L’argent, le moteur des marchés

Global money update: US relative strength

31 juillet 2025 par Simon Ward

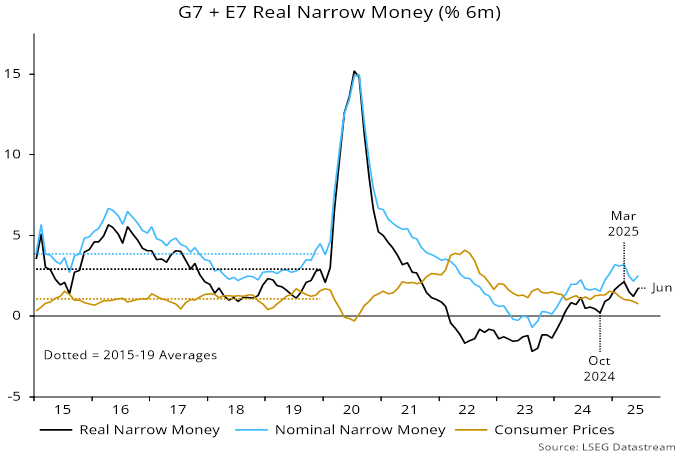

Global (i.e. G7 plus E7) six-month real narrow money momentum – a key indicator in the approach followed here – recovered in June but remains below a multi-year high reached in March.

The June rise reflected a small rebound in nominal money growth combined with a further fall in six-month consumer price momentum, to its lowest since 2020 – see chart 1.

Chart 1

CPI momentum is now below its 2015-19 average, vindicating the « monetarist » forecast that global inflation would fully reverse its 2021-22 spike once the ridiculous – but thankfully temporary – policy-driven money growth surge of 2020-21 had passed through the system.

The rise in six-month real narrow money momentum into March suggested that global economic growth would strengthen into late 2025, following a weak start to the year related to a monetary slowdown into October 2024.

Front-running of US tariffs, however, may have supported growth during H1, with H2 payback liable to dampen the expected pick-up. The March peak in real money momentum, meanwhile, suggests economic deceleration from late 2025.

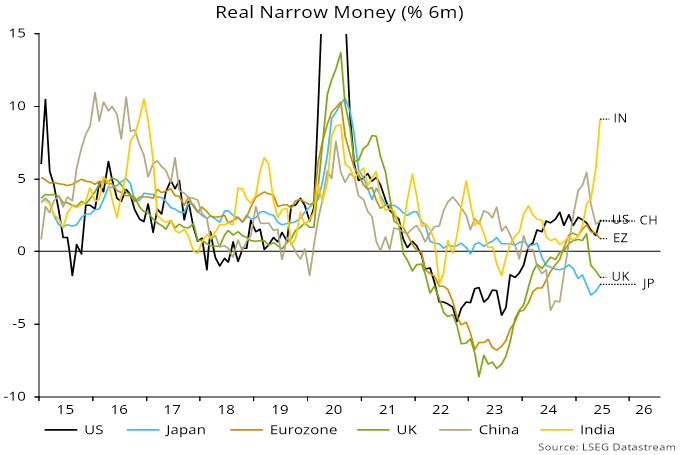

The June rise in global real money momentum was driven by a further pick-up in India following a dovish RBI shift coupled with a surprise rebound in the US. By contrast, Eurozone momentum slowed for a third month while UK contraction intensified, almost catching down to Japan – chart 2.

Chart 2

Interpretation of recent US money numbers is clouded by disruption to fiscal financing from the delay in lifting the debt ceiling. An associated run-down of the Treasury’s cash balance at the Fed may have supported H1 money growth, suggesting a drag as the balance is restored to its prior level.

(“Austrian” measures of the money stock include government deposits, on which basis US six-month narrow money momentum was negative in June. Such an approach is not endorsed here, for the obvious reason that – unlike for private sector agents – government money holdings are unrelated to future spending.)

Still, recent sideways movement of US six-month real narrow money momentum versus a slowdown in the Eurozone and outright weakness in Japan / the UK suggests improving US relative economic prospects while casting doubt on forecasts of further equity market underperformance.