Commentaires

China trip: Key takeaways

15 novembre 2023

Summary

- EM equities fell over the month, with the MSCI EM Index down -4% over the period.

- Declines were led by markets with higher exposure to commodities and oil such as Latin America and the GCC.

- Quality stocks in China outperformed, while value names dominated by State-Owned Enterprises (SOEs) continued to cool following outperformance through the first half of the year. Chinese growth stocks remain laggards.

- Stocks in Poland rallied hard after former prime minister and European Council president Donald Tusk led a centrist coalition to victory in national elections, promising to restore ties with the European Union.

- Weakening narrow money momentum over the period suggests downside surprises to economic growth are likely. Our portfolio exposure remains defensive given this backdrop, underweight commodities and oil, favouring high quality and sustainably growing businesses that can weather a downturn.

- Unexpected economic weakness in the months ahead may force central banks to reconsider tight policy settings.

“It’s never too late to catch the China train – you can still ride the dragon to heaven.”

– Wang Jianjun, China vice-chair of the China Securities Regulatory Commission

Our team visited China and Hong Kong through September and October, seeing over 100 companies, policy makers, strategists and research analysts. The trip provided an opportunity to gauge sentiment on the ground and test our conviction on portfolio companies, while uncovering new risks and opportunities.

It’s safe to say that the team didn’t leave feeling quite as bullish as the vice-chair of China’s securities regulator at a conference we attended (quoted above). It remains difficult to build strong conviction for the longer-term outlook, but our sense is that a slow burn post-pandemic recovery is still in play. We were reminded by several Chinese executives that we are only a little over half a year into this recovery and that it will take time for green shoots to emerge.

Below is a summary of some key headlines which emerged over the trip.

Politics – domestic discontent evident while geopolitical risk stabilising

China’s economic slump marks the first real recession since reform and opening up under Deng Xiaoping in the late 1970s. What is notable is rising dissatisfaction spreading outside of investment circles, with frustration over a lack of visibility or conviction on economic policy direction bubbling up in the middle-class, entrepreneurs and elites. Current economic woes are increasingly blamed on policy missteps as opposed to unfavourable economic conditions.

Public mourning over the death of former premier Li Keqiang in early November provided an outlet for public venting of frustration. Mourners in Li’s home town of Hefei spoke about Li’s more moderate approach to politics, which has been interpreted by many China watchers as thinly veiled criticism of the more authoritarian turn political and economic institutions have taken under Xi.

While geopolitical risks stemming from Sino-US confrontation remain elevated, there are signs of stabilisation. Xi is set to meet US President Biden at the APEC summit in San Franciso in November. This follows dialogue between several members of the US administration and their Chinese counterparts, and an agreement between the US and China to prohibit the development of autonomous AI weaponry.

The CCP’s propaganda arm has also been hard at work. Chinese film Lover’s Grief Over the Yellow River (1999) has started airing on Chinese television recently. The plot centers on the story of a US pilot falling in love with a Chinese woman during the Second World War. It appears that the Party is seeking to keep a lid on anti-US and nationalistic sentiment ahead of the summit.

Source: Lover’s Grief Over the Yellow River, IMDB.

Consumption – fragile recovery remains intact

Trends are incrementally better than in the first half of 2023. Demand for leisure, travel and restaurants remains resilient and travel has exceeded pre-COVID levels. Tier-1/2 city shopping malls are very crowded on weekends, with long queues at popular restaurants. However, there are clear signs of consumption trade-down, e.g., fewer high-ticket item purchases, quiet high-end restaurants, and more subdued spending during online promotional seasons as we see platforms ramp up subsidies/incentives. Overall, consumption appears in line with our expectations and on track for a gradual recovery.

Property – momentum fading but the situation appears manageable

July’s Politburo meeting acknowledged the risks in the property sector and set off an improvement in the policy backdrop. The sector is looking less bearish on the relaxation of the downpayment ratio for property purchases and falling mortgage rates. These measures set off a temporary spike in secondary transaction data but it has since faded. Property prices have not yet reached a clearing price and market participants remain cautious. We found that those with more than one property are looking to sell, and those who want to buy now are only upgrading from their existing home. Speculative demand has evaporated.

Private developers are at risk of further defaults on offshore bonds but the government will not allow for onshore defaults (mainly via restructuring rather than outright capital injections). A systemic crisis appears unlikely, and the backdrop looks set to improve from here in T1/2 cities. Lower tiers will take significantly longer to recover.

Key themes

We found a lack of conviction generally among domestic investors in China, who are focused on high-frequency data and rotating quickly through sectors and stocks. Consensus buy and hold names were rare, and while the SOE reform story had been a popular trade in the first half of 2023, several portfolio managers we spoke to were broadly sceptical of these names. We agree that low valuations and a lack of momentum in other areas are unlikely to be sustainable drivers for these stocks.

While the sentiment among investors remains flat, there are several compelling trends that are likely to shape China’s investment landscape in the years to come.

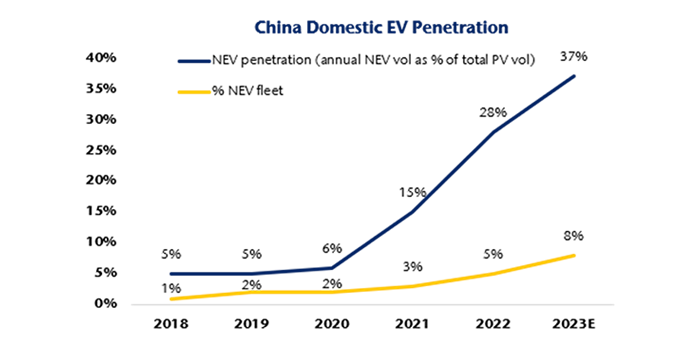

- EVs – Chinese specialist EV makers (BYD in particular) are playing a different game to the rest. EV penetration of new car sales is already at nearly 40% in China, offering competitive pricing and the potential to go global (with the promise of higher margins in foreign markets).

Source: Bernstein Research, 2023.

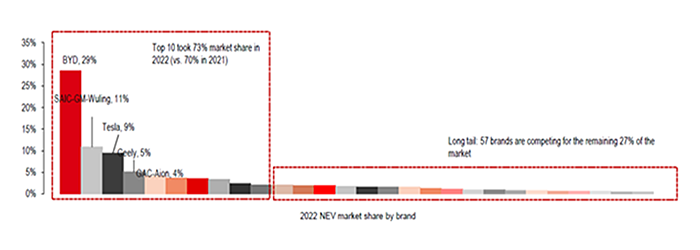

- BYD stood out as a company working so hard to play down expectations that their IR team almost seemed depressed! They are likely trying to tread softly as they push into more lucrative foreign markets, being very cautious in their communications on growth assumptions and deliberately vague on margin upside outside of China. The company is the dominant player in the mass market segment for EVs, and boasts 37% market share of NEV sales in China (Tesla in 2nd place with 10%, albeit targeting higher-end consumers).

- Risks include intense levels of domestic competition in a market that is due significant consolidation. On current trends, BYD and Tesla are looking like winners, at the expense of traditional international OEMs that have been slow to pivot to EVs.

Consolidation is on the way

Source: HSBC Research, 2023.

- Autonomous driving – Pony.ai is preparing for its IPO, fuelled by the excitement around partnerships with leading carmakers to incorporate its level 4 autonomous driving software. The aim is to produce the first large-scale robotaxi networks, with operations already running in Beijing and Guangzhou: China’s capital city is letting the public take fully driverless robotaxis – and has bigger rollout plans, startup Pony.ai says.

- Other themes include high-end manufacturing, industrial automation, semiconductor supply chain localisation, export-driven business in niche markets, as well as belt and road infrastructure.

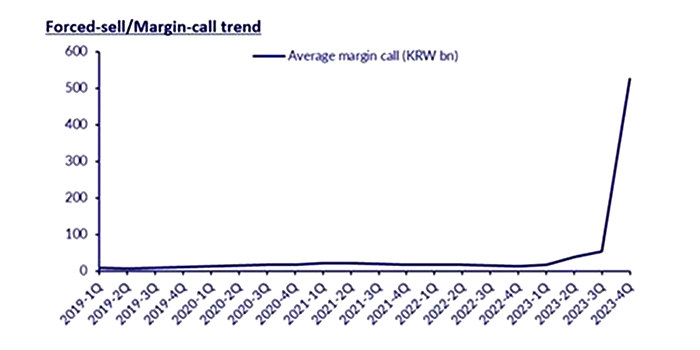

Korean stocks hit by a wave of margins calls

Korean stocks were also hit hard through the month, down -7% in USD terms in part due to forced selling/margin calls as brokers revised up margin loan hurdles. The margin calls exacerbated an already challenged environment for names in the battery supply chain which is working through a downcycle. Stocks favoured by retail investors such as battery materials producer Ecopro (down -31%) and steelmaker POSCO (which is investing in the battery supply chain, down -23%) unwound.

Source: CLSA, 2023.

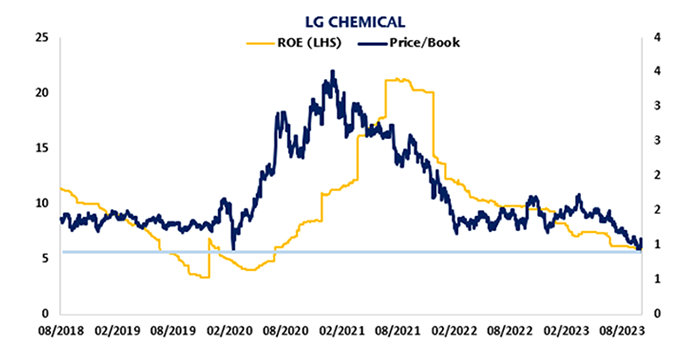

Our exposure to batteries is limited to Materials company, LG Chemical, and its subsidiary, LG Energy Solution, the world’s second-largest battery maker. While we don’t think battery makers are out of the woods just yet (especially as many of the key names are yet to make it through a full cycle since being listed), valuations in the sector are beginning to look tempting.

LG Chemical now trades at <1x price/book, which is its lowest valuation ever. According to JP Morgan, the company’s stock now trades at a 58% discount to its 82% stake in LG Energy Solution, while valuing its petrochemicals, advanced materials and biotech businesses at 0. Recent results also suggest operational performance might be approaching a bottom, with third-quarter results positively surprising. We are maintaining current levels of exposure while looking for more evidence of an upturn in batteries and petrochems.

Source: Bloomberg and NS Partners.

The oil price is telling you something

Brent crude finished October lower despite the outbreak of tensions in the Middle East following the October 7 attacks by Hamas against Israel. While risks of escalation remain, oil is looking like the dog that didn’t bark.

Does this tell us something about the global demand picture? Consumers are responding to high oil prices by curbing consumption, with demand for gasoline and diesel in the US falling.

It may also signal ample supply growth outside of the OPEC cartel. The shale boom continues in the Permian Basin, while the US is lifting embargoes on Venezuelan oil.

How much global production share will OPEC be willing to cede to competitors before abandoning supply discipline? We saw Saudi Arabia do exactly that during the COVID pandemic in response to Russia’s refusal to curb supply, which saw the oil price go negative.

This suits the US just fine, on a view that lower oil prices will squeeze opponents like Russia and Iran while easing inflationary pressures further.

Oil just one indicator of a deteriorating backdrop

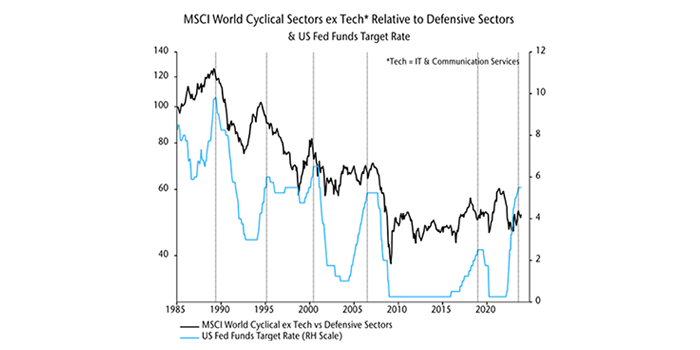

The global economy is likely to surprise to the downside while liquidity remains poor. The Materials and Energy sectors were weak through the month, in line with our view that cyclicals look vulnerable here.

Historically, while cyclical sectors can hold up over a short period following the conclusion of a hiking cycle, their underperformance over the medium term is stark. As our Chief Economist Simon Ward has pointed out, cyclical sectors underperformed following the last five US rate peaks, though not always immediately.

Source: Refinitive Datastream and NS Partners.

While the money numbers have been signalling downside risks to the economy for some time, other leading indicators, including consumer and manufacturing expectations, have slipped. Excessive tightening by central banks is now also feeding through to backward-looking data, such as unemployment and payrolls, which are starting to crack.

Are we on the cusp of central banks beginning to ease? Inflation has been rattling back globally, which is good news. However, in the absence of a financial accident (which is certainly possible given the liquidity backdrop), it has historically been the labour market that has prompted the central banks to start cutting.

{kind=link}

{kind=link}