L’argent, le moteur des marchés

Eurozone money update: insufficient recovery

28 novembre 2024 par Simon Ward

Eurozone money trends are improving but remain too weak to support economic optimism, while country details highlight French stress.

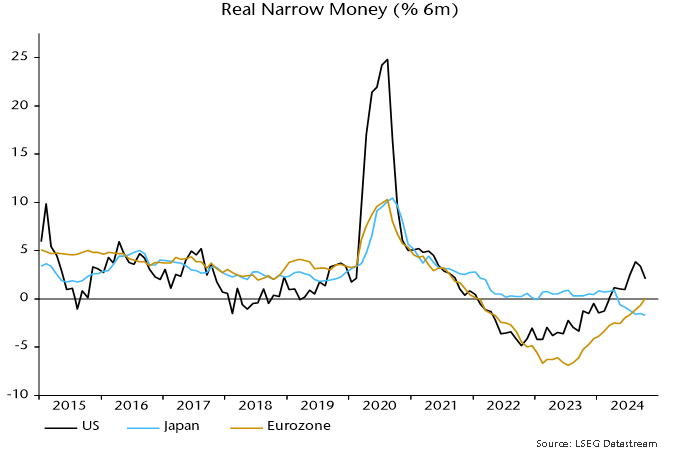

A post in June noted that six-month real narrow money momentum was still significantly negative, suggesting that a minor economic recovery in H1 2024 would give way to a H2 “double dip”. The PMI composite output index fell from 50.9 in June to a flash reading of 48.1 in November.

Six-month real money momentum has risen further since June but was still barely positive in October. It has, however, crossed above Japan and narrowed a shortfall with the US, implying improving relative prospects – chart 1.

Chart 1

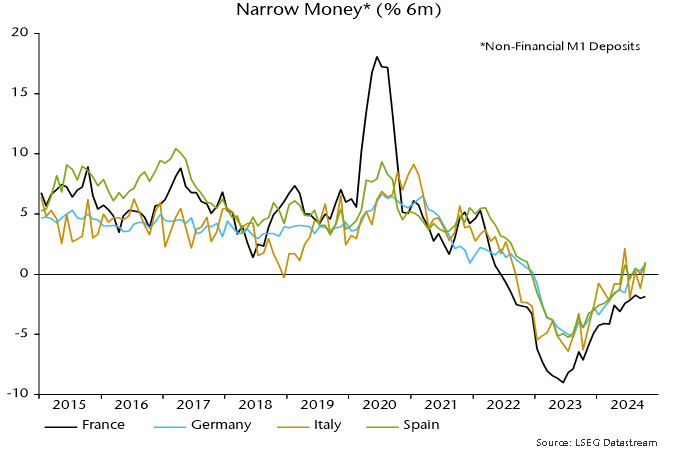

Consensus gloom about Germany may be overdone. Six-month nominal narrow money momentum has swung into positive territory since mid-year, catching up with Spain / Italy – chart 2.

Chart 2

French momentum, by contrast, remains negative, with a recovery stalling in September / October.

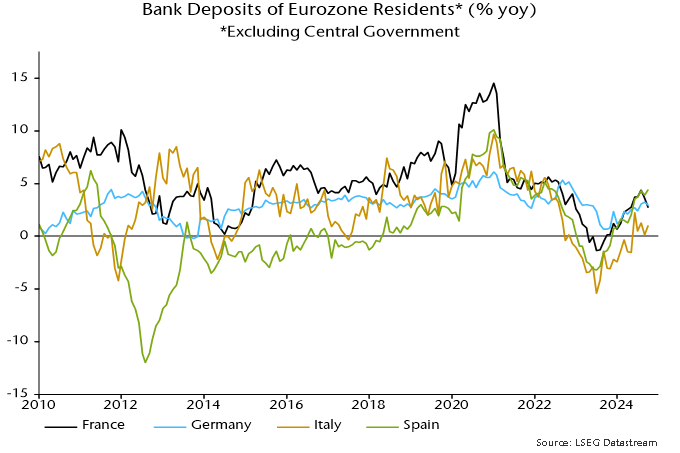

French narrow money weakness appears to reflect low confidence and spending intentions rather than deposit flight (so far). Annual growth of all bank deposits slowed sharply in September / October but is still on a par with in Germany – chart 3.

Chart 3

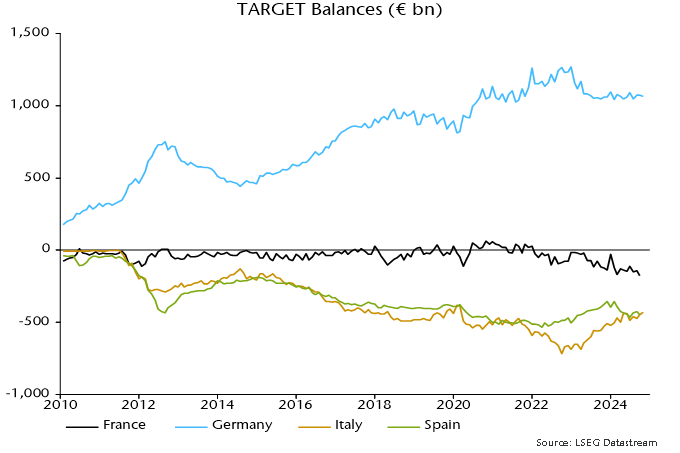

France’s deficit in the TARGET system rose by €34 billion in September to a record €175 billion, which could signal a capital outflow related to the political / fiscal crisis. There has, however, been no corresponding increase in Germany’s surplus, for which an October number is available – chart 4.

Chart 4