L’argent, le moteur des marchés

Global money update: EM strength

27 novembre 2025 par Simon Ward

Global money trends suggest that major economic weakness will be deferred until later in 2026.

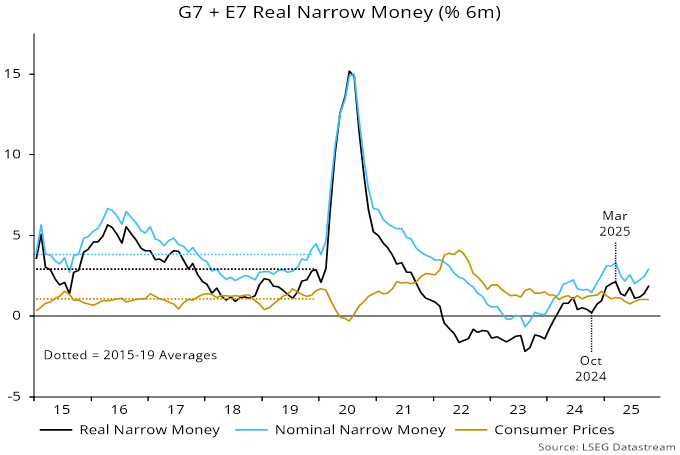

Six-month real narrow money momentum in the G7 and seven large emerging economies recovered further in October, almost returning to its March high – see chart 1.

Chart 1

The fall from March into the summer is expected here to be reflected in a slowdown in industrial momentum – as proxied by global manufacturing PMI new orders – into late Q1 2026. The recent money growth recovery suggests a partial PMI rebound in Q2 – chart 2.

Chart 2

The cyclical framework used here implies rising recession risk, with the stockbuilding and housing cycles in time windows to begin downswings. Monetary weakness would signal that a negative scenario is crystallising. The latest numbers appear to signal a delay.

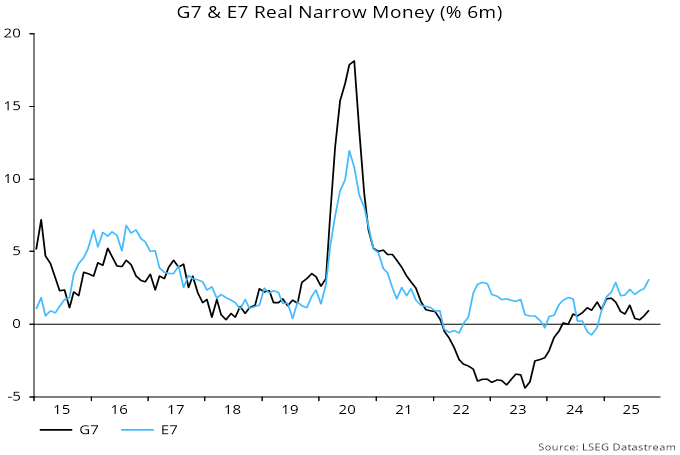

The composition of the money growth rebound gives pause. The return towards the March high has been driven by further strength in the E7 component, with G7 real money momentum lagging significantly – chart 3.

Chart 3

Narrow money trends are respectable or strong across major EMs, with the exception of Brazil – chart 4.

Chart 4

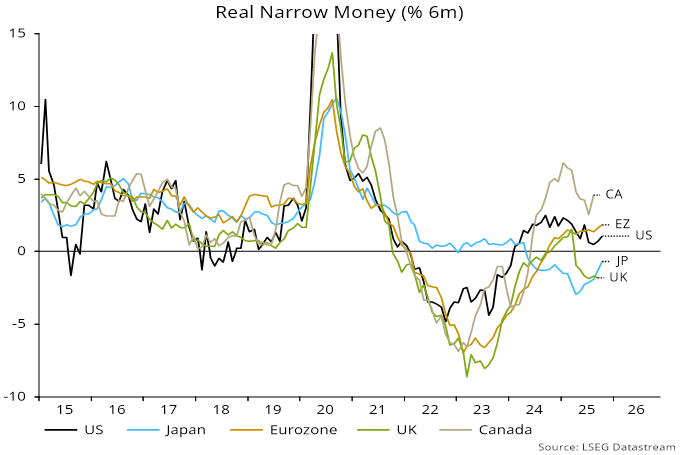

Soft G7 growth reflects a slowdown in the US and continued – though moderating – weakness in Japan and the UK. Eurozone momentum rose further last month, though remains unexceptional.

Chart 5