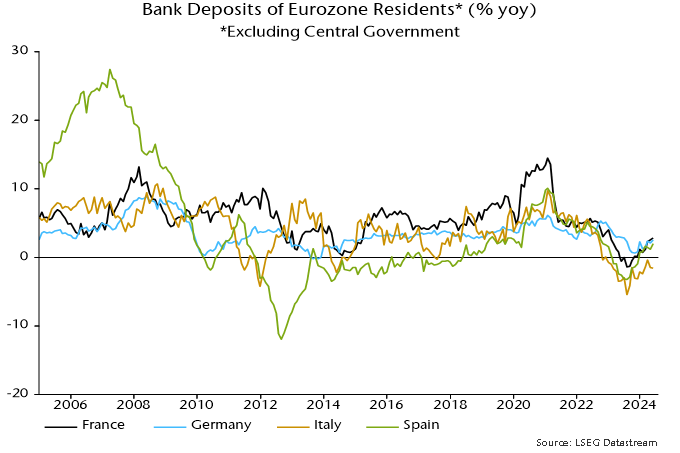

Growth of bank deposits is similar in France, Germany and Spain but lagging in Italy – chart 5. The country numbers warrant heightened scrutiny, given a risk that French political turmoil triggers deposit flight to Germany.

Chart 5