L’argent, le moteur des marchés

Eurozone money update: further softening

25 juillet 2025 par Simon Ward

June money numbers cast doubt on ECB President Lagarde’s assertion that policy-makers – and by extension the Eurozone economy – are “in a good place”.

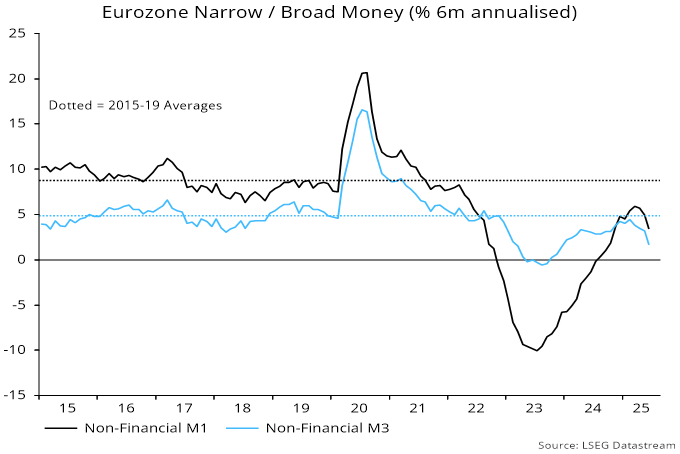

Six-month growth of the preferred narrow / broad money measures here – non-financial M1 / M3, comprising holdings of households and non-financial corporations (NFCs) – fell further to 3.4% and 1.6% annualised respectively last month. The latter is the slowest since December 2023 and compares with a 4.9% average over 2015-19 – see chart 1.

Chart 1

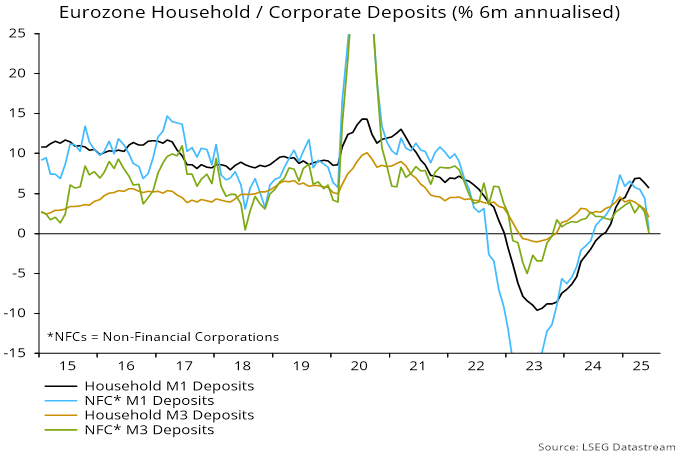

Weakness is focused on the corporate sector: NFC M1 / M3 deposits rose by only 0.5% and 0.1% annualised respectively in the six months to June, implying real terms contraction – chart 2.

Chart 2

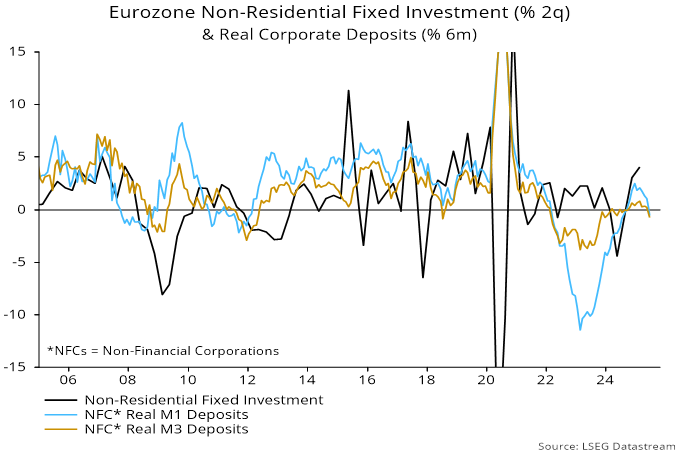

Corporate liquidity deterioration suggests that companies are under increased financial pressure and will rein in expansion plans – chart 3. A contraction in UK real corporate money preceded recent employment cut-backs.

Chart 3

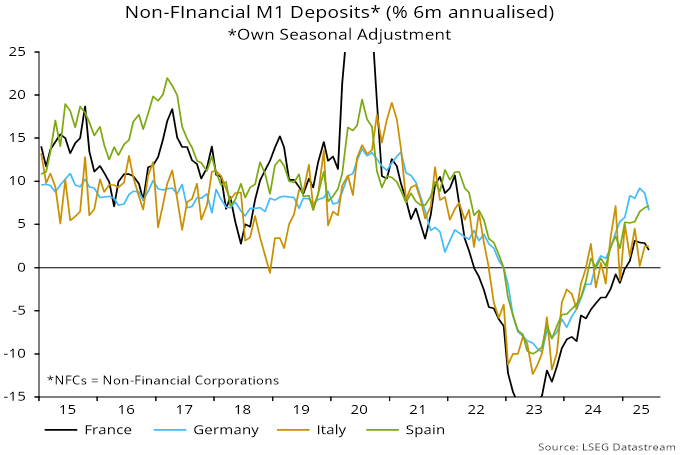

Six-month narrow money momentum is notably weaker in France / Italy than Germany / Spain, although German growth has fallen back since April – chart 4.

Chart 4

Consensus commentary focuses on bank lending, which, as an empirical matter, lags money trends. Adjusted loans to households and NFCs rose by a solid 0.4% on the month but six-month growth eased from 3.0% to 2.8% annualised. The “credit impulse”, in other words, may be rolling over.

Recent rate cuts are feeding through and it is possible that monetary weakness will prove temporary. Still, ECB officials should be concerned by the slowdown and signalling an openness to further easing rather than projecting complacency.