L’argent, le moteur des marchés

Global money update: weak signal with US still diverging

30 octobre 2024 par Simon Ward

Global (i.e. G7 plus E7) six-month real narrow money momentum is estimated to have edged lower in September, based on monetary data covering 88% of the aggregate. Momentum has been moving sideways since the spring at a weak level by historical standards, suggesting that the global economy will expand at a below-trend pace through mid-2025 – see chart 1.

Chart 1

Note that the global narrow money measure incorporates an adjustment for a recent negative distortion to Chinese data from regulatory changes, i.e. momentum would be weaker than shown without this correction.

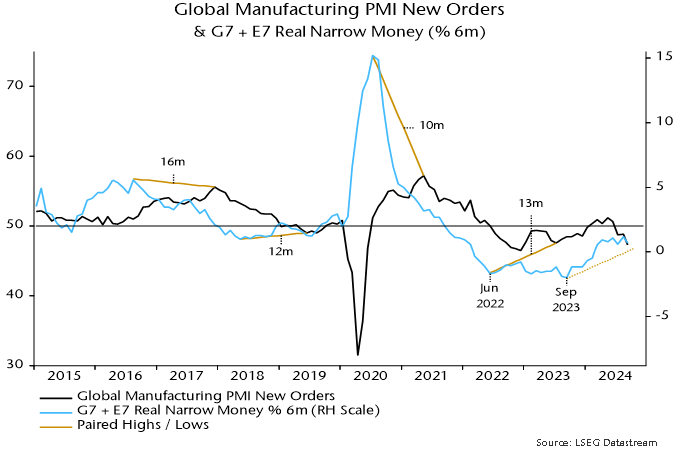

A low in real money momentum in September 2023 was expected here to be reflected in a decline in global industrial momentum – as proxied by the manufacturing PMI new orders index – into a low in late 2024. October flash results could be consistent with a bottoming out: PMIs fell in Japan and the UK but recovered slightly in the US and Eurozone – chart 2.

Chart 2

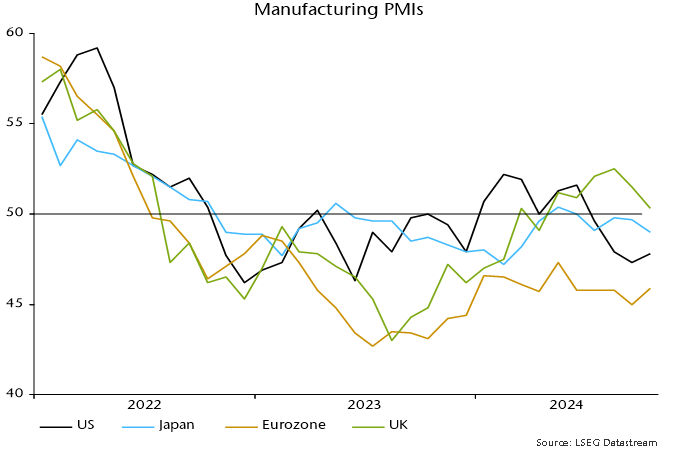

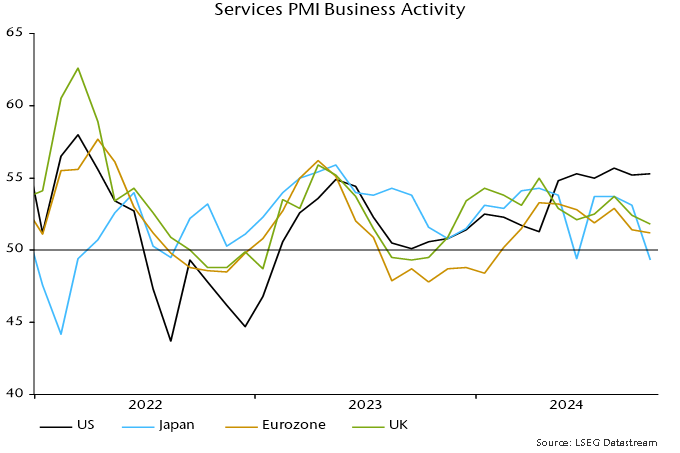

With money trends remaining weak, a manufacturing recovery into H1 2025 was expected to be limited and offset by a loss of momentum in services. Services business activity indices in the Eurozone and UK fell to 20- and 23-month lows respectively in October, according to flash results, with a sharper decline in Japan. US activity and new business indices, however, were strong, although the employment component remained sub-50.

Chart 3

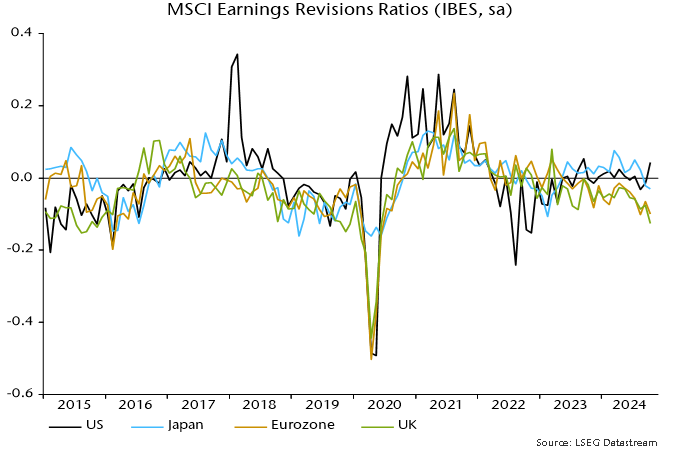

US relative strength is also evidenced by October earnings revisions ratios, with US net upgrades contrasting with weakness in Japan and Europe, particularly the UK – chart 4.

Chart 4

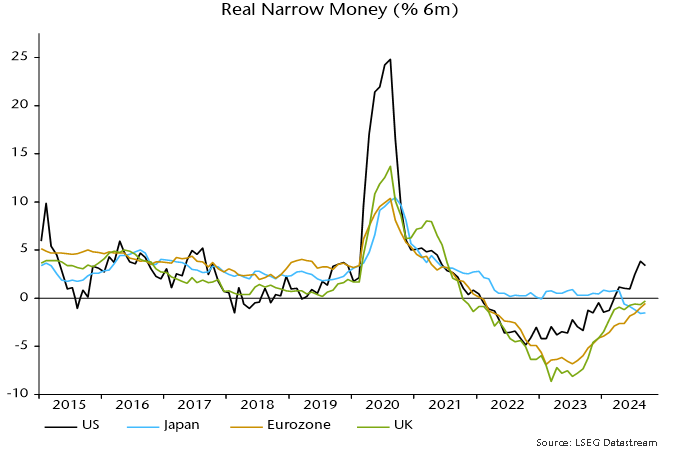

US economic outperformance is consistent with a recent wide gap between US and European / Japanese six-month real narrow money momentum. The expectation here was for a US pull-back in September due to an unfavourable base effect but this proved minor, with narrow money rising solidly again on the month – chart 5.

Chart 5

Eurozone / UK real narrow money momentum continues to recover but disappointingly slowly, suggesting a more urgent need for policy easing. A slump in Japan, initially due to f/x intervention but sustained by BoJ policy tightening, signals likely further negative economic news.

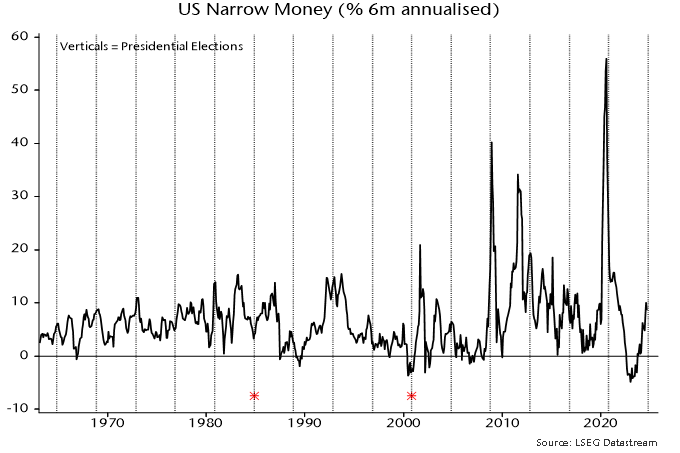

US narrow money acceleration started long before the September rate cut and hasn’t been mirrored by broader aggregates. One interpretation is that households / firms are accumulating “transactions” money in anticipation of increasing spending after the elections. Chart 6 suggests a tendency for narrow money momentum to pick up into presidential elections and reverse thereafter, with occasional notable exceptions (1984, 2000).

Chart 6