Commentaires

Brazilian Blackjack revisited

20 août 2025

In our December 2024 commentary, we framed investing in Brazil as a high-stakes game of Blackjack. We argued that macro uncertainties such as fiscal deficits and political volatility were the low cards (2–6) which favoured the dealer. While these factors make for a daunting investment backdrop, our view was that these “cards” stood a chance of being dealt out as President Lula’s term progressed toward the 2026 elections. As a result, the proportion of high cards (10–Ace), being Brazil’s economic strengths and its reform potential, would start to rise and underpin an increasingly favourable set up for the player (investor).

Since our December post until August 2025, the deck has run down as October 2026 presidential elections in Brazil approach. As anticipated, the stakes are intensifying: Latin America’s 2025 electoral calendar is heating up, with presidential votes scheduled in Bolivia, Chile, Ecuador, and mid-term elections in Argentina, setting the stage for regional sentiment shifts that could influence outcomes in Brazil.

By the second quarter of 2026, we expect to have a good sense of the deck count and our chances of getting a Blackjack. It is likely that the “risk premium” for Brazilian equities has already peaked and will fall as early polls are released, candidates emerge and policy platforms take shape. This creates a unique window now for measured risk-taking as we await further confirmation on the above, selectively allocating chips (capital) to high-conviction hands where the asymmetry of risks favours the upside.

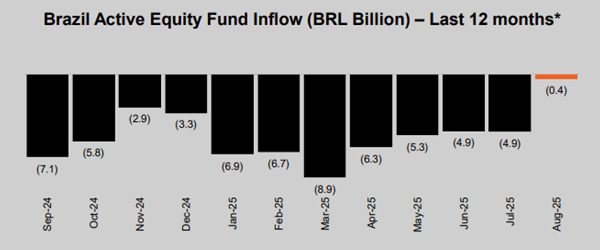

Active equity fund redemptions decelerate

Source: Itau BBA (August 2025)

So far, our approach has been assertive but disciplined: avoiding high-rolling bets on speculative names in favour of quality opportunities. This has paid off handsomely so far, typified by outperformance in portfolio holdings like Vivara (a jewellery retailer) and SABESP (sanitation utility), delivering strong returns amid a resilient economy.

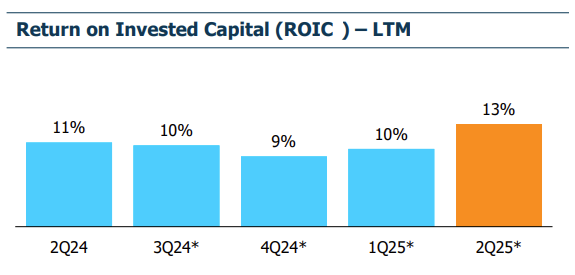

Brazilian water utility SABESP returns improving

Source: SABESP Q2 2025 investor presentation

Recent macro and political developments: Improving outlook, but risks linger

Since December 2024, Brazil’s economic resilience, despite the tension between tight monetary policy and loose fiscal policy, is undoubtedly a high card. GDP growth is moderating from 3.4% in 2024 to around 2.2–2.3% in 2025, as high interest rates start biting into activity. However, positives abound: unemployment hit record lows in mid-2025, inflation is easing (expected at 5.0% year-end) and the economy is positioned to weather Trump’s proposed 50% tariffs on non-US imports, thanks to exemptions for key commodities and diversified exports.

Politically, the deck is shifting favourably for investors seeking change. Lula’s approval rating has dipped amid unease over economic stability, with polls modelling runoffs showing him mostly behind right-wing figures like Tarcísio de Freitas (current governor of Sao Paulo State). Former president Bolsonaro himself is sidelined by legal troubles, reducing « anti-establishment » risks. The 2024 municipal elections saw gains for conservative candidates, signalling a potential 2026 swing toward market-friendly policies if a centre-right candidate consolidates support.

This echoes our original thesis: as Lula’s socialist term winds down, extreme pessimism over the economy should fade, creating a disconnect between strong company fundamentals and cheap equity valuations.

Core positions: Delivering as expected, with Q2 2025 earnings validation

Our core Latin American holdings have performed robustly, showcasing consistent top-line growth, improving returns (ROIC/ROE) and strong moats in defensive sectors. This validates our philosophy of steering clear of higher-risk names (e.g., leveraged cyclicals, where low margins and geopolitical exposure have led to underperformance amid prolonged high rates and global uncertainty). Initial signs of a softer local economy – for example, a Q2 retail slowdown – have hit speculative plays harder, reinforcing our quality focus.

The results from Q2 2025 underscore management prowess and support the view that our Brazilian names should be robust amid a volatile macro backdrop: top-line momentum (avg. +15% YoY) and ROIC/ROE improvements (avg. +2–3 pts). We are also excited about emerging opportunities as a “positive count” in the deck for Brazil, an opportunity to add some new names from our opinion list.

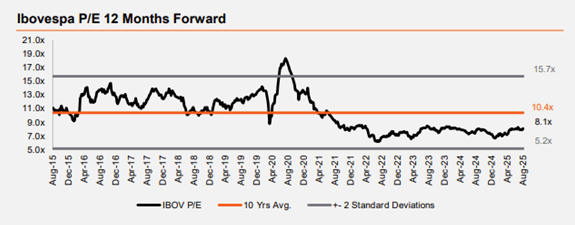

Valuations in Brazil remain attractive

Source: Itau BBA (August 2025)

In a couple of months, our planned trip to the region (with a packed agenda) will allow on-the-ground validation, potentially enhancing conviction in existing and prospective portfolio companies.

Outlook: Calibrating bets as odds shift

As inflation cooling and political fragmentation dissipating act as low cards exiting the deck, the count could tilt toward investors. For now, play smart; global headwinds (Trump tariffs and a US slowdown) and domestic fiscal risks could bust hands. We remain focused on quality amid depressed valuations and are keeping eyes on the 2026 Ace: a conservative presidential win that could unlock multi-baggers. Stay tuned for post-trip updates; this game is far from over.