L’argent, le moteur des marchés

Manufacturing roll-over?

06 novembre 2025

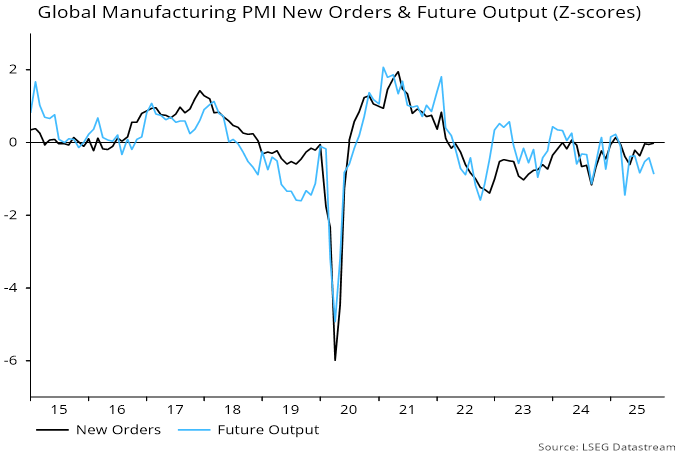

The forecast that global manufacturing PMI new orders will inflect weaker from a Q4 peak is supported by the “internals” of the October survey.

While new orders rose on the month, the increase was smaller than had been suggested by DM flash surveys, reflecting an EM decline led by China and Korea – often global bellwethers.

Firms were gloomier despite the orders uptick, with the future output index falling to its lowest since April in the wake of the “Liberation Day” shock. In contrast to new orders, this component is below its post-2015 average – see chart 1. (So is the corresponding services gauge.)

Chart 1

Pessimism may partly reflect an inventory overhang: indices measuring additions to stocks of purchased inputs and finished goods were in the 82nd and 97th percentiles of their long-run ranges (i.e. since 1998) respectively last month – more evidence that the global stockbuilding cycle is peaking.

Purchases of inputs boost orders of supplier firms. Accordingly, the new orders index is positively correlated with changes in the stocks of purchases index. The latter is likely to fall from its currently extended level. Even a stabilisation would imply a decline in the rate of change, in turn suggesting softer new orders – chart 2.

Chart 2

Global manufacturing deceleration is often associated with underperformance of cyclical equity market sectors. The price relative of MSCI World non-tech cyclical sectors versus defensive sectors ex. energy is below a September peak – chart 3.

Chart 3

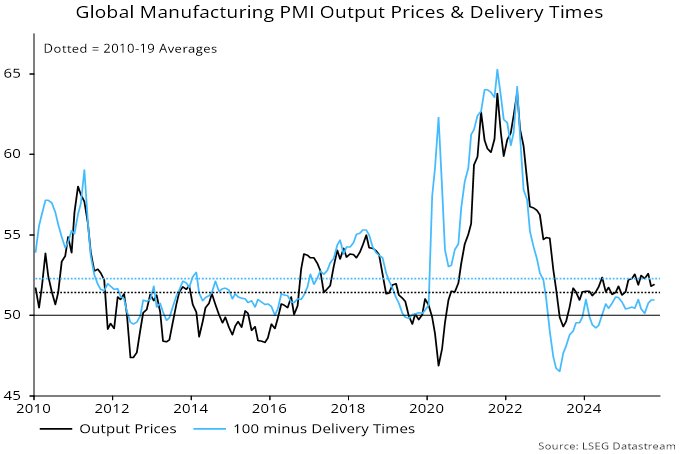

Cyclical earnings are more at risk when pricing power is weak. The output price index has fallen back and is close to its 2010-19 average, while delivery delays remain below the corresponding average, suggesting excess capacity and / or inventories – chart 4.

Chart 4