Eurozone February monetary data were extraordinarily negative, suggesting that interest rates were already at a restrictive level before the 50 bp rate hikes in February / March.

Economic sentiment has lifted in early 2023 in response to a collapsing gas price and China’s reopening but the impact of monetary restriction has yet to kick in.

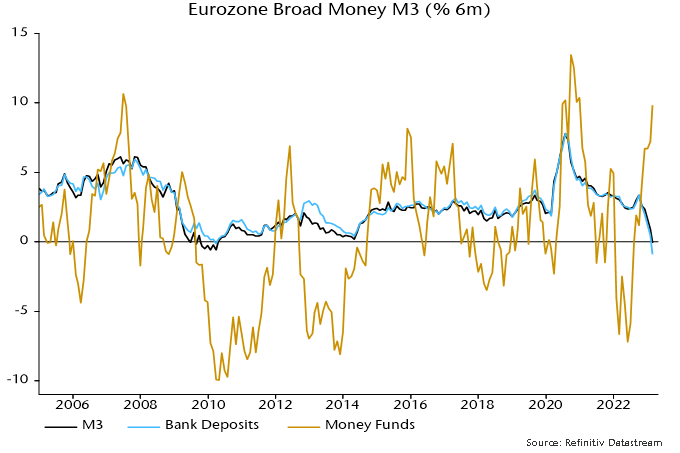

The headline M3 broad money measure was down again in February and has fallen in four of the last five months. The six-month rate of change turned negative and is the weakest since 2010 in the aftermath of the GFC – see chart 1.

Chart 1

Bank deposits are contracting at a faster pace than then because of a portfolio switch into money market funds and short-term bank bonds. This switch has been motivated by relative yields but the banking crisis could give a further boost to money fund inflows.

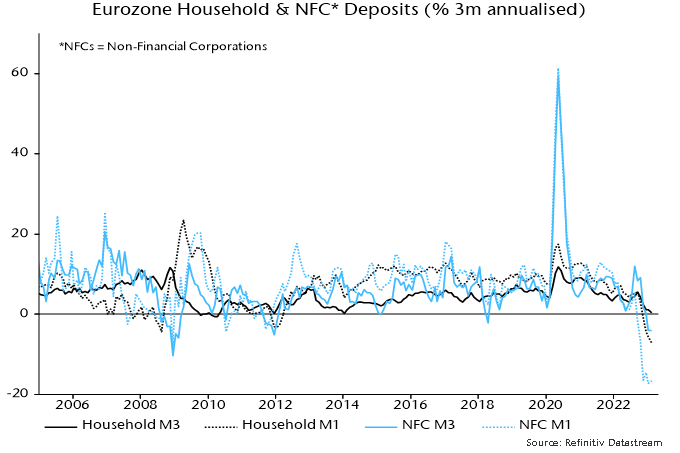

Corporate money trends are particularly alarming. Bank deposits of non-financial corporations contracted at a 4.0% annualised pace in the latest three months, with the overnight (M1) component down by 16.6% – chart 2. Household deposits fell in February and are barely up over three months, with a shift out of overnight accounts suggesting weak spending intentions.

Chart 2

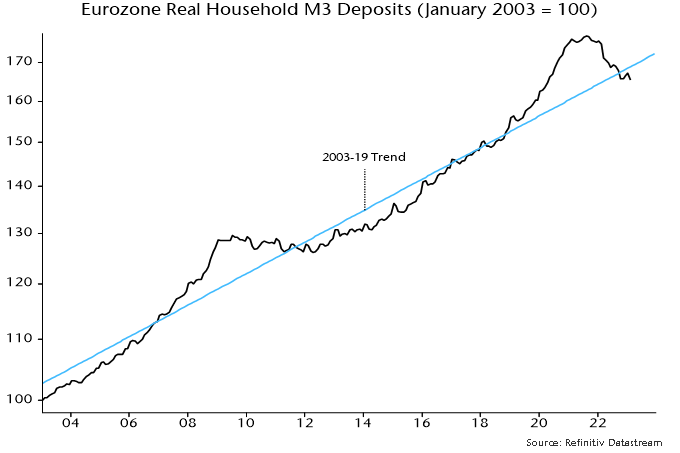

Talk of households still sitting on substantial spendable “excess” savings is suspect. Allowing for inflation erosion, household M3 deposits are below their pre-pandemic trend – chart 3.

Chart 3

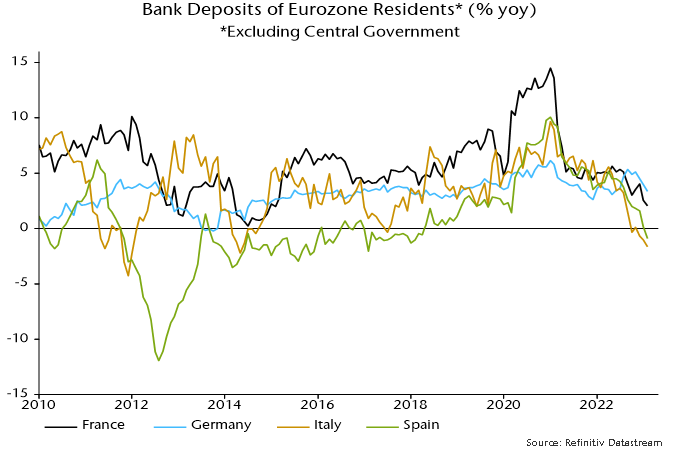

Country deposit data suggest that a core / periphery divergence is opening up, with Spain following Italy into year-on-year contraction – chart 4.

Chart 4

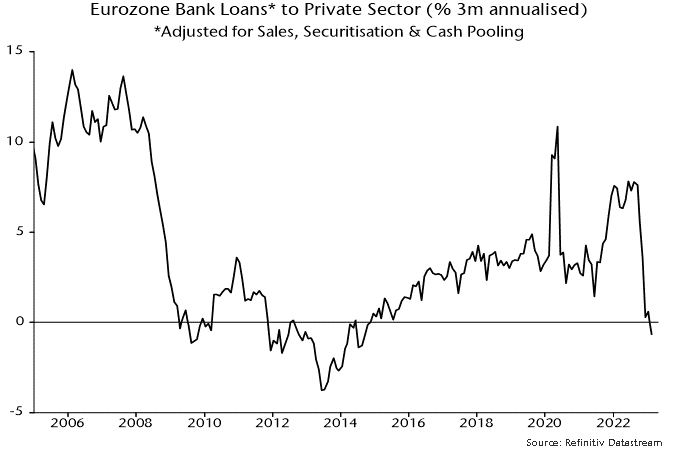

Monetary weakness partly reflects a collapse in credit growth: three-month loan momentum was running at an annualised 7.6% as recently as September but turned negative in February – chart 5.

Chart 5

Corporations have been repaying short-term loans in size since November, consistent with a downswing in stockbuilding, which reached a record share of GDP in Q4. Numbers could bounce near term as firms draw down credit lines while they still can.