International equities finished 2025 strongly driven by positive Q3 earnings surprises, attractive valuations relative to the US and a risk-on environment, with the AI capex narrative continuing to dominate. The EAFE index rose 6.13% in local currency terms and 4.86% in US dollars. Utilities was the best performing sector, rising 10.13%, helped by expected higher energy demand from data centres worldwide and the long-term electrification trend. Communications was the weakest, with media earnings impacted by reduced advertising spending and telecom free cash flow pressurized by capex burdens.

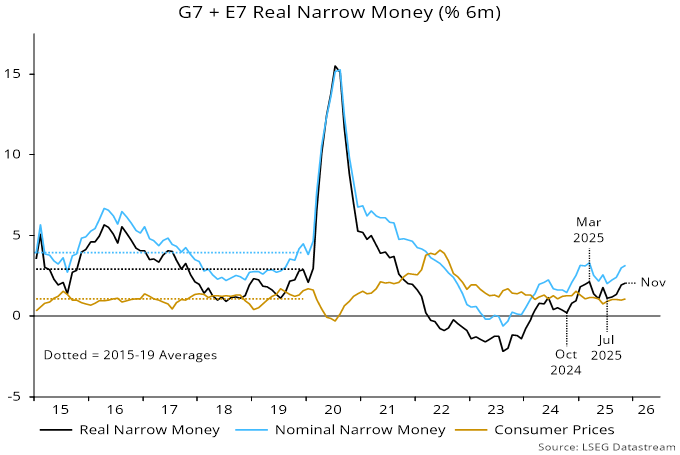

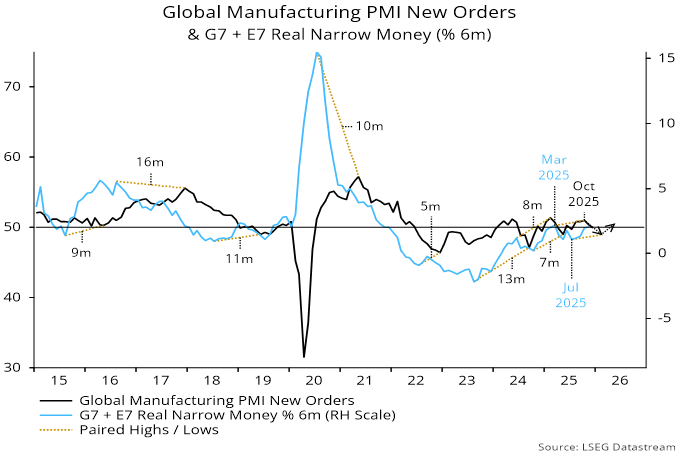

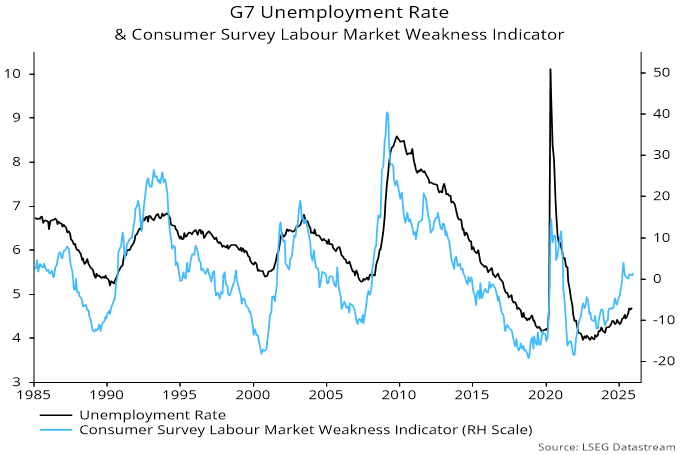

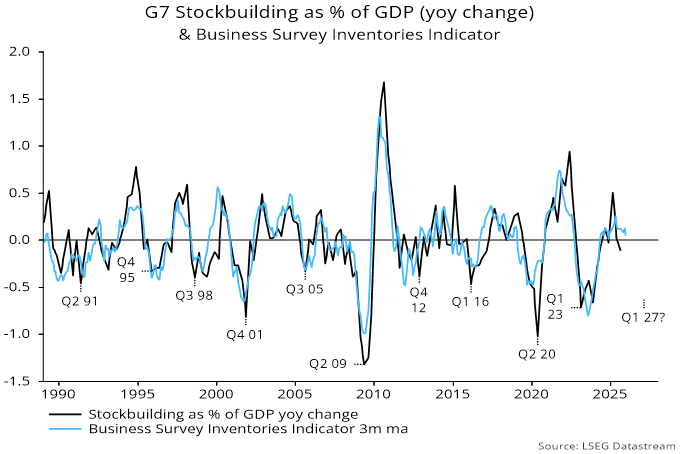

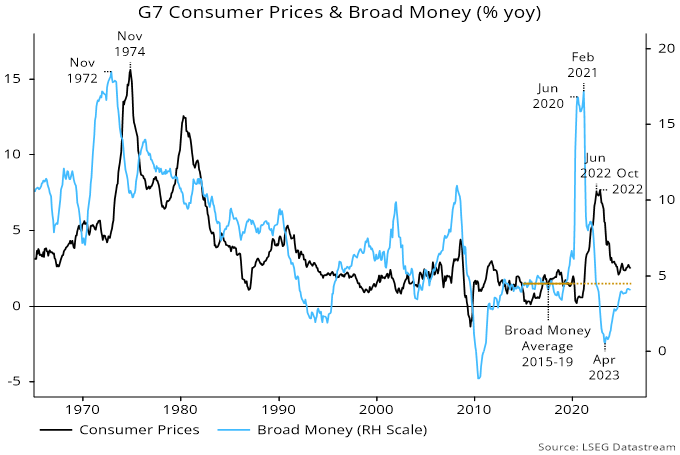

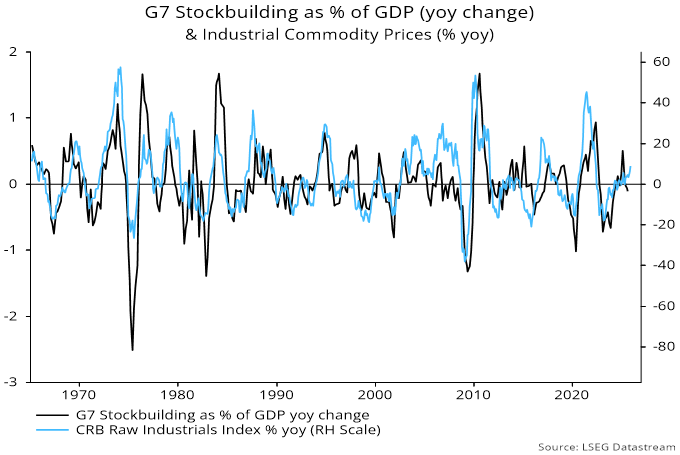

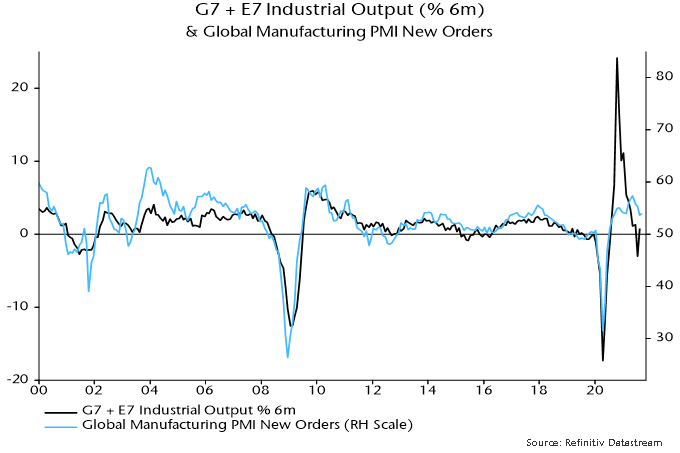

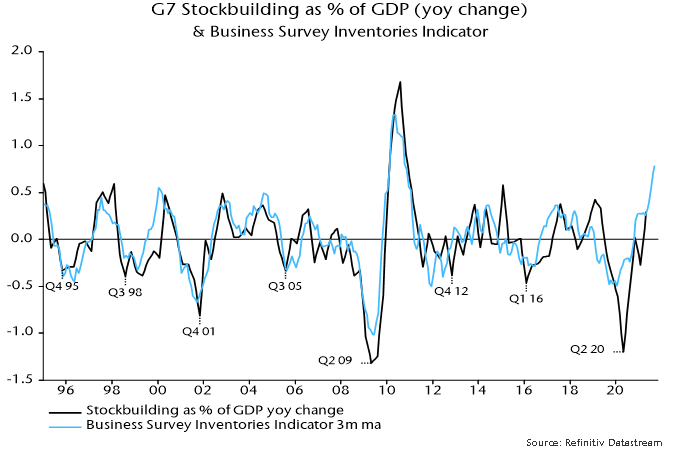

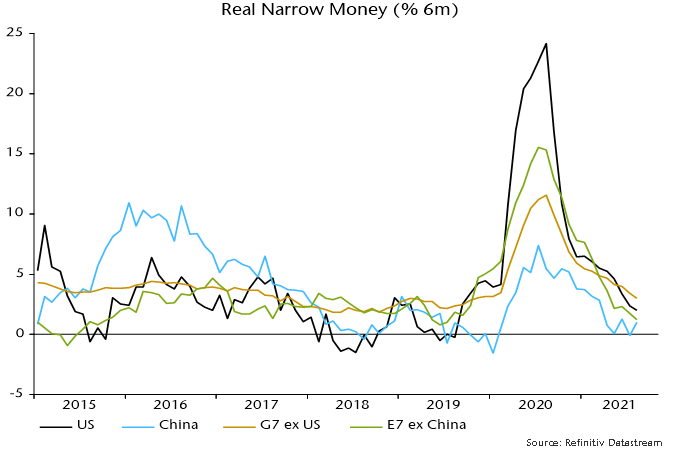

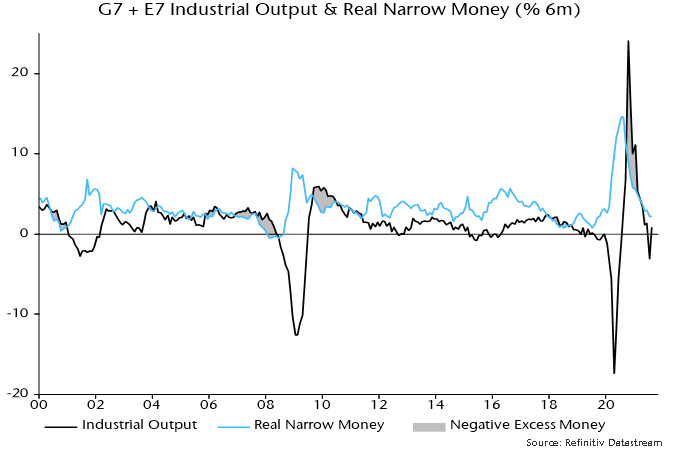

Global manufacturing PMI new orders fell for a second month in December, consistent with our forecast of a slowdown in economic momentum from late 2025, based on an earlier fall in real money growth from a March 2025 peak. Money numbers, however, have recovered since Q3, with EM growth reaching a new high. Accordingly, we now expect a PMI decline to bottom out in early 2026, with a recovery into mid-year. While global growth looks set to hold up in H1, this may not prevent a further rise in unemployment rates, partly reflecting AI job displacement. Moreover, the stockbuilding cycle remains on course to enter a downswing during 2026, suggesting another economic slowdown in H2.

The outperformance of Eurozone equities in 2025 was consistent with relative money trends, which remain favourable but less than a year ago – the money growth gap with Japan and the UK has narrowed. In Germany fiscal expansion focused on infrastructure and defence spending is offsetting weaker exports due to falling US demand and tariffs. In the UK uncertainty ahead of the November Budget against a backdrop of weak government finances weighed on consumer and business confidence. Inflation has undershot expectations allowing the Bank of England to cut rates but Chancellor Rachel Reeves has prioritised spending and deficit control over avoiding growth-damaging tax rises.

In Japan Sanae Takaichi became the country’s first female prime minister after leading her Liberal Democratic Party into a new post-election coalition. Her key policy aims are higher defence spending, investment in AI and nuclear power, lower interest rates and increased spending, representing a return towards the Abe playbook. However, the Bank of Japan has continued to raise interest rates as it ‘normalizes’ policy, although the Yen has remained under pressure, partly reflecting fiscal concerns. Rising Japanese bond yields could represent a global liquidity risk for markets in 2026 if Japanese investors repatriate funds attracted by higher domestic returns.

Stock selection was the main negative in both Japan and Europe. Performance was weak notably in industrials, IT, and consumer areas. Concerns about AI disruption continued to negatively impact UK-listed publisher Relx (-16%), UK online property marketer Rightmove (-28%) and Australian accounting software company Xero (-28%). Rightmove was also hit by an increase in investment, partly in AI tools, that will significantly impact margins. Meanwhile, Xero’s acquisition of Melio, a payments company, was viewed negatively: while accelerating Xero’s US growth ambitions, the US$2.5bln price was high and negatively impacts near term return on invested capital. In utilities UK power generator SSE (+24%) raised capital to increase network capex which should generate attractive total shareholder returns out to 2030. In materials, the rising copper price has driven Rio Tinto (+19%) higher while banks such as Caixabank (+17%) and Natwest (+23%) have continued to report well and the sector has been a standout multi-year performer within EAFE.

In Japan, food products and specialty chemicals company Ajinomoto (-28%) fell after weak Q2 numbers impacted by tariffs in the US, supply disruptions in Brazil and a timing mismatch in frozen food promotions. The hope is that these are one-off factors and management has maintained full year guidance but the market was skeptical. Japan Steel Works (-21%) was also weak as demand for petrochemical products has slowed in China while signs of progress in the Russia/Ukraine peace talks were viewed negatively. Other defence related stocks saw profit taking including Thales (-15%) in France and the unowned Rheinmetal in Germany (-23%) – the latter shows as a positive in attribution. The Japanese banks also fared badly versus their European counterparts with Rakuten (-22%) and Mitsubishi UFJ (-3%) both down despite the interest rate hike, with the market less confident about further rises after the more expansionary Prime Minister Takaichi came to power.

Activity over the quarter has moved the portfolio overweight the more defensive healthcare sector while reducing IT and industrials. We have re-introduced Swiss pharmaceutical giant Roche, which is growing its topline at ~6% and earnings at double digits for the next five years with upside potential from a strong drug pipeline. In financials UK-listed Standard Chartered has been bought, reducing the underweight in financials and bringing an attractive geographical exposure notably to Hong Kong and Singapore. The company is returning cash to shareholders, has strong local franchises in the fast-growing countries where it operates and is expanding its affluent wealth management business across its Asian footprint. We favour emerging markets as an asset class and have purchased Chinese multi-media giant Tencent which is benefiting from AI integration across its businesses and user base.

We have also added Swedish industrial equipment maker Atlas Copco which has returned to orders growth driven by semiconductor capex ramps. Atlas has suffered from its end markets such as automotive and construction stalling but the slowdown in growth can be reversed as interest rates fall and the valuation is attractive as key markets return to expansion. We have also purchased Japan Steel Works which operates in attractive areas such as defence, nuclear and power, but is on a valuation that has lagged other stocks in these areas. On the sell side in industrials we have reduced perceived AI-threatened business service companies such as UK-listed Relx and Experian, and taken profits in some defence-orientated stocks such as Thales and Safran, both in France.

2026 has been a challenging year for active managers with the significant underperformance of quality as a factor impacting fundamental stock pickers. The advent of AI as a major theme has negatively affected many of our favoured asset-light, high return companies across sectors in areas such as software and business services, while cyclical value stocks such as banks and defence-related industrials have enjoyed a significant re-rating.

We continue to view further market upside as limited given the maturity of the stockbuilding cycle – downswings are usually associated with underperformance of equities and other cyclical assets. Cyclical considerations similarly support our preference for quality, which may also act as a hedge against a recovery in the US dollar – sentiment and positioning are much less unfavourable for the dollar than a year ago. Our investment approach remains centred on high-quality, resilient businesses with durable competitive advantages and long-term growth potential. In the current market environment favouring speculative AI-related equities and interest rate-sensitive cyclicals, our strategy has lagged the broader index. We continue to monitor elevated valuations and capital deployment risks within the AI infrastructure space. Many firms are committing substantial investment with uncertain long-term returns. Should enthusiasm around AI moderate, we believe our portfolio is well-positioned to preserve capital and deliver attractive relative returns over time.

The Composite rose by 1.96% (1.81% Net) versus a 4.86% rise for the benchmark.