In February, we travelled to Saudi Arabia and Dubai to meet with a long-time holding in Jeddah, attend the second instalment of the Saudi Capital Markets Forum in Riyadh, and visit a newer addition to the portfolio in the United Arab Emirates (UAE).

1. Company visit in Jeddah

Our last research visit to Jeddah was in 2019, a time when the world looked remarkably different, and markets were not accounting for the successful execution of Saudi Arabia’s Vision 2030 transformation.

Located on the country’s Western coastline, Jeddah enjoys a more temperate climate and serves as both a gateway to the holy cities and a bustling commercial port. It has historically been more liberal than the capital, Riyadh, which has recently advanced at the forefront of the Kingdom’s social and cultural evolution.

The Saudia Dairy and Foodstuff Company (SADAFCO), established in 1976 in Jeddah, manufactures and sells Long-Life (UHT) milk, tomato paste, and ice cream under its flagship brand, Saudia. Leading the market in Long-Life Milk (64% market share), tomato paste (56%), and ice cream (31%), the company boasts strong distribution channels with three factories, 23 depots, and almost 1,000 trucks, generating annual revenues of $700 million.

SADAFCO factory, Jeddah.

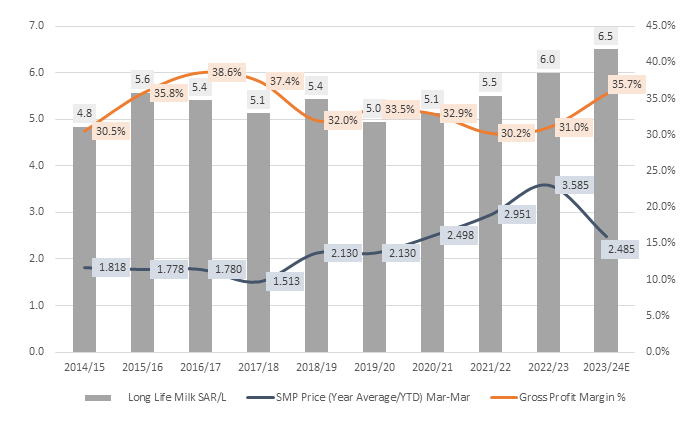

During our visit, we toured the ice cream and milk factories within the HQ compound, built in 2020 and 1976, respectively. Both facilities impressed us with their high levels of automation and operational efficiency, producing over 50,000 ice cream products and 10,000 litres of milk per hour. The company’s approach to reconstitute milk from skimmed milk powder (SMP) instead of producing fresh milk is advantageous in Saudi Arabia due to limited renewable water resources and recent subsidy removals on cattle feed. Water consumption for UHT milk production is significantly lower compared to fresh milk (under 1.9 litres of water per litre of UHT milk versus over 600 litres for fresh milk). Management have been proactively economising water usage through a water recovery system that collects hot water, cools it to an ambient temperature, and recirculates it in a closed system. This has led to savings of 45 million litres of water per year at an average cost of over $200,000.

Total water withdrawl/production volume

Source: Sustainability Report.

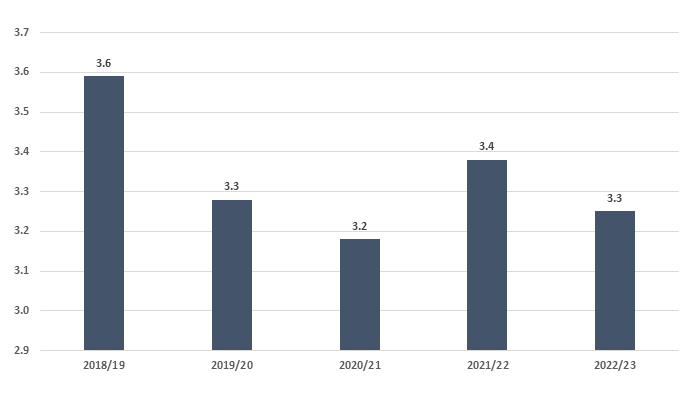

Competitors relying on fresh milk have seen their production costs increase, leading to pressure to raise prices. This situation, along with recent SMP price declines, has supported SADAFCO’s margins.

Gross margins vs. average SMP price vs. product prices

Source: Company, CIAL.

The business has diversified over the years, with the ice cream segment showing rapid growth and recent extensions into out-of-home (OOH) markets, doubling the potential addressable market. We are confident in the brand’s strength, the company’s wide distribution reach, and a strong management team focused on long-term value creation.

2. Saudi Capital Markets Forum in Riyadh

We spent three days in Riyadh, attending the second Saudi Capital Market Forum (SCMF), and conducting site visits across retail, fitness centres, and pharmacies.

The 2024 SCMF hosted twice the number of investors as in 2023, indicative of the growing interest in the market. Many participants were new to the country, and the diversity of the attendees was a notable shift from previous years. On recent flights to Riyadh, we have noticed more tourists visiting for music and sporting events, as well as creatives capitalising on the boom in media spending and domestic tourism – a distinct experience from past trips when we saw mostly business travellers and locals.

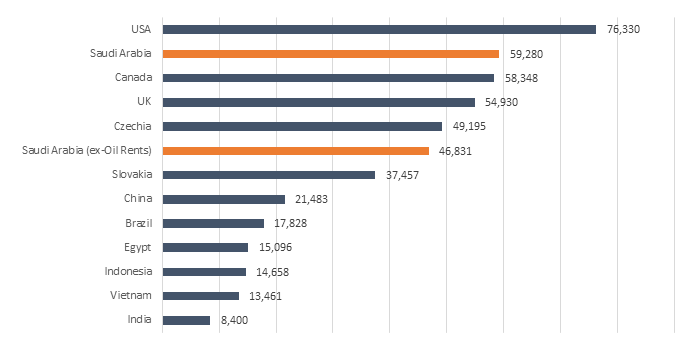

There is an appetite to accelerate the learning curve on the country given Saudi Arabia’s weighting in the Emerging Markets (EM) index and historically low involvement with the region. Saudi is not your typical EM, with a per capita GDP comparable to Czechia and Slovakia and a modest population of 36 million people.

GDP per capita (purchasing power parity)

Source: World Bank.

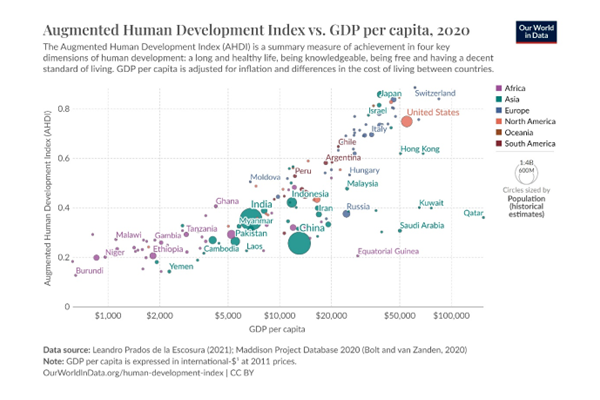

From a socioeconomic perspective, the country lags in terms of human development measures, especially relative to income per capita levels as shown in this chart:

Beyond the country’s cross-sectional nuances, there are well-documented economic and social changes taking place, underpinned by Vision 2030. Each of our visits to the country serves as a snapshot of the remarkable transformation taking place. Even with all the commentary about it, nothing compares to seeing the changes firsthand.

Notable developments in civil liberties include the dilution of the religious police’s power as early as 2016, allowing music concerts, female gyms, and cinemas since 2017, and 2018’s lifting of the ban on women driving. Whilst evident in 2019, it is only more recently that cumulative change alongside growing internal conviction in the country’s evolution have aided a lighter and more liberated atmosphere.

Female participation in the workforce has increased (up to 40% vs. 33% in 2016), impacting sectors differently. Since many women live with their husbands or parents, the rise in disposable income is largely discretionary. Concurrently, growth in leisure options is cannibalising the time previously spent in shopping malls. There is huge excitement for the tourism sector given the government’s willingness and fiscal capability to drive the industry. In healthcare and education, the government once held both regulatory and provisional roles, but is now focusing on the former and setting ambitious privatisation targets.

So, while the typical analyses of conventional EMs may not fully apply to Saudi Arabia, there are plenty of industries with promising growth prospects reflecting the leadership’s long-term goals.

3. Company visit in Dubai

Our final stop was Dubai, where we visited Taaleem, a recent addition to the portfolio.

Taaleem is one of the UAE’s largest K12 school operators, with 16,500 students across 14 private schools offering British, International Baccalaureate, and American curricula. Positioned in the ‘Premium’ market segment, with tuition fees from $15,000 to $20,000, Taaleem also partners with the government in operating 18 schools comprising 19,000 students, where the company earns fixed fees per student as well as variable fees based on academic attainment.

Greenfields International School (GIS).

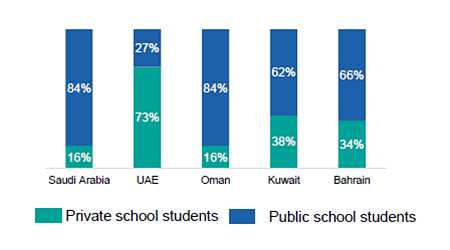

Unlike Saudi Arabia (16% private education penetration), the UAE has a high private education penetration, driven by a large expat population. The market is expanding, with private enrolments expected to reach 570,000 by 2027. The demand for high-quality schools is increasing as more expats establish roots in the country.

Private education market in KSA is still the lowest in GCC

Source: NCLE Presentation 1Q24.

We visited Greenfields International School, a 1,500 student International Baccalaureate (IB) school in Dubai Investment Park. A substantial proportion of the students are expats from within the region, yet the school is home to 75 different nationalities, reflecting the IB diploma’s broad appeal. Fees average $15,000 but vary widely, ranging from $8,900 for pre-school to $21,400 for the upper grades. Contributing 10% to Taaleem’s total revenues, the school (est. 2007) has improved its performance and ratings under new leadership.

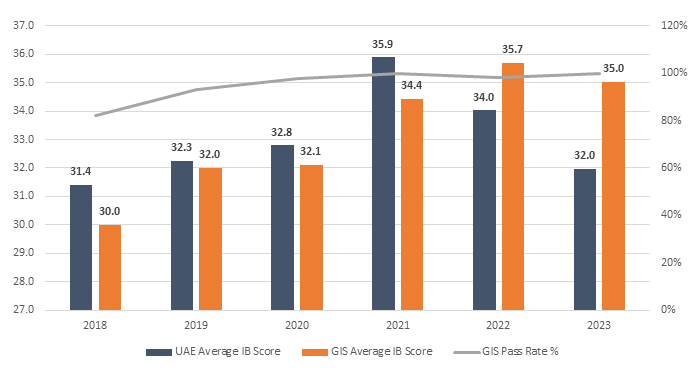

Historically, Greenfields underperformed the rest of Taaleem’s portfolio in Dubai’s Educational Ratings, earning a ‘Good’ and scoring IB exam results below the UAE average. Since a new Principal took over in mid-2021, IB scores and pass rates have improved, and the school’s rating is now ‘Very Good.’ Most recently, Greenfields was recognised as one of Dubai’s top-5 IB schools.

GIS average IB score & pass rate (%) vs. UAE average IB score

Source: KHDA.

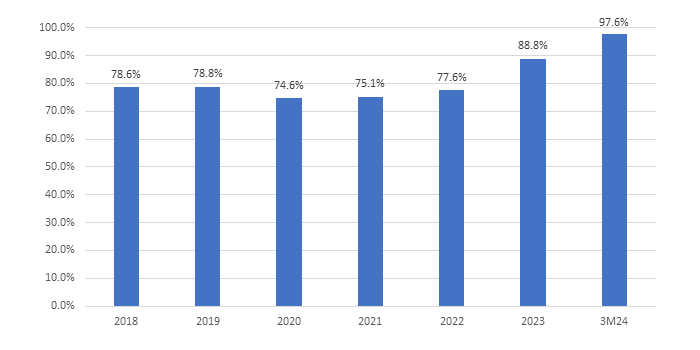

Our experience suggests that for private education providers, financial results often correlate with academic achievement and student/parent satisfaction. In the first quarter of this year, the school increased its utilisation rate to 98% from the mid-70% range pre-2023. Construction is underway to add 500 more seats for the next academic year and management feels confident about filling this increased capacity.

GIS utilisation (%)

Source: Company/KHDA.

We believe there is embedded average fee growth as the student base graduates to higher grades from pre-school. The main cash costs for the business are staff, and there is more interest from teachers in the UK and Europe due to lifestyle and earnings advantages. Taaleem benefits from government partnerships and is playing a role in improving education standards. Land is scarce in both Dubai and Abu Dhabi but as an education provider, Taaleem benefits from the government’s earmarking of space for schools and hospitals.

Despite potential risks, such as the UAE’s shifting appeal as an expat destination, we are confident in the quality-price ratio of Taaleem’s schools and expect them to be less impacted, so long as academic achievement and parent satisfaction remain high.

From the strides in Jeddah’s industrial sector to Riyadh’s evolving market landscape and Dubai’s educational innovation, our trip illuminated the swift changes and emerging opportunities within these economies and how tradition and modernity are coming together to shape the future.