L’argent, le moteur des marchés

Defiant Fed forecasts

11 décembre 2025 par Simon Ward

The Fed’s economic forecasts continue to suggest that the window for easing will close in early 2026, according to a simple model of its historical behaviour.

Put differently, an extension of rate cuts requires either downside labour market and / or inflation surprises or a change in the Fed’s reaction function.

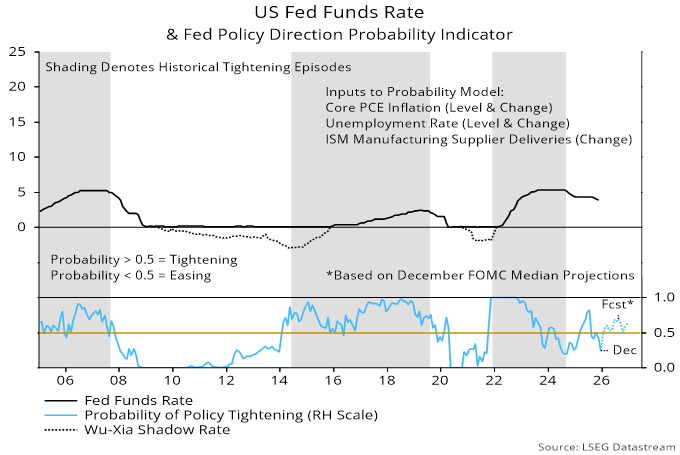

The model classifies the Fed as being in tightening or easing mode depending on whether a probability estimate is above or below 0.5. The estimate is based on currently reported and lagged values of core PCE inflation, the unemployment rate and the ISM manufacturing delivery delays index. Despite the small number of inputs, the model does a satisfactory job of “explaining” the Fed’s past actions.

The probability estimate fell below 0.5 in August ahead of the September rate cut and declined further last week, reflecting a sharp drop in the ISM component – see chart 1.

Chart 1

The December FOMC median forecasts for the unemployment rate in Q4 2025 and Q4 2026 are unchanged from September, at 4.5% and 4.4% respectively. Forecasts for annual core PCE inflation have been lowered by 0.1 pp, to 3.0% and 2.5%. The analysis here assumes smooth trajectories between the two quarters.

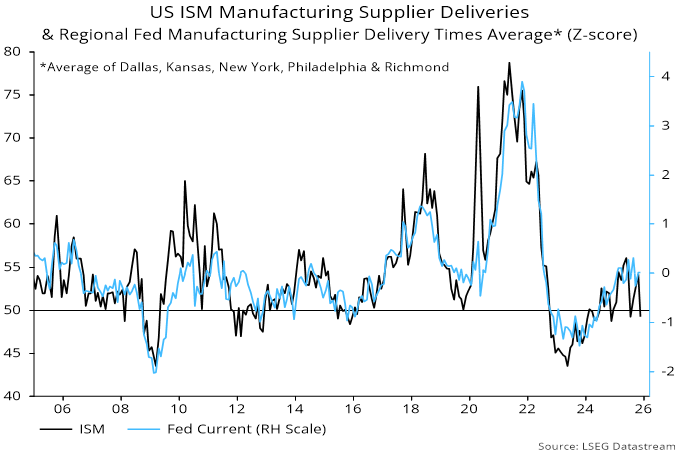

The model also requires an assumption for the ISM deliveries index. The December drop contrasts with mixed readings of equivalent components of regional Fed surveys, suggesting at least a partial reversal – chart 2. The projections assume a return to the Q4 average in January, followed by stability.

Chart 2

On this basis, the probability estimate rises in January and moves above 0.5 in February, climbing further into the summer.

The suggestion of an imminent end to the easing cycle is unsurprising given a central Fed view of a continued core inflation overshoot and a reduction in labour market slack.

A new Fed chair is unlikely to shift the reaction function without larger changes in the committee’s composition. The administration’s hopes of much lower rates will hinge on data.