L’argent, le moteur des marchés

UK inflation: “monetarist” optimism on track

19 novembre 2025 par Simon Ward

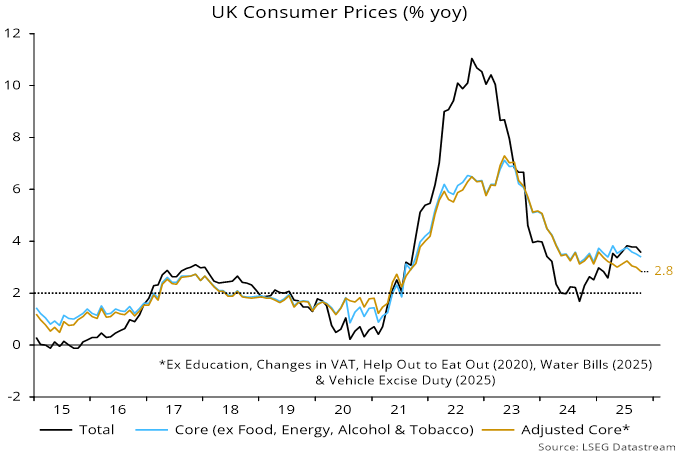

A measure of UK annual core CPI inflation excluding direct policy effects fell further to 2.8% in October, the lowest since August 2021 – see chart 1.

Chart 1

The measure adjusts for the imposition of VAT on school fees and bumper one-off rises in water bills and vehicle excise duty. It does not strip out the indirect impact of government actions, including national insurance and minimum wage rises and new packaging waste fees. The NI increase alone may have boosted annual core inflation by 0.25 pp, based on projections in the February Monetary Policy Report.

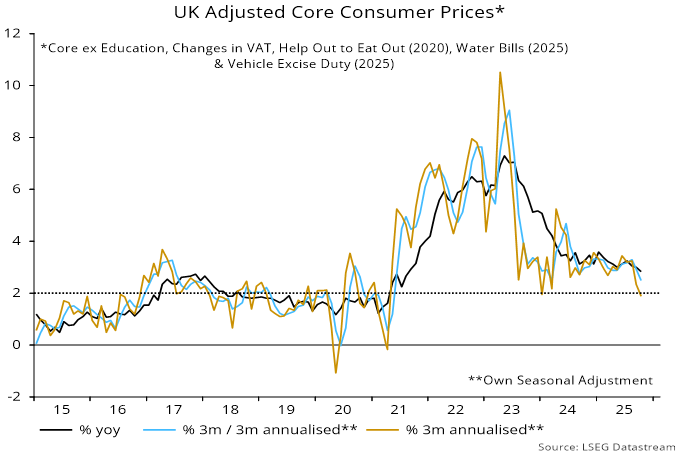

Policy effects are fading from shorter-term rates of change. The adjusted core measure rose at a 2.5% annualised pace in the three months to October from the previous three months, and by 1.9% between July and October – chart 2.

Chart 2

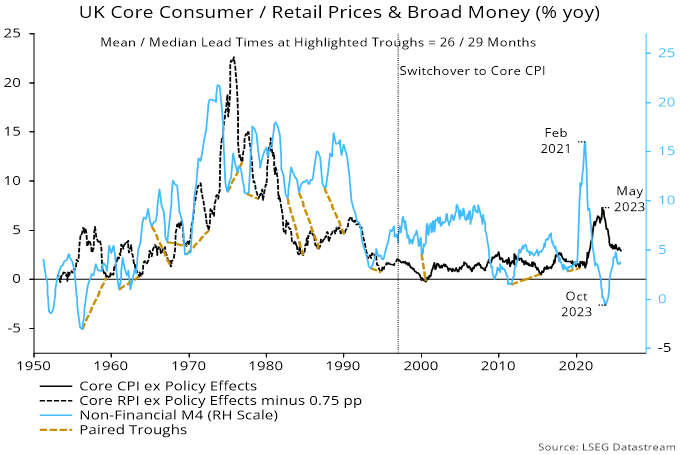

The core slowdown is consistent with lagged monetary trends, which suggest further deceleration in H1 2026.

Lows in annual broad money growth preceded lows in adjusted core inflation with mean and median lags of 26 and 29 months respectively since WW2. Money growth bottomed in October 2023, suggesting an inflation low between December 2025 and March 2026 – chart 3.

Chart 3

The indirect policy effects cited above may have delayed transmission, raising the possibility of a longer-than-average lag on this occasion.

Money growth, moreover, has remained weak since 2023, suggesting that low core inflation will be sustained into 2027, at least.

Beyond core, food inflation has remained sticky but could break lower in 2026. Annual food inflation of 4.8% in October compares with 1.9% in the Eurozone. Readings were similar at the time of the October 2024 Budget, suggesting that most of the current wedge reflects policy effects. Average UK food inflation was below the Eurozone level over 2015-24.

Based on plausible core / food assumptions, and assuming a neutral Budget impact, annual headline CPI inflation could fall to c.2.25% by Q2 2026 (versus a Bank forecast of 2.9%), with a return to target during H2.