L’argent, le moteur des marchés

Are equities stalling?

25 juin 2026 par Simon Ward

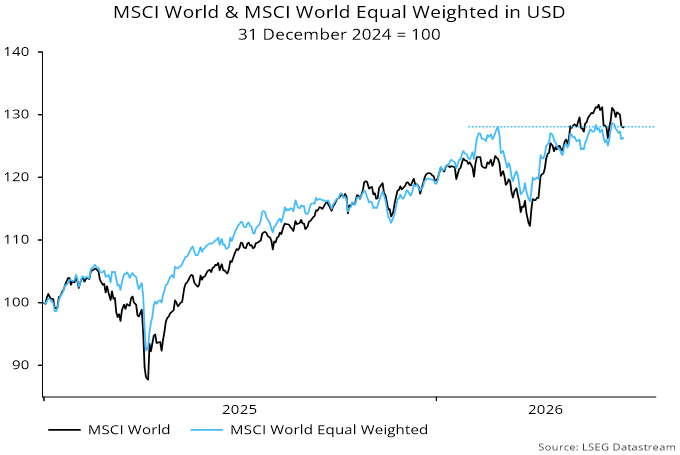

Global equities have lost momentum. The MSCI World index is little changed since mid-May. The equal-weight version of the index remains below a high reached in late February – see chart 1.

Chart 1

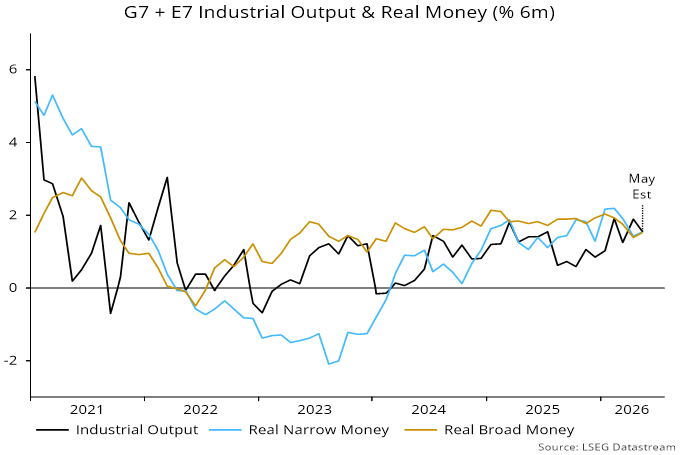

The stall could be explained by a less favourable “excess” money backdrop. Six-month growth of global (i.e. G7 plus E7) real money – on both narrow and broad definitions – crossed below that of industrial output in April. Narrow money growth was higher over August-March, while the broad money gap had been positive in most months since end-2022 – chart 2.

Chart 2

Real money growth rates appear to have recovered in May but may not have moved back above output expansion, based on partial information.

Prospects for a restoration of excess money support are mixed.

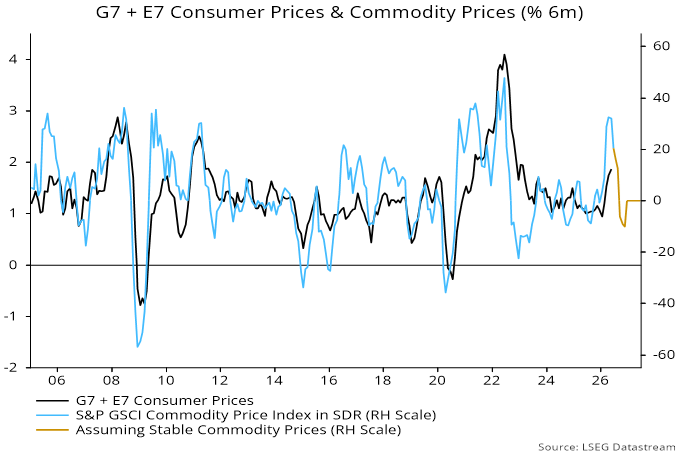

The real money slowdown reflected an energy-driven rise in six-month CPI momentum. This should reverse if recent commodity price relief is sustained – chart 3.

Chart 3

Yield curves, however, remain higher than before Gulf conflict, reflecting tighter actual and expected monetary policies. Higher rates could dampen nominal money growth.

Meanwhile, solid June flash PMI results suggest that six-month industrial output expansion will hold up near term.

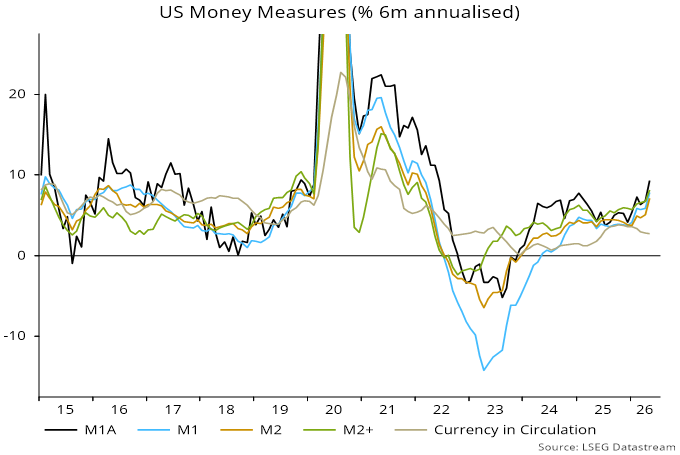

As previously discussed, global money growth has been supported recently by faster US expansion. Six-month growth of the preferred US narrow and broad measures here – M1A and M2+ respectively – rose further to 9.3% and 8.2% annualised respectively in May – chart 4. (The M1A series has been adjusted for a reclassification of some savings deposits as demand deposits in November.)

Chart 4

By contrast, six-month growth of Eurozone and UK broad money – as measured by non-financial M3 / M4 – was just 3.7% and 3.4% annualised respectively in April. May numbers are released next week.

The break-out of US six-month money growth above a January 2025 high coincided with a resumption of Fed balance sheet expansion. Chair Warsh wants to reverse this policy, suggesting a future downside risk to money trends.