Connor, Clark & Lunn Funds Inc. (CC&L Funds) is excited to announce the recent launch of a prospectus qualified version of the NS Partners International Equity Focus portfolio, which is now available to individual Canadian investors. The NS Partners International Equity Focus Fund is based on a similar portfolio, previously available only to institutional and internal investors.

The Fund seeks to provide investors with long term capital appreciation by investing in a portfolio comprised primarily of non-North American equities, including up to 20% in emerging markets.

To manage the fund, CC&L Funds has retained NS Partners Ltd (NS Partners) a London, UK-based manager with over 30 years of experience in managing international equity portfolios, including developed and emerging markets. NS Partners combines a bottom-up quality/growth framework to analyze companies with a unique top-down global liquidity analysis to help identify regions, countries and sectors that are expected to out and underperform, as well as whether to position the portfolio for a ‘risk-seeking’ or ‘risk averse’ environment.

“For investors allocated to large-cap global equity portfolios, there is a compelling case to make a stand-alone allocation to international equities, given the valuation and concentration issues in the large-cap U.S. equity market, and the headwind of a strong U.S. dollar. By introducing our NS Partners International Equity Focus portfolio in fund format, we can offer a compelling solution for individual investors, managed by a proven, institutional caliber investment team with a differentiated approach” said Tim Elliott, President and CEO of CC&L Funds.

“We’re excited that our International Equity Focus portfolio is being made accessible to a broader group of Canadian investors. With our proven process, a strong record on the institutional side and our talented and committed investment team, we believe this portfolio will provide an attractive solution for those seeking long-term growth from international equity markets.” said Tim Bray, President and Chief Investment Officer at NS Partners.

Both CC&L Funds and NS Partners are affiliates of Connor, Clark and Lunn Financial Group (“CC&L”), whose multi-affiliate structure brings together the talents of diverse investment teams who offer a broad range of traditional and alternative investment solutions. CC&L is one of Canada’s largest independently owned asset managers, responsible for over $104 billion in assets on behalf of institutional and individual investors.

About the fund

Available in A and F Series, the fund conforms with the regulatory framework related to conventional mutual funds offered by Simplified Prospects. The fund will be offered through licensed investment dealers, priced daily, with daily liquidity, and available through FundServ.

About Connor, Clark & Lunn Funds Inc.

Connor, Clark & Lunn Funds Inc. (CC&L Funds) partners with leading Canadian financial institutions and their investment advisors to deliver unique institutional investment strategies to individual investors through a select offering of funds, alternative investments and separately managed accounts.

By limiting the offering to a focused group of investment solutions, CC&L Funds is able to deliver unique and differentiated strategies designed to enhance traditional investor portfolios. For more information, please visit www.cclfundsinc.com.

About NS Partners Ltd

NS Partners Ltd is an independent investment management firm specializing in actively managed global equity portfolios on behalf of major companies, pension funds, foundations, endowments and sovereign wealth funds. NS Partners Ltd is part of the Connor, Clark & Lunn Financial Group, a multi-boutique asset management firm. For more information, please visit www.ns-partners.co.uk.

About Connor, Clark & Lunn Financial Group Ltd.

Connor, Clark & Lunn Financial Group Ltd. (CC&L Financial Group) is an independently owned, multi-affiliate asset management firm that provides a broad range of traditional and alternative investment management solutions to institutional and individual investors. CC&L Financial Group brings significant scale and expertise to the delivery of non-investment management functions through the centralization of all operational and distribution functions, allowing talented investment managers to focus on what they do best. CC&L Financial Group’s affiliates manage over $104 billion in assets. For more information, please visit www.cclgroup.com.

Contact

Lisa Wilson Manager, Product & Client Service Connor, Clark & Lunn Funds Inc. 416-864-3120 [email protected]

Gulf equity markets rolled over in the fourth quarter and materially underperformed emerging markets. This marks a stark but predictable (as we wrote in our last Q3 letter) reversal in fortunes, with tailwinds of the outperformance in the last 18 months turning to headwinds. We summarize the key drivers of the weakness in Gulf equity markets in the fourth quarter below:

Lower oil price and a different transmission mechanism – Gulf economies are highly levered to oil prices. While a Brent oil price of $80 is healthy for most Gulf economies, surpluses will naturally be lower as prices come down and barrels produced and sold remain static. Moreover, and focusing on Saudi Arabia, the share of oil revenue proceeds going into the banking system has come down considerably as the government allocates an increasing proportion of oil revenue to its sovereign wealth fund where the trickle down to economic activity is seemingly less visible (for now).

Higher interest rates – Gulf currencies are effectively pegged to the U.S. dollar and central banks have had to adjust to the Fed’s four rate hikes of 75 basis points in 2022. The relative attraction of owning equities with three months SIBOR rates reported at 5.59% is understandably low. Gulf investors have more alternatives than ever before to invest their money, with the recent Al Rajhi Bank Sukuk proving to be particularly popular among retail investors. Higher rates are also putting pressure on the net interest margins of banks as they compete to attract deposits. This phenomenon is likely to be especially acute in Saudi Arabia, where the liquidity environment has tightened n the fourth quarter of 2022. Saudi banks represent ~23% of most MENA indices and so the aforementioned profit margin compression has a material impact on the market’s aggregate EPS growth expectations for 2023. In other Gulf markets like the UAE and Qatar, state and quasi-state companies have been pre-paying debt at a rapid pace to avoid higher interest rates, leading to anemic corporate loan growth and further pressure on profitability.

Weaker USD – Gulf equities are effectively US dollar-denominated assets and are generally more attractive for global investors when the U.S. dollar is appreciating. This relationship has become stronger since Gulf equity markets became a large component of emerging market indices. Active Global Emerging Market (GEM) investors are not incremental buyers of Gulf equities in a weaker USD environment and their current underweight exposure to the region suggests they prefer to own assets denominated in non-pegged currencies.

Valuations – Gulf equity markets are coming off excessive valuation levels that reflected over-optimism on the degree and timing of the impact of reform program announcements, and robust foreign inflows following the deletion of Russia from the emerging market universe in March 2022, which we discussed in our second quarter letter.

A wall of offerings – 2022 was a record year for capital raised through primary and secondary transactions and the number of deals closed in the region with 47 listings raising a total of $26.5 billion. A large number of deals and the prospect of share sales by government and quasi-government shareholders took the air out of the market. We think it is wise for government funds to reduce or float their stakes in strategically listed companies given the level of ownership is far above what is required to retain control. However, this is likely to weigh on the share prices of many of the large-cap companies in the market where those entities are key shareholders. On a lighter note, overexcited bankers salivating at the prospect of fees from investment banking deals continue to be a reliable indicator of negative future market performance.

As for the strategy, we managed – to a large extent— to avoid the significant drawdown that the region experienced in the fourth quarter. Three factors helped us achieve this outperformance:

Sticking to high conviction portfolio companies like Saudi Dairy and Food Co. (SADAFCO) where management execution and weaker competition are leading to significant earnings growth that the market has been behind on for a few quarters now.

Adding to high conviction portfolio conviction companies that we believe are likely to experience an improvement in an operating environment like the National Company for Learning & Education (NCLE). NCLE’s eleven K-12 schools are experiencing a noticeable increase in utilization as students return to in-person learning in Saudi Arabia and management’s various initiatives (which focus primarily on quality of education in existing schools, M&A and greenfield for new schools) bear fruit.

Reducing or exiting portfolio companies we believe have reached valuation levels that are no longer attractive. A good example of this is Saudi Tadawul Group (STG), the country’s stock exchange which we exited at nearly peak average daily traded value. Over 60% of STG’s revenue is linked to traded values on the stock exchange and our exit decision reflected an understanding that traded values cannot just continue to go up, a view that the market is only getting around now as traded values have dropped 50% y-o-y in recent months.

We continue to see a strong opportunity for the strategy as the market begins to reflect the “bad news” in the price of assets we like, and as investments in companies we’ve made in the last 6-12 months or earlier continue to deliver.

While we acknowledge that the environment has been favourable for the strategy, and decisions we made have on the whole been good ones, we are not resting on our laurels and will endeavor to continue delivering differentiated value-added returns for our clients looking to access the growing investable opportunity in the MENA region.

Vergent Asset Management LLP

As this quarter marks the final letter for the year 2022, we thought it will be helpful to reflect on the key events that shaped the performance of the strategy in the year.

Economics

The war in Ukraine, and the resulting spillover into higher energy and food prices, exposed structural imbalances that resulted in spiraling inflation and currency depreciation across most markets. Our focus on African and Asian companies and through-the-cycle underwriting process put us at a disadvantage as food and oil prices experienced sharp and sustained inflation.

The consumer basket in our markets is over-indexed to those basic commodities, and the fiscal and balance of payment dynamics of most developing countries (where we exclusively invest) are inversely correlated to commodity prices. In response, we identified the most vulnerable countries in the portfolio and made decisions to exit two companies in Egypt and one in Pakistan, and selectively reduce exposure to Kenya. We highlighted in our third quarter letter that our portfolio companies experience a net positive carry in a higher rate environment, as most hold more cash than debt. Where there is debt, it is mostly in local currency or otherwise matched with foreign currency income. Of the top ten companies in the portfolio, seven enjoy a net cash position.

Despite active portfolio management that reduced exposure to the most vulnerable countries, and defensive portfolio attributes, returns were still dramatically overwhelmed by the impact of currency moves. Around 47% of the strategy’s returns in the year can be explained by foreign currency depreciation against the US dollar, with notable currency devaluation in the Egyptian pound, Pakistani rupee, and the Ghanaian cedi.

Politics

The strategy experienced volatility from the onset as political unrest in Kazakhstan in January led to a meaningful drawdown in the share price of Kaspi.Kz, a fairly sizable position for the strategy. Since then, Kazakhstan’s political outlook has materially improved. On the domestic front, Kassym-Jomart Tokayev secured a second term in a snap election held in November, cementing his position against political rivals from the previous regime. On the foreign policy front, Tokayev seems to have navigated the Russian-Ukraine crisis as well as anyone expected, striking a neutral position that preserved his country’s deep-rooted ties to Russia, while constructively increasing diplomatic and economic engagement with the West and China. Our team visited Kazakhstan in May where we visited with Kaspi.Kz management, their main bank competitor, and other relevant stakeholders. Our visit was instrumental in reinforcing our constructive thesis on Kaspi.Kz, which we then translated into opportunistic buying of the shares at what we deemed to be deeply discounted valuations. Fortunately, this helped turn a 38% drop in the share price of Kaspi.KZ in 2022 to a flat performance contribution to the strategy in the same year.

Kenya and the Philippines, key markets for the strategy, also held presidential elections this year. In Kenya, a peaceful election held in September saw power seamlessly transition to President-elect William Ruto, a testament to the democratic process, and the strength of institutions, in the East African country. President Ruto’s policy priority to reduce debt and improve Kenya’s fiscal position is negative for near-term growth but essential for sustainable long-term economic growth. His pro-trade stance, and his visit to neighbouring Addis Ababa for the national launch of Safaricom’s operations in Ethiopia, signal a commitment to preserving and expanding Kenya’s role as an economic and diplomatic hub for the region. It is worth noting that this political progress has not had the hoped-for effect on Kenyan equities, where weak macroeconomic conditions and dwindling stock market liquidity are prevailing. In the Philippines, Ferdinand Marcos Jr., the namesake son of the late dictator, was elected President in an election held in May. While many Filipinos are skeptical of Macros Jr.’s abilities and are understandably wary of his family’s history, his appointment of well-regarded technocrats in key economic roles has been a bright spot. While policy under Marcos, just like his predecessor Rodrigo Duterte, is probably going to remain uninspiring, it is fair to conclude that a Marcos presidency is, on the whole, positive for Filipino equities.

Earnings vs. Valuations

Reassuringly, earnings from key portfolio companies remained resilient in the year, reflecting elements of quality we expected when we underwrote those investments. We calculate that the strategy’s top 10 holdings experienced an average of 17% growth in revenue and earnings per share in the first nine months of 2022, compared to the same period in 2021. Even when there were setbacks in earnings, operating metrics were exceptionally strong for certain portfolio companies. Take Safaricom as an example; while EBITDA and EBIT were down 4% and 11% year-on-year respectively, the company’s M-Pesa ecosystem continued to grow from strength to strength, producing 32% growth in transaction volumes and signalling continued adoption by Kenyan consumers of M-Pesa in their daily lives. More importantly, most portfolio companies are guiding for a better year ahead, which bodes well for earnings visibility in the next six to twelve months.

With earnings being resilient and share prices coming down, multiples on the portfolio have come down to the level of ~10x Price to Cash Flow (P/CF). This multiple should be put in the context of a Return on Equity (ROE) that is well above 30% for the overall portfolio. This undervaluation has not gone unnoticed by the insiders of some portfolio companies; insider buying in the shares of Integrated Diagnostics Holdings in the third quarter, share buybacks from Kaspi.Kz in the last nine months, and a tender offer from Diageo for the minorities in East African Breweries in October (at a 30% premium) are all evidence of value recognition by the ultimate insiders.

Outlook

We are optimistic on the strategy’s performance in 2023. We highlight four key factors we believe can shape the outlook for performance:

With the U.S. dollar appreciation cycle potentially peaking, the pressure on currencies in most of our markets has abated, and we think it is unlikely we will see any meaningful negative contributions from currencies like the Indonesian rupiah, the Filipino peso, and the Moroccan dirham. In vulnerable countries like Egypt and Pakistan – where the strategy does not have much exposure— central banks are doing away with unhealthy currency management and letting market forces be the primary driver of the FX rate. This is a positive move that will open investment opportunities for the strategy in 2023.

Inflationary pressures have abated on food and certain commodities. While prices remain high by historical standards, we believe consumers, businesses, and governments have taken the brunt of the pain in 2022. The normalization of supply chains from the reopening of China should result in lower supply-side inflation and release the pressure on some of our companies to hold larger than normal inventory levels, which will increase cash conversion.

The domestic political picture is fairly stable after a busy 2022. This bodes well for policy visibility in 2023 and beyond. We expect policy to generally be pro-business and positive for equities. Looking forward, we expect the Indonesian general elections in February 2024 to be a positive catalyst for the strategy’s Indonesian portfolio in the second half of 2023.

The starting point for valuations is considerably low relative to the earnings power and visibility of portfolio companies. In other words, there is a fair amount of downside that is priced in. We are seeing insiders act on those valuation levels and consider that to be a strong bullish signal.

Finally, it is worth reminding readers that our objective is to deliver differentiated returns that can be attributed to the skill of investing (alpha) over the directionality of markets (beta). We believe there is an abundant alpha opportunity in frontier and emerging markets, which we choose to express through a concentrated but geographically diverse portfolio of companies with idiosyncratic earnings drivers and share price catalysts. Naturally, this should result in significant deviations from global and emerging market indices in certain periods, but hopefully provide a superior risk-adjusted return profile to investors in the long term.

As demand stays firm and China reopens, there will be growing pressure on central banks to hike rates further to contain demand. Inflation has just started to cool off in Europe, but levels are still elevated. Consequently, interest rates could stay higher than expected for some time.

Here are some observations following some earnings results that came out for Q4 (2022):

Q4 earnings and top-line growth declined sequentially but held up well, given the still solid demand and pricing.

Companies expressed more optimism for the global economy but were incrementally more cautious on margins levels, foreign exchange tailwinds and demand for 2023.

A lower proportion of companies mentioned having enough pricing power to pass on inflation in the short term.

Labour cost component is becoming the primary source of concern on the cost side, as supply chain and energy costs have come down considerably.

We believe that the old continent prospects look better than they appear. Some of the highlights and attractiveness of European companies include:

Forward price-to-earnings ratio

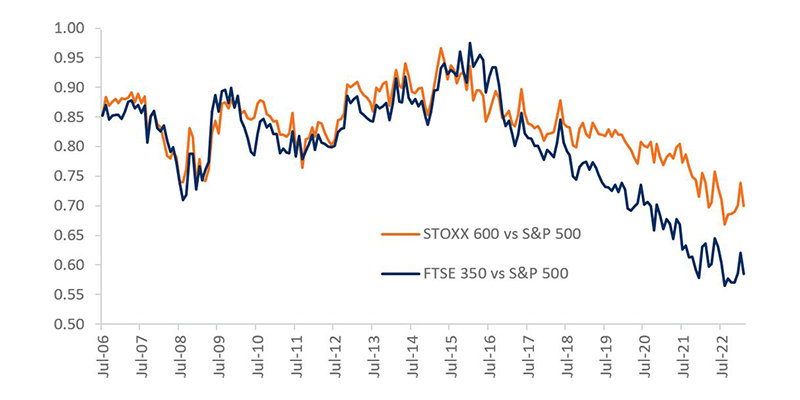

Forward price-to-earnings ratios for European companies have been attractive relative to the S&P 500. The discount has been even stronger for the UK FTSE 350 Index as shown below.

STOXX 600 and FTSE 350 12-month P/E forward relative to S&P 500

Source: Berenberg

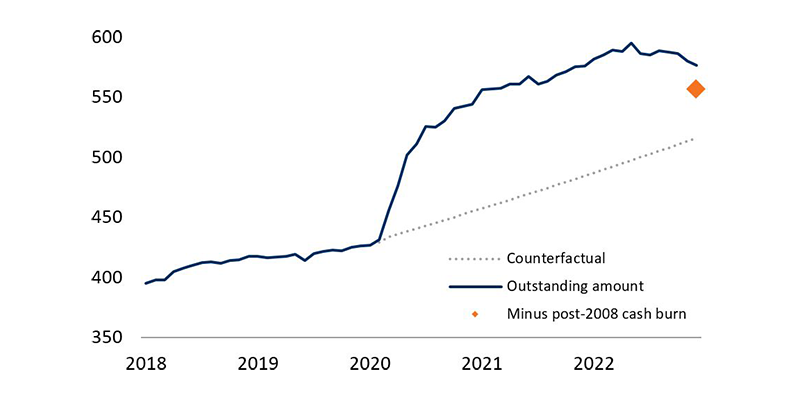

Cash positions

Cash piles have been quite considerable since the global financial crisis, and especially in the UK post-Brexit. Geopolitics and macroeconomics have pushed UK companies to increase their cash positions to more than £576 billion at the end of 2022. We believe that once confidence returns, capital spending should resume.

Deposit of UK non-financial institutions (£bn)

Source: BoE, Berenberg

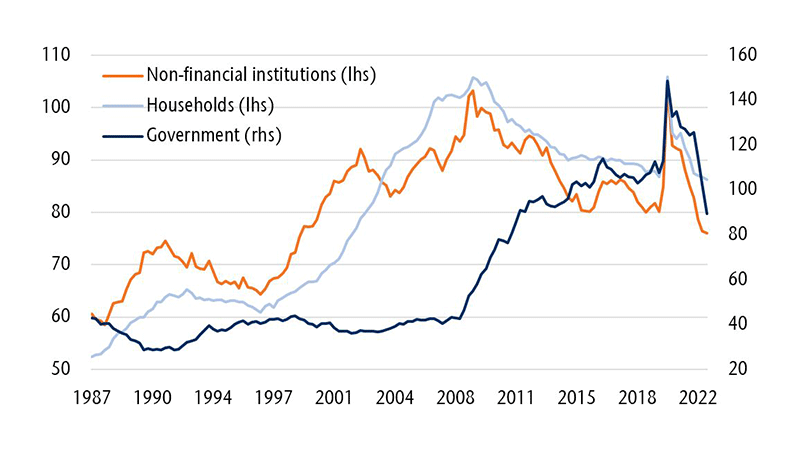

Debt levels

Balance sheets have improved across all segments in both the UK and continental Europe. Thanks to stronger GDP levels driven by inflation, debt levels as a percentage of GDP decreased to levels last seen in 2009. Corporate debt levels even returned to 2007 levels.

Outstanding debt in % of GDP

Source: ONS, Berenberg

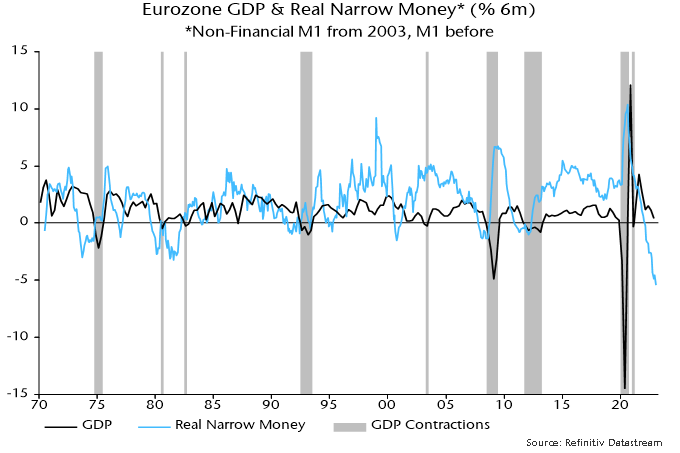

A Eurozone recession can now be ruled out, according to the ECB and a PMI-hugging consensus.

Someone forgot to tell the monetary data.

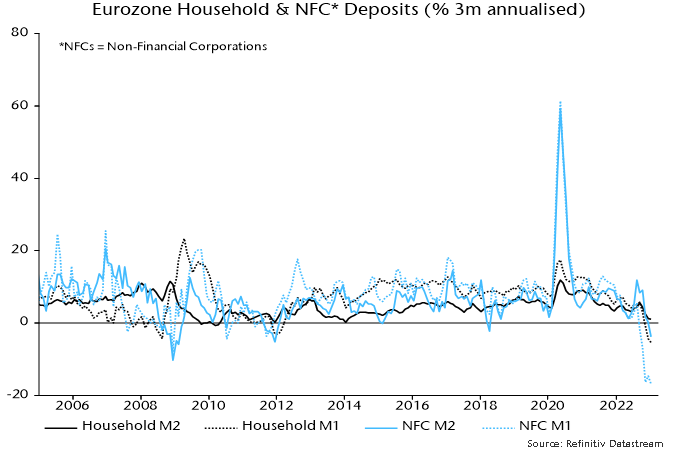

The favoured Eurozone narrow money measure here – non-financial M1 – fell for a fifth consecutive month in January, while broad money – non-financial M3 – was unchanged following marginal gains in November / December.

With inflation data remaining hot, six-month contraction of real narrow money (i.e. deflated by consumer prices) reached a new record, of 5.4% or 10.5% annualised – see chart 1.

Chart 1

A post last month noted that UK sectoral money trends were displaying a recessionary pattern: corporate broad and narrow money holdings were falling in nominal terms, suggesting a cash flow squeeze, while households were moving large sums out of time deposits into sight deposits, consistent with a shift in consumer behaviour from spending to saving.

The same trends are now on show in the Eurozone: corporate M2 and M1 deposits fell in the three months to January, as did household M1 deposits – chart 2.

Chart 2

The no-recession bandwagon gained momentum following Eurostat’s flash estimate that Eurozone GDP grew by 0.1% in Q4. Recently released national details paint an uglier picture.

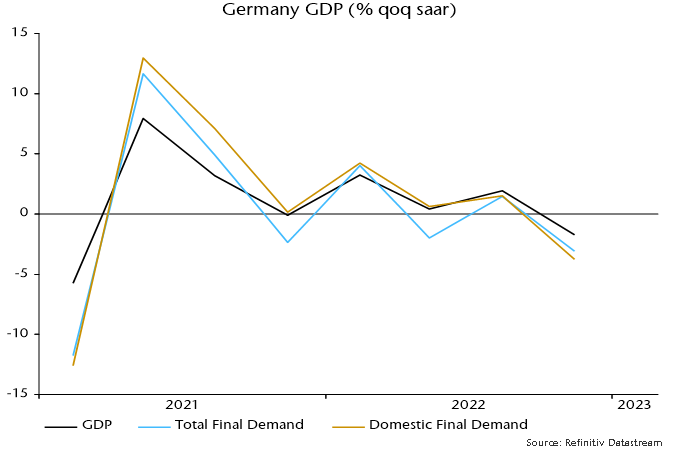

The Q4 fall in German GDP was revised from 0.2% to 0.4%, which will feed into an updated Eurozone number next week.

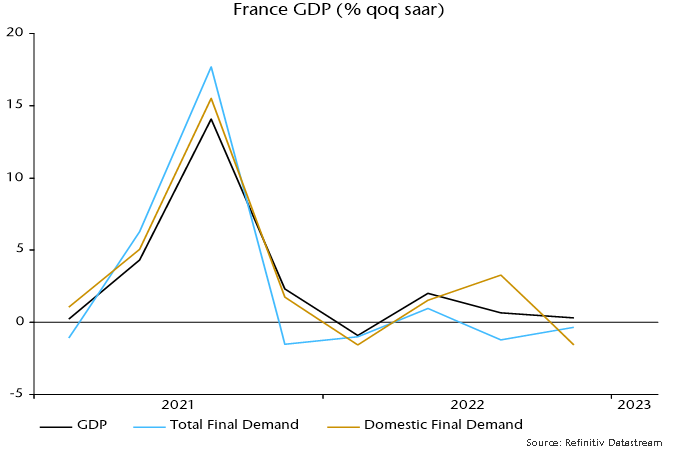

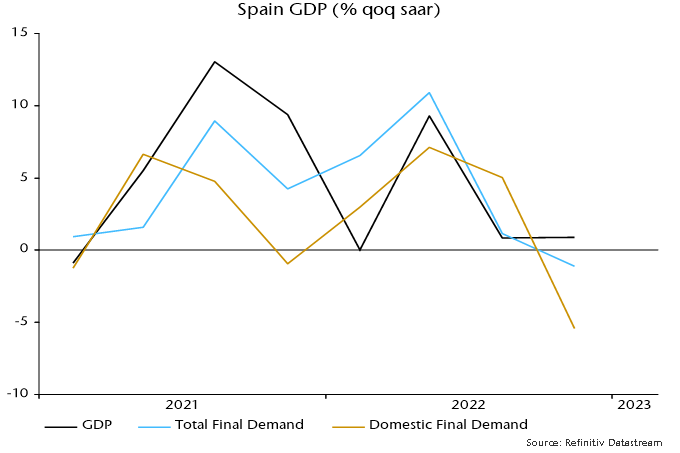

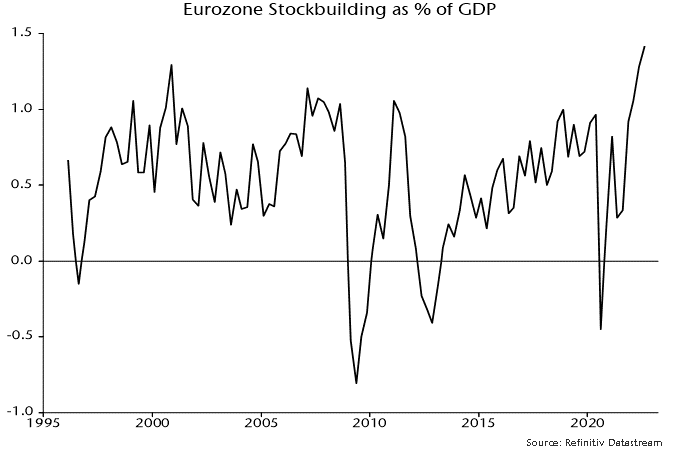

More significantly, expenditure breakdowns show that domestic final demand weakened sharply in Q4 in France, Germany and Spain – at annualised rates of 1.6%, 3.7% and 5.4% respectively. The GDP impact was cushioned by a rise in net exports driven by import weakness and a further increase in stockbuilding – charts 3-5.

Chart 3

Chart 4

Chart 5

Eurozone stockbuilding, therefore, appears to have risen further from its record (in data since the mid 1990s) share of GDP in Q3 – chart 6. A violent reversal from lower peaks in 2007 and 2011 was a key driver of the 2008-09 and 2011-12 recessions.

Chart 6

The no-recession narrative was bolstered by February PMI results showing a pick-up in Eurozone services activity and new business. Manufacturing new orders, however, remained contractionary and are a better guide to the cyclical trend (since the key economic cycles – stockbuilding, business investment and housing – involve goods demand; there is no independent services cycle).

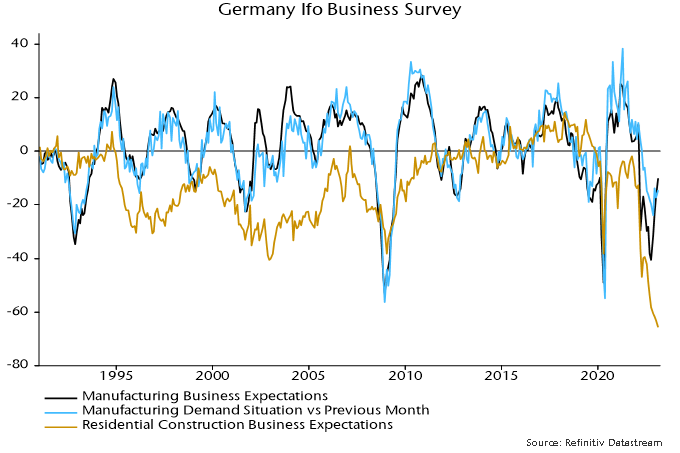

The move off the lows in manufacturing PMI results has been mirrored in the German Ifo manufacturing survey. Business expectations, however, remain weak by historical standards and an indicator of demand inflow has risen by less, stalling between December and February – chart 7.

Chart 7

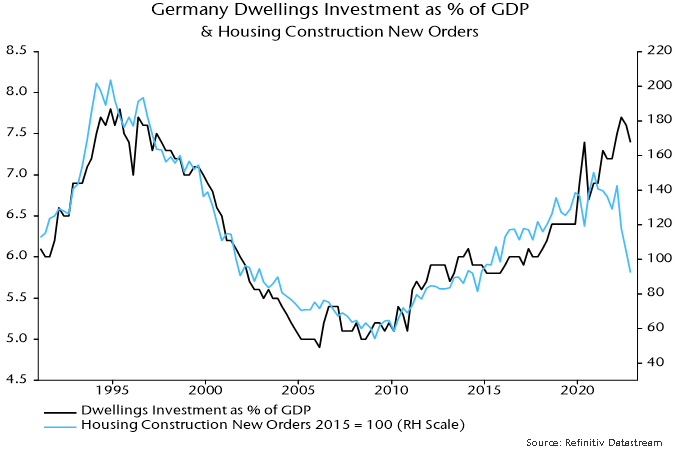

Residential construction expectations, meanwhile, plumbed another record low in February. Survey weakness has been reflected in hard data: housing construction new orders in Q4 were down 35% from Q1 and the lowest since 2014. Dwellings investment was a drag on GDP during H2 2022 but the orders plunge suggests a further big negative impact to come – chart 8.

Chart 8

January was a strong start to the year for equity markets. In fact, the Nasdaq is off to its best start since 1991. Given that lenders (banks) are building reserves to prepare for a recession, and the money printers (central banks) are trying to cool the economy, the strength of equity markets seems to defy logic. It’s as if financial markets are completely ignoring the recession nipping at our heels. What’s driving this?

You guessed it: much of the January returns were powered by a trash rally. We’re talking about low-quality, high volatility stocks driven up by retail investors and internet frenzy.

Source: Sain Godil’s phone

What defines a trash rally?

Remember the GameStop phenomenon of January 2021? This is a textbook example of a trash rally. A near-bankrupt company saw its stock skyrocket thanks to a bizarre retail trading frenzy and a rash of internet jokes and memes. This resulted in a significant and illogical increase in stock price (trash rally) and the origins of the term “meme stock.”

Meme stocks are defined by several key characteristics:

low ROE

negative earnings

high leverage

low market cap

high short interest

weak leadership

The current trash rally is being fueled by a resurgent risk appetite among some investors. We’re seeing explosive growth in a variety of meme stocks this month after a crushing year for equities, although many analysts are skeptical the most recent moves will last.

A closer look at the data

According to JP Morgan, retail market orders reached 23% on Jan 23, 2023. To put things in perspective, when the original GameStop saga began, retail trading peaked at 22%. The result of this euphoria can be seen below with the year-to-date performance of these high beta stocks including some indexes that replicate low-quality stocks.

How has the performance been since January 2022

Source: Global Alpha Capital Management and Bloomberg

How are those meme stocks doing since January 2022?

Two years ago, we were all stuck at home, feeling bored, and getting a false sense of financial security from stimulus checks. With sports events and gambling closed, retail investors made the stock market their casino. While some retail investors made a fortune, unfortunately, many lost a lot. The above charts (blue bars) show how most of the names have been cut in half, if not more.

Management teams of many meme stocks took advantage of the inflated stock prices to issue more equity and improve their finances. According to the Financial Times, meme stocks have raised over $4.7 billion from the hype.

AMC, a poster child for meme stocks, raised $2.8 billion from sales of equity and new debt. Fundamentally their business has not improved with current sales below 2018 revenue, and EBITDA is expected to be half of what they did in 2018. This is despite the fact that Avatar: The Way of Water is close to collecting $2 billion in global box office ($623.5 million in the U.S.).

Here we go again

All signs point to another meme stock rally. Take troubled retailer Bed Bath & Beyond, for example. They missed interest payments on bonds on Jan 29, which may lead to bankruptcy, and yet the stock price appreciated by 129% in just over a week. Carvana, the debt-strapped online used-car retailer is up 143% year-to-date. A meme stock favourite, Carvana was trading at $11.55 at the point of writing, way below its peak of $370 set in August 2021. Despite being down almost 98% from its peak, more than 266,000 call contracts changed hands on January 30, 2023 according to Bloomberg.

Is this just a U.S. Phenomenon?

The Bonusetu (a Finnish Casino) research team combed through Google trends for each European country to find the most Googled stock for each country. Tesla took the top spot in a whopping 28 countries and AMC is most popular in five countries. Below is a screenshot or performance of some other names in the group.

While we understand Google trend data does not necessarily mean Europeans participated in the trades, it’s difficult to imagine an alternative explanation. Was everybody in the UK, Germany, Ireland, and Croatia just purchasing tickets to watch Avatar at an AMC theatre? Or booking their next vacation on Icelandic Air or Virgin Galactic? It seems far more likely they were getting seduced by meme stocks.

Will history repeat itself?

Once again euphoria has set in and everyone is having a good time, gleefully ignoring the well-documented consequences of excessive indulgence. We’ve seen this story play out several times over the last few decades. Think back to 2001. That year, Nasdaq was up 12% in January but fell over 30% in the following 11 months when the dot-com bubble burst. In our February 11, 2021, weekly called The Canary in the Coal Mine we compared the meme stock situation to the tech bubble as well as the 2008 financial crisis.

Portfolio Impact

Popular media is once again helping stir up the meme stock frenzy. As we see a repeat of the same movie (no pun intended, AMC) this may have an unfortunate impact on higher-quality names that could get mispriced lower. The good news? For long-term investors in quality companies, this provides an amazing opportunity to buy quality companies at attractive valuations.

Our ability to be highly selective and nimble in our portfolio holdings leaves us well-positioned to enter a period of great opportunity for fundamental stock pickers. Our focus on high-quality companies with defensible business models and strong balance sheets should help outperform our small-cap benchmark. As we reflect on the state of markets and the fundamentals of our target companies, we are excited about the current environment and future growth opportunities.

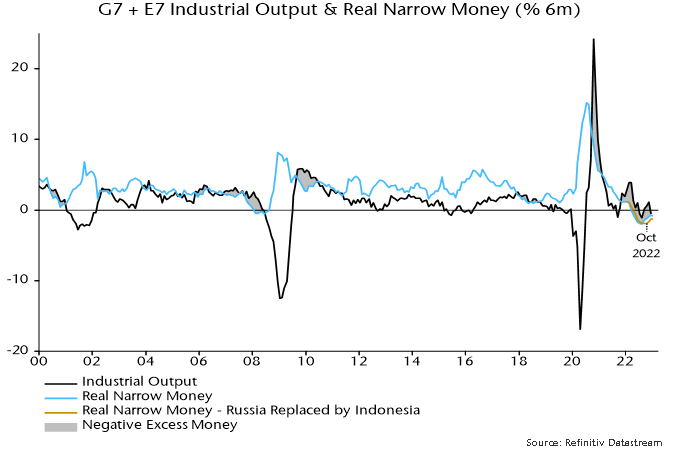

The two measures of global “excess” money tracked here remain negative, arguing for a cautious view of equity market prospects.

Excess (or deficient) money refers to the difference between the actual money stock and the demand for money to support economic transactions. According to “monetarist” theory, a surplus is associated with increased demand for financial / real assets and upward pressure on their prices, assuming no change in supply.

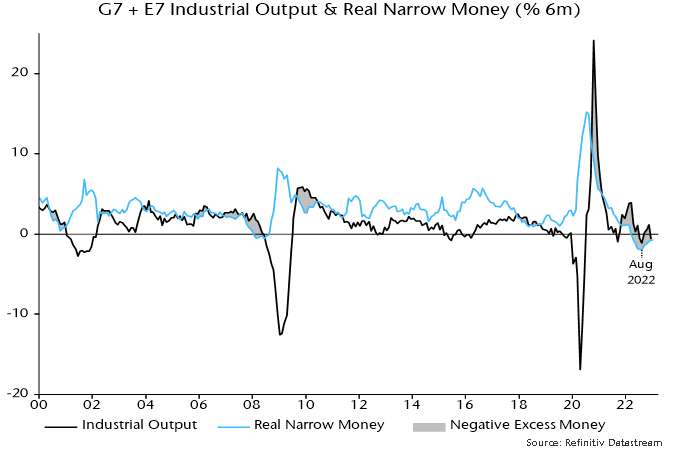

Excess money is unobservable so two proxies are followed here: the difference between six-month rates of change of global (i.e. G7 plus E7) real narrow money and industrial output; and the deviation of 12-month real narrow money growth from a slow moving average.

Historically (i.e. over 1970-2021), global equities outperformed US dollar cash on average only when both measures were positive. Unsurprisingly, average performance was worst when both were negative (underperformance of 8.9% pa). These results allow for reporting lags in monetary / economic data.

The second measure turned negative in October 2021, which was known by end-November. The first measure followed in November, which was known by end-January 2022 (a longer lag because industrial output numbers are released after monetary / CPI data).

Previous posts noted a recovery in global six-month real narrow money momentum during H2 2022*. With industrial output expected to weaken, it was suggested that the first measure would turn positive, possibly by December.

The second measure – based on 12- rather than six-month real money momentum – was deeply negative in late 2022, with a switch to positive deemed unlikely before mid-2023.

The suggested switch positive in the first measure has yet to occur. The six-month rate of change of industrial output crossed below zero in December but remained just above real narrow money momentum – see chart 1.

Chart 1

Will a cross-over have occurred in January? Partial data suggest that the recovery in real money momentum stalled last month. A reliable January estimate of industrial output won’t be available until mid-March. A reopening bounce in China could offset weakness elsewhere.

A further point is that the recovery in global real narrow money momentum since mid-2022 partly reflected a strong pick-up in Russia, which may be of limited global relevance given the country’s enforced economic and financial isolation.

Chart 2 shows the result of replacing Russia with Indonesia in the G7 plus E7 real money calculation from January 2022, before the February invasion of Ukraine**. The trough in real money momentum is placed in October rather than August, with the subsequent recovery even more anaemic.

Chart 2

*The trough in real money momentum originally occurred in June but is now placed in August, partly reflecting revisions to US CPI seasonal adjustments.

**The other E7 countries (as defined here) are Brazil, China, India, Korea, Mexico and Taiwan.

Since the World Bank’s International Finance Corporation first coined the term emerging markets in 1981, the characteristics and composition of the markets have evolved significantly. Past concerns regarding the resilience of emerging markets during a crisis led some investors to struggle with the merits of including a direct allocation. However, with the rise of China and its leadership of global economic growth, investors are increasingly considering a dedicated allocation to emerging markets. This article reviews the evolution and the general case for investing in emerging markets.

The key attributes supporting the case for global emerging markets have been evident for some time and include:

Greater growth

In the latest Global Economic Prospects report by The World Bank Group, emerging and developing economies are forecast to grow more than double that of advanced economies in 2023 and 2024.

Drivers of Innovation

Many emerging markets companies have become leaders of innovation in important sectors such as internet-related technologies, electric vehicle battery manufacturing, and computer chip manufacturing.

Household names

Many emerging market companies are household names such as Samsung and Hyundai, while other less recognized companies have acquired well-known global brands.

Rising returns

As emerging markets shift from manufacturing to more value-added industries, there is an expectation for the ability to generate superior returns to rise.

Alpha opportunities

Emerging markets are less researched by the analyst community compared with large cap developed equity markets, which creates opportunities for excess returns from independent research by active managers.

Background

Emerging markets are characterized as countries with growing economies and a growing middle-class population. Many of these markets continue to have high rates of poverty, and often they are still experiencing significant social and political change. But despite such headwinds, the growth prospects of emerging markets can provide a strong base for investors to be rewarded.

The market capitalization of emerging markets was US$ 90,456 billion as of December 31, 2022, representing a little over 11% of the world equity capitalization. Yet many institutional investors have no direct exposure to emerging markets. Instead, investors often rely on their international and global equity managers to selectively invest in emerging markets, which can result in the allocation falling well short of its representation of the world equity market capitalization. With emerging markets representing the highest growth area of global stock markets, there is a case for investors to benefit from at least a market representation.

The MSCI Emerging Markets Index is comprised of over 1,300 stocks in 24 countries. Countries are normally grouped into three regions, Emerging Markets Asia, Emerging Markets Latin America and Emerging Markets Europe, Middle East and Africa, with the Asian region representing almost 80% of the market index.

Evolution

For the longest time emerging markets were considered similar to the Canadian equity market, with a heavy bias to commodities. Today, the combined weighting in energy and materials for emerging markets is less than 13% of the index market capitalization, compared to 30% of the Canadian equity market. Instead, emerging markets have evolved to offer opportunities different to the Canadian equity market. For example, emerging markets have experienced a steady rise in the information technology and health care sector allocations, which together represent over 20% of the market index (Figure 1). Not only that, but within the information technology sector there has also been a radical change in its composition with large and successful companies, such as Alibaba and Tencent making up an important component of the sector.

Figure 1: Index Sector Allocations

Global Industry Classification (GIC) Sector

MSCI Emerging Markets (%)

S&P/TSX Composite (%)

Energy

5.0

18.1

Materials

7.6

12.0

Industrials

19.4

13.3

Consumer Discretionary

12.5

3.7

Consumer Staples

4.7

4.2

Health Care

10.7

0.4

Financials

14.3

30.8

Information Technology

10.8

5.7

Communication Services

2.8

4.9

Utilities

3.2

4.4

Real Estate

8.9

2.6

Source: Thomson Reuters Datastream. Data as of December 31, 2022. Due to rounding, column percentages may not total 100%.

The financial sector represents around 14% of the index and offers a further differentiation versus developed markets, where the loan-to-deposit ratios in emerging market companies are generally lower.

However, the biggest change to the emerging market index has been with respect to country allocation, and the growing dominance of China in the index. It was not long ago that large cap China A shares represented less than 1% of the MSCI Emerging Markets Index. At the end of 2022, China accounted for over 32% of the index (Figure 2).

Figure 2: Region and Larger Country Allocations

Region and Country

MSCI Emerging Markets Index (%)

Emerging Markets Asia

78.3

China

32.3

India

14.4

Taiwan

13.8

Republic of Korea

11.3

Emerging Markets Europe, Middle East & Africa

13.2

Saudi Arabia

4.1

United Arab Emirates

1.4

Qatar

1.0

Kuwait

0.9

South Africa

3.7

Emerging Markets Latin America

8.5

Brazil

5.3

Mexico

2.3

Understanding the Risks

It is important to appreciate risks associated with investing in emerging markets. While active managers can mitigate some of these risks through research and careful selection of individual stocks, investors should recognize the following.

Political and social risk: Political and social changes taking place in emerging market countries can lead to uncertainty due to corruption, regulations not always being rigorously enforced, or governments exhibiting an unwanted influence. The uncertainty contributes to market volatility. For example, Beijing’s actions to limit the influence of Hong Kong-listed technology companies, combined with a real estate sector crisis and the zero-COVID policies that witnessed longer strict pandemic controls relative to most other governments, contributed to a tough and volatile 2021-2022 for emerging market equities.

Information and liquidity risk: Although the quality of data has vastly improved, obtaining good, complete and timely information can still be challenging in emerging markets. Currency controls remaining in a small number of markets also may create liquidity concerns.

Recognizing the potential benefits

While the countries are classified as emerging, nearly all the companies in the MSCI Emerging Markets Index have a market capitalization greater than US$ 1 billion, which compares to 209 Canadian companies with a market value above US$ 1 billion. Increasingly, emerging market companies are becoming household names, whether on their own merits, or through acquisition of global branded companies, such as Samsung, Hyundai Motor and the Indian conglomerate, Tata, which is the owner of brands such as Jaguar, Land Rover and Tetley Tea.

The key benefits offered by emerging markets include:

Growth opportunity: The drivers of growth are wide ranging and include demographics, economic development, technology, innovation, infrastructure development, and capital market developments. While global growth is expected to moderate from 2021 levels, emerging and developing countries are expected to account for a significant component of world gross domestic product (GDP). The World Bank forecasts emerging and developing markets to grow at an average annual rate of 3.4% in 2023 and 4.1% in 2024, compared to expansion of only 0.5% and 1.6%, respectively for advanced (developed) economies.1 A significant proportion of developed market company earnings are also linked to emerging market growth, further underlining its importance.

Drivers of innovation: Innovation in emerging markets has contributed to its evolution, as well as China becoming an important component of the market. Innovation has allowed several emerging market countries to leapfrog the developed world in terms of business models. For example, while many farmers in India have no access to computers and landlines, smart phones have created an information and business environment that allows buyers and sellers to interact, as well as enabling e-payments.

Rerating opportunity: Ordinarily, high-growth assets are priced at a premium. Emerging market stocks have traditionally traded at a discount to developed world valuations, but the economic fundamentals for emerging markets as a whole have improved.

Improving returns: Many emerging market companies are shifting away from manufacturing for Western companies and looking to develop their own identity and growth success. To achieve this they are tapping into higher value-added areas using brands and technology, recognizing that branded firms with loyal followers can achieve more than double the margins of non-brand firms. Return on invested capital (ROIC) should rise for emerging market companies as they develop world-class brands.

Growing universe of opportunities: The growth of China in the emerging market index has also witnessed a growth in the universe of investment opportunities. Today, there are as many China A shares that meet the typical liquidity and market capitalization criteria as there are in the United States (US) equity market. Similarly, the number of opportunities for emerging markets excluding China is not too different from the number of opportunities for the global developed market, excluding the US.

Style offset opportunity: The growing opportunity set has witnessed a growth in systematic (quantitative) fund offerings, where the managers use technology to gain a breadth of understanding on a large universe of companies, compared to the depth of understanding associated with fundamental managers focused on selecting a smaller portfolio of companies. As for other equity markets, investors who can accommodate multiple managers in an asset class can benefit from the complementary approaches of systematic and fundamental styles.

Alpha opportunity: The external analyst community generally undertakes less research of emerging market companies compared to global developed companies. Active managers have been able to benefit from independent research with over 86% of managers in the emerging market equity universe outperforming the MSCI Emerging Market Index over the 10 years ended December 31, 2021 (based on the eVestment database).

Environmental, Social and Governance Considerations (ESG)

Despite the political and social challenges associated with emerging market countries, companies are increasingly recognizing the importance of ESG considerations. Helping this cause has been the expansion of ESG coverage of emerging markets companies by third-party providers. The importance of each ESG component varies from one country, industry or company to another. However, like the developed world, corporate governance tends to be the most material issue, followed by the steps being taken to manage the environmental impact of companies in the emerging markets.

The Case for Emerging Markets

Many investors are underweight emerging markets relative to its representation in world equity markets, yet global growth is expected to be led by emerging and other developing markets.

Canadian investors have historically shied away from emerging markets, partly due to the historical commodity bias. Today, emerging markets offer a very different opportunity set due to innovation that has seen a transformation in the type of companies and opportunities, including a significant growth in the information technology sector.

As emerging market companies shift from manufacturing to higher value-added interests using brands and technology, the number of emerging market household names will increase, and help to grow margins and ultimately the return potential from emerging markets.

1 Source: World Bank Global Economic Prospects, January 2023

This week we will be discussing a new addition to the portfolio, SalMar (Ticker: SALM NO), and the latest developments in the salmon farming industry.

The global salmon market was estimated to be a US $50 billion industry in 2020 and expected to grow at 3.7% a year to reach $76 billion by 2028. The growing disposable income in emerging countries and subsequent changes in dietary habits are some of the main drivers behind this growth. Consumers of salmon are more often from the middle- and upper middle-classes who are generally less sensitive to economic slowdowns and less likely to dramatically change their spending patterns, particularly in food purchases. In addition, the health benefits of eating salmon rich in Omega-3 over red meat are well-documented. As a protein, its feed conversion ratio (i.e., the kilograms of feed needed to increase the animal’s body weight by one kilogram) is one of the best among the protein sectors.

Global Alpha received the SalMar shares as part of the cash and share deal that SalMar made to acquire our previous holding in the portfolio, Norway Royal Salmon. The combined entity creates the second-largest salmon farmer in the world.

Both parties have operations in Northern and Central Norway. With this new acquisition, synergies will come from improved utilization of available biomass i.e. the total weight of the fish. SalMar will implement their best-in-class practices at the existing Norway Royal Salmon operations in Norway to improve biological challenges. Gaining increased access to smolt (juvenile salmon) will give SalMar additional benefits stemming from vertical integration such as increasing the quantity of harvested fish, which will optimize the utilization of the processing facility.

However, before the deal closed, the industry received some unexpected news. On September 28, 2022, the Norwegian government announced the most significant change to date to the salmon industry’s regulatory framework by imposing a 40% resource tax on salmon and trout farming in Norway. This would take the marginal tax rate of producers from 22% to 62% if implemented in the initially proposed form. A resource tax is already levied on oil and gas, hydropower operations, and profits generated using Norway’s natural resources.

The major salmon producers were quick to respond to the government’s proposal:

SalMar: “Earlier this year, SalMar bought its relative share available for a fixed price for the capacity adjustment in the traffic light system. 1,223 MAB tonnes for a total consideration of NOK244.6 million. SalMar has chosen to use the opportunity to terminate the purchase. This is due to the resource rent tax the Government has now announced.”

Leroy Seafood (LSG NO): “In 2022 Leroy purchased 614 tonnes maximum allowable biomass under the so-called traffic light system at a total value of NOK123m. Leroy has decided to cancel this purchase. Increasing the tax rate from 22% to 62% creates unreasonable framework conditions for the industry in Norway, changing the scope and incentives for investments in areas other than maintenance capex. All major new investments in the Group’s value chain in Norway must regrettably be put on hold pending the decision of the Storting, the Norwegian parliament.”

Mowi (MOWI NO): “In light of the Norwegian government’s proposal for a 40% resource tax on Norwegian aquaculture, and a resulting total tax of 62%, Mowi is cancelling its acquisition of 914 tonnes MAB for a total value of NOK183m. The government’s tax proposal means that Mowi can no longer justify the purchase price. Mowi respectfully advises the government to reconsider its resource tax proposal.”

In addition to suspending purchases, the biggest salmon producers were notably absent from the first auction of biomass capacity since the government proposed the resource tax, even though these same producers bought capacity at the previous auction in 2020.

More recently, shares of the Norwegian salmon producers have been reacting to headlines from politicians. They first rose after Geir Pollestad, deputy leader of the Norwegian Center Party, told a local newspaper that the party was open to modifying the tax. However, finance minister Trygve Vedum said shortly afterward that the original proposal of a 40% tax should remain. With the governing parties losing popularity, and amid growing concerns about the over-reliance of regions on the salmon industry for employment, we foresee a compromise will be reached and a modified version of the original proposal will be implemented.

Supply growth should remain muted given increased biological challenges and stricter regulations. We see support for salmon prices and demand for salmon is likely to remain strong despite the challenges. These social and environmental aspects are further reasons why exposure to the salmon industry is attractive and we will continue to follow as developments unfold.

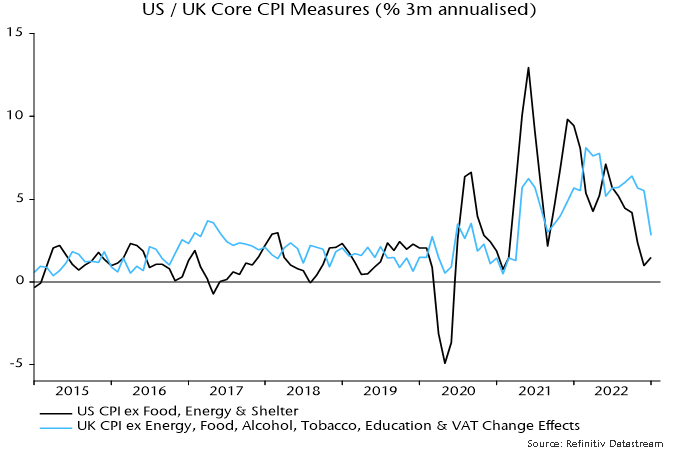

US and UK CPI data this week elicited opposite market reactions but core momentum has recently slowed notably in both cases, consistent with a moderation in money growth rates two years earlier.

Chart 1 shows three-month annualised rates of change of preferred core measures – CPI ex. food, energy and shelter for the US and CPI ex. energy, food, alcohol, tobacco, education and VAT change effects for the UK. US three-month momentum was just 1.5% in January, while UK momentum fell sharply to 2.8%.

Chart 1

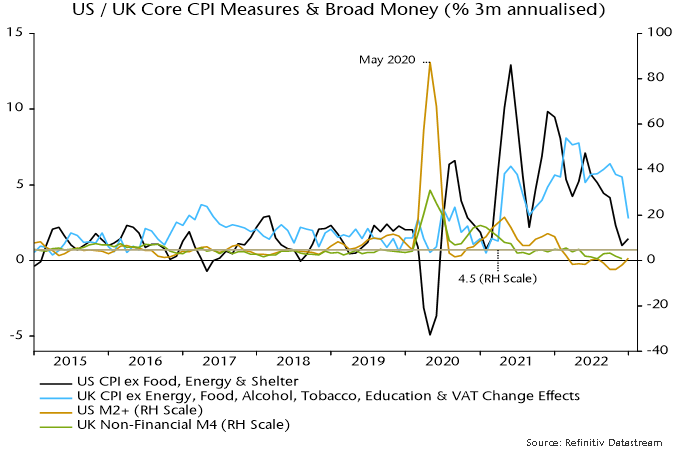

The ”monetarist” rule of thumb is that money leads prices by about two years. Chart 2 superimposes three-month rates of change of broad money. Growth peaked in May 2020. The recent significant declines in core CPI momentum began in June 2022 in the UK and July in the US.

Chart 2

Average broad money growth of 4.5% pa in both the US and UK over 2010-19 was associated with sub-2% average core CPI inflation. Three-month rates of change of broad money moved below 4.5% annualised on a sustained basis in March 2022 in the US and June in the UK. A reasonable expectation, therefore, is that core CPIs will be rising at a sub-2% by mid-2024 in both cases.

The path lower in money growth from the May 2020 peak was bumpy and core CPI momentum is likely to display similar volatility around a declining trend.