L’argent, le moteur des marchés

Is earnings momentum peaking?

27 mai 2026 par Simon Ward

An expected fall in global manufacturing PMI new orders suggests a moderation, at least, in current earnings strength.

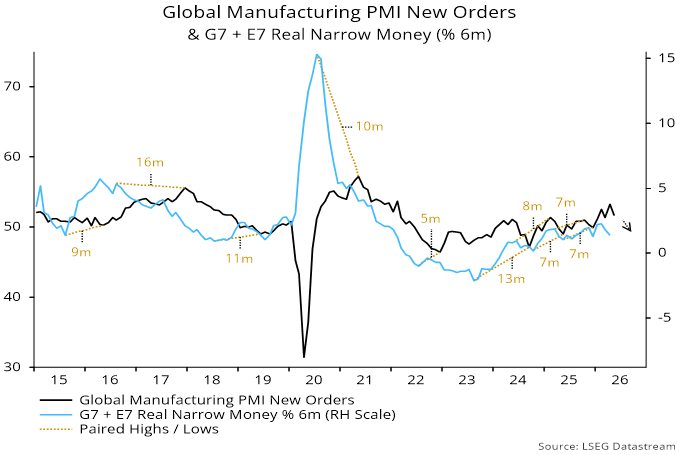

New orders reached a four-plus-year high in April but DM flash results imply a pull-back in May. The forecast here is for a further decline in H2, reflecting an inflation-driven slowdown in global six-month real narrow money momentum from a February peak – see chart 1.

Chart 1

A further consideration is that orders have been boosted recently by demand front-loading and stockbuilding motivated by supply concerns, implying future payback.

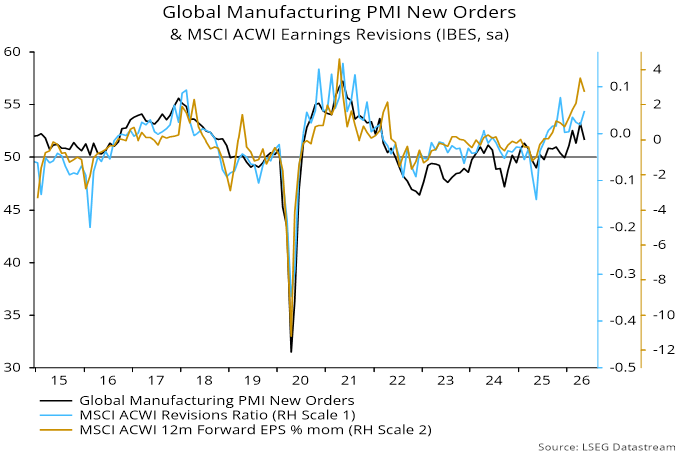

PMI new orders are contemporaneously correlated with MSCI World earnings revisions, whether expressed in terms of the revisions ratio (net proportion of analyst estimates upgraded each month) or the one-month percentage change in aggregate forecast earnings per share – chart 2.

Chart 2

Both revisions measures remained strong in May but the expected new orders decline suggests a moderation, at least, ahead.

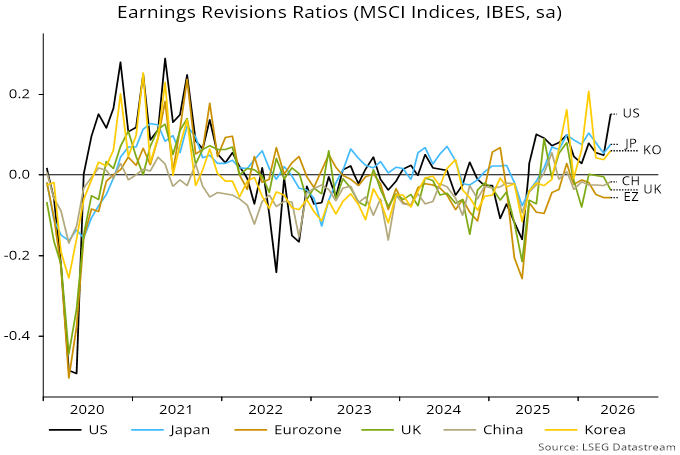

Current earnings strength is focused on the US and AI-spend beneficiaries, with downgrades in Europe, China and EM ex. Korea / Taiwan – chart 3. The suggestion of European relative weakness was echoed in the flash PMIs.

Chart 3

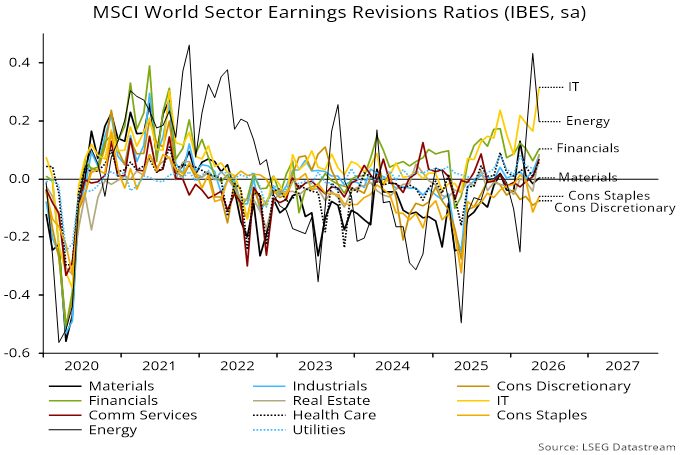

Sector wise, IT extended its lead, with consumer sectors continuing to suffer earnings downgrades – chart 4. The revisions ratio gaps between IT and consumer discretionary / staples reached new records in data extending back to 1995 – another manifestation of economic disparities.

Chart 4