L’argent, le moteur des marchés

EM money update: India hotting up

18 juillet 2025 par Simon Ward

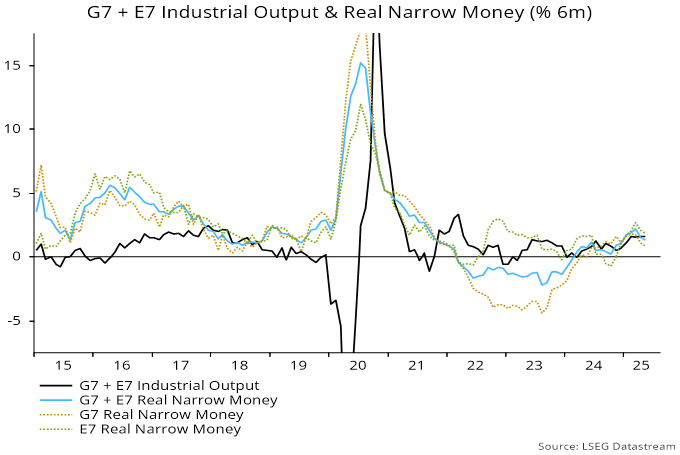

EM equities outperformed DM on average historically under two conditions, namely 1) global (i.e. G7 plus E7) six-month real narrow money growth was above industrial output growth and 2) real money growth was stronger in the E7 than G7. The first condition indicates a supportive global liquidity backdrop while the second signals stronger economic prospects for EM than DM.

Allowing for data reporting lags, these conditions were satisfied from end-February through end-June, a period during which MSCI EM outperformed MSCI World by 5.8%. However, the latest numbers, for May, show global six-month real money growth slipping back below industrial output momentum, although the E7 / G7 gap remains positive – see chart 1.

Chart 1

The suspension of the positive signal may prove temporary. Global industrial output has been boosted by front-loading to avoid higher US tariff rates, with payback likely during H2.

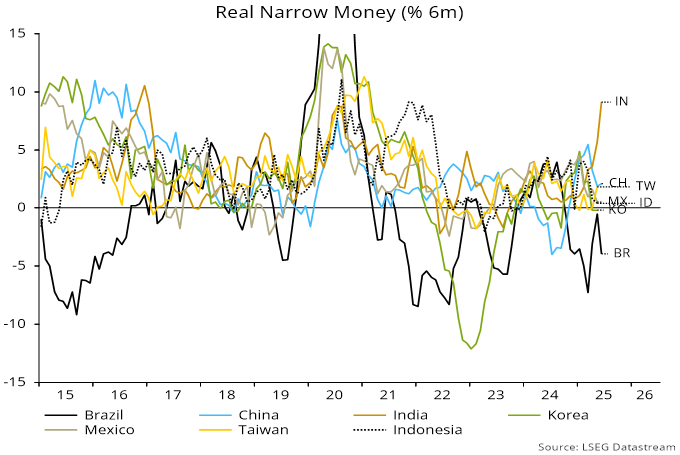

Chart 2 shows six-month real narrow money momentum in major EM economies and includes June data for Brazil, China and India. The stand-out recent development has been a pick-up in India in response to aggressive RBI easing, suggesting acceleration in an already strong economy.

Chart 2

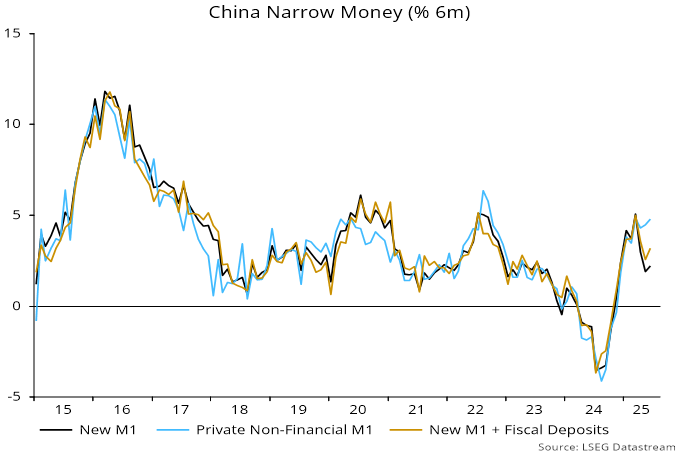

Chinese six-month momentum stabilised in June after falling in April / May. The series shown is based on the new official M1 measure, which includes household demand deposits and is close to the “true M1” definition historically used here. The June stabilisation followed a cut in reserve requirements in May and an associated further decline in money rates.

The Chinese slowdown since March is regarded here as of limited concern and likely to reverse, for the following reasons. First, there has been no loss of momentum in “private non-financial M1”, comprising currency and demand deposits of households and non-financial enterprises – chart 3. The aggregate slowdown appears to be attributable a fall in money holdings of government-related organisations and / or non-bank financial institutions.

Chart 3

Secondly, M1 excludes fiscal deposits, which have been growing solidly ahead of likely spending and / or transfers to government-related bodies. Momentum of an expanded aggregate including such deposits fell by less in April / May, recovering slightly in June.

Elsewhere. Taiwanese growth firmed in May and may rise further as currency strength forces the central bank to ease. By contrast, momentum has slowed in Indonesia, Korea and Mexico and remains negative in Brazil.