Eurozone monetary trends have been suggesting an economic slowdown through end-2021. A recent moderation of consumer price momentum, however, has stabilised six-month real narrow money growth, hinting at a bottoming out of business surveys and other coincident indicators in early 2022.

The Ifo manufacturing survey is a timely indicator of German / Eurozone industrial momentum, displaying a strong contemporaneous correlation with German / Eurozone manufacturing PMIs (but with a longer history). The business expectations component peaked in March, falling for a fifth month in August – see chart 1.

Chart 1

The March peak is consistent with an August 2020 peak in Eurozone six-month real narrow money growth. The implied seven-month lead is slightly shorter than the historical average – the correlation between Ifo business expectations and Eurozone real money growth is maximised by applying a nine month lag to the latter.

Real narrow money growth, however, has moved sideways since May (July money numbers were released yesterday). The suggestion is that the Ifo indicator – along with PMIs and other business surveys – will weaken further during H2 but bottom out in early 2022.

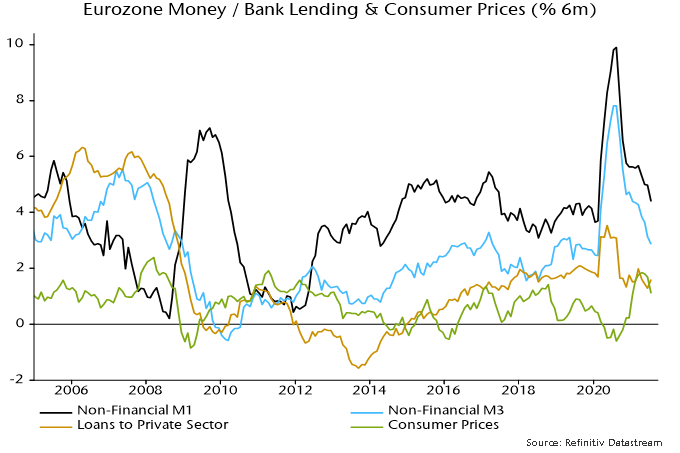

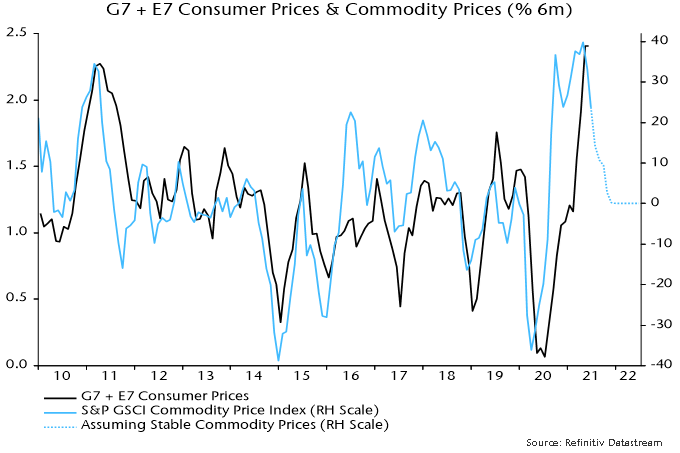

The recent stabilisation of real money growth is not entirely convincing: nominal money trends continued to weaken in June / July but this was offset by a slowdown in six-month consumer price momentum – chart 2.

Chart 2

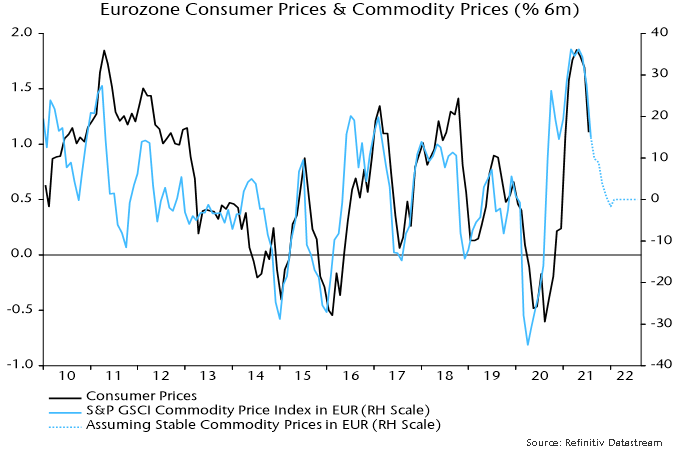

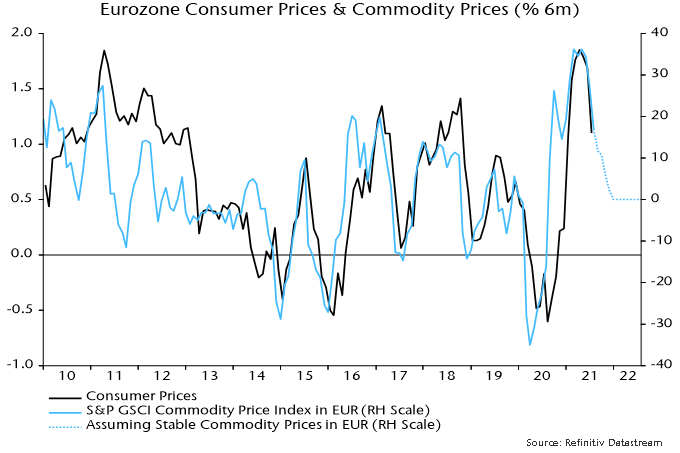

The inflation slowdown, however, could extend, assuming that commodity prices (in euro terms) stabilise at their current level – chart 3.

Chart 3

A recovery in nominal money growth is required to warrant shifting to a positive view of economic prospects. Such a signal would relate to H1 2022 – earlier real money weakness has “baked in” likely economic disappointment over the remainder of 2021.

What could lift money growth? The most likely candidate is a pick-up in bank lending. Six-month growth of loans to the private sector recovered in July – chart 2 – while the most recent ECB bank lending survey reported the strongest expectations for credit demand since 2016.

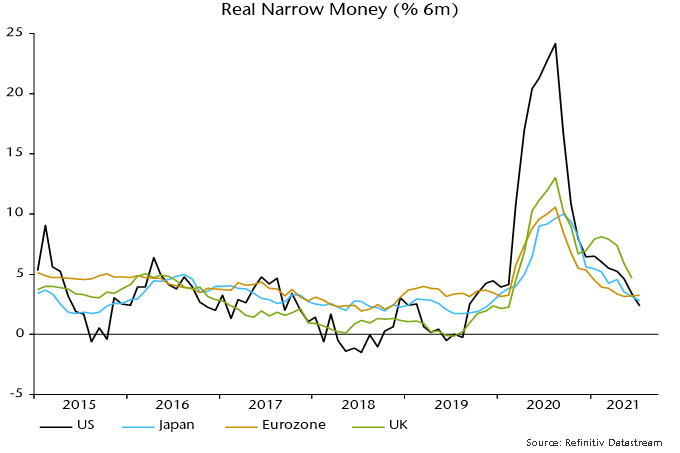

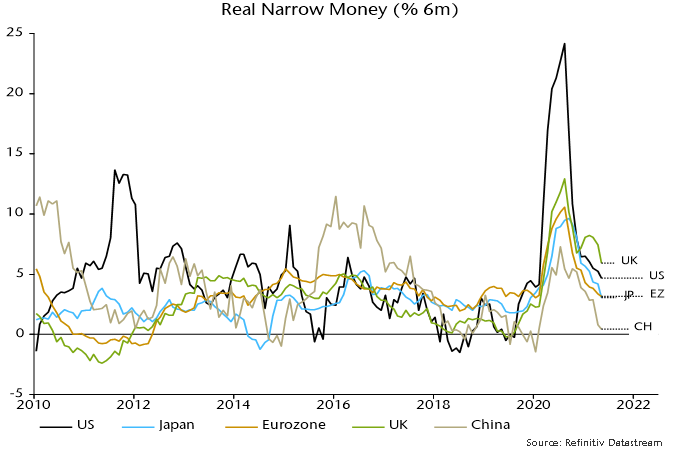

The recent stabilisation of Eurozone six-month real narrow money growth contrasts with a further slowdown in the US – chart 4. The divergence / cross-over suggests improving Eurozone relative economic and equity market prospects, although US real growth could benefit from a faster inflation slowdown over coming months.

Chart 4

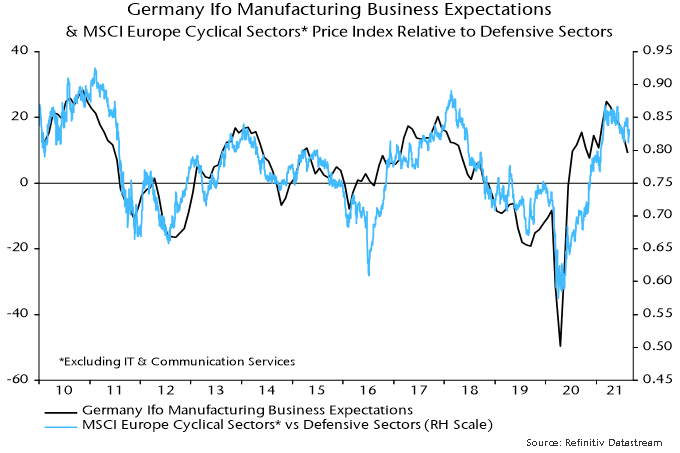

A further fall in Ifo manufacturing business expectations and other survey indicators during H2 would probably be associated with underperformance of European non-tech cyclical sectors relative to defensive sectors – chart 5.

Chart 5

Detailed monetary data for July released yesterday suggest that recent policy easing is beginning to support money growth, in turn hinting at a recovery in economic momentum from end-2021.

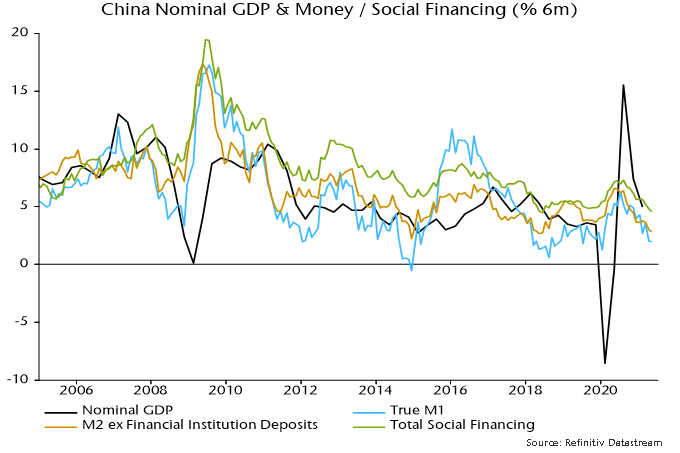

A sustained slowdown in six-month narrow money growth from July 2020 correctly signalled “surprise” Chinese economic weakness so far in 2021. The expectation here was that the PBoC would ease policy in Q2, supporting economic prospects for later in 2021. Adjustment was delayed but the reserve requirement ratio cut on 9 July appeared to mark a significant shift. The hope was that July monetary data would confirm a bottom in money growth.

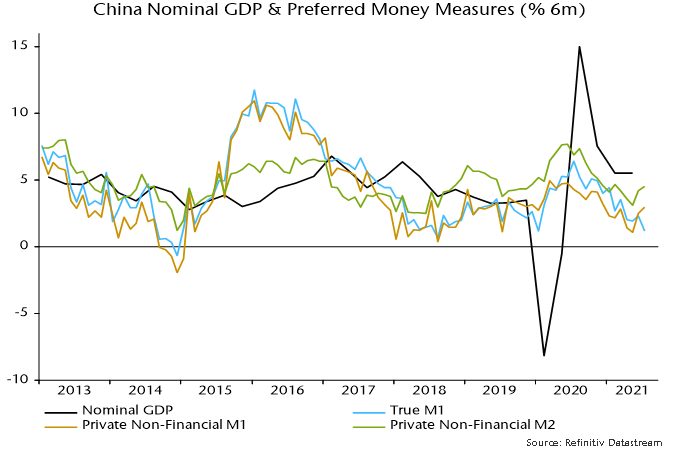

The headline July numbers released on 11 August seemed to dash this hope, with six-month of “true M1” falling to a new low – see chart 1*.

Chart 1

The additional data released yesterday allow a breakdown of the deposit component of this measure between households, non-financial enterprises and government departments / organisations. It turns out that the further fall in growth in July was due to the latter public sector element, which is volatile and arguably less important for assessing prospects for demand and output.

Six-month growth of “private non-financial M1”, i.e. currency in circulation plus demand deposits of households and non-financial enterprises, rose for a second month in July. So did the corresponding broader M2 measure – chart 1.

This improvement needs to be confirmed by a recovery in overall narrow money growth in August, ideally accompanied by a further increase in the private sector measure. One concern is that the rebound in the latter has so far been driven by the household component – enterprise money growth remains weak.

Increased bond issuance and fiscal easing could lift public sector money growth during H2.

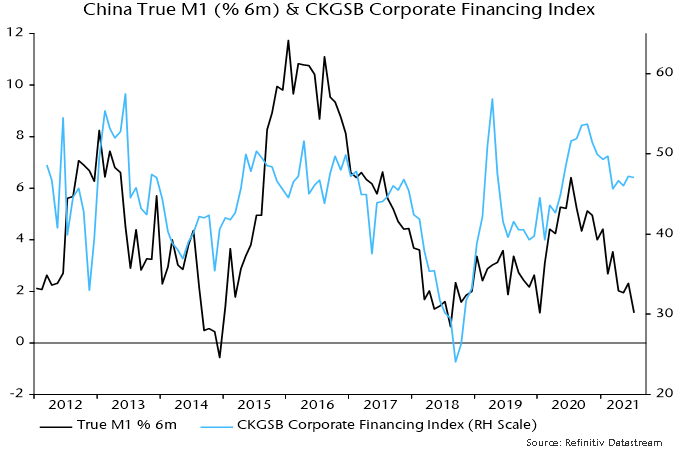

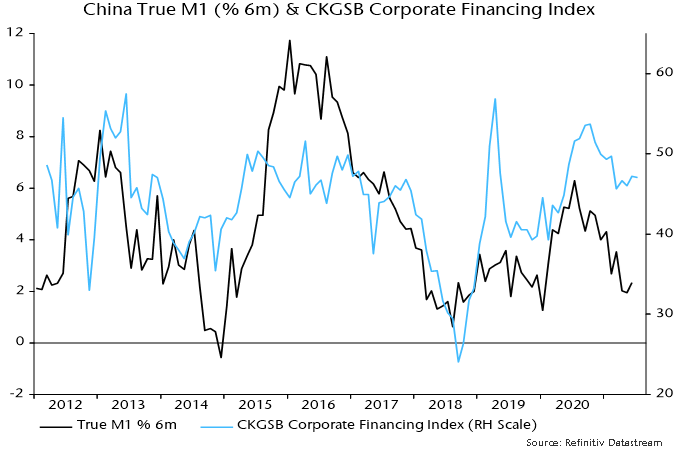

The corporate financing index in the Cheung Kong Graduate School of Business monthly survey is a useful corroborating indicator of money / credit trends – a rise signals easier conditions. The index bottomed in March but has yet to improve much – chart 2. August survey results will be released shortly.

Chart 2

*True M1 includes household demand deposits, which are omitted from the official M1 measure.

The assessment here remains that the global manufacturing PMI new orders index peaked in May and will fall through H2 2021, reflecting a decline in global six-month real narrow money growth from July 2020 through May. Real money growth, however, stabilised between May and June, raising the possibility that a turning point was at hand. A recovery in real money trends during Q3 would be a positive signal for economic prospects for H1 2022 and could support a second leg of the reflation trade.

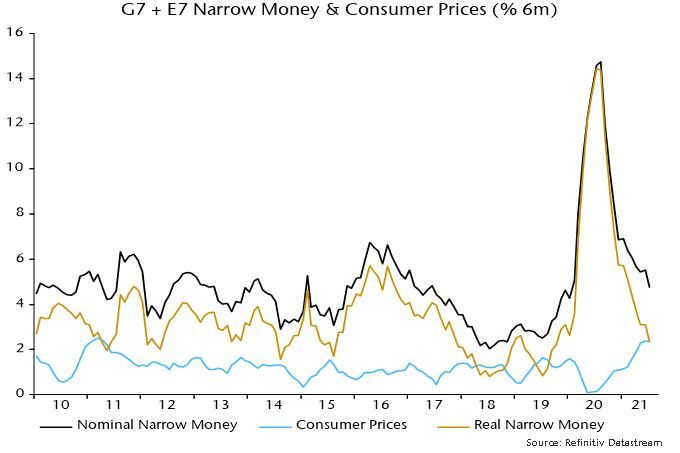

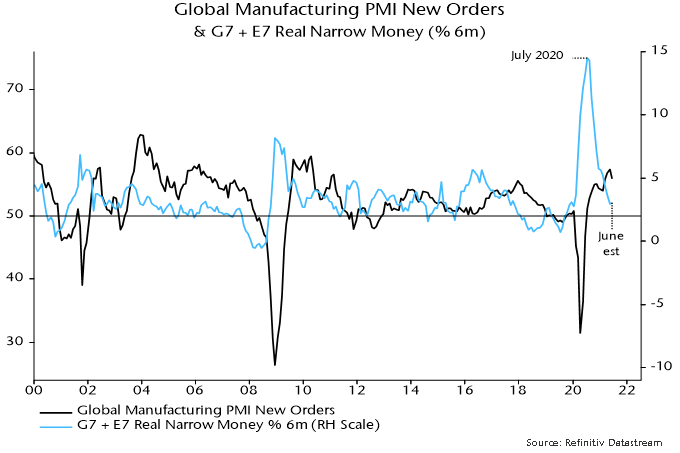

Incoming monetary news for July is unfavourable for this scenario. Global six-month real narrow money growth is estimated to have fallen further last month to its lowest since October 2019, based on monetary data covering 70% of the G7 plus E7 aggregate monitored here – see chart 1.

Chart 1

A pick-up in six-month consumer price inflation contributed to the fall in real narrow money growth into May / June. Price momentum stabilised in July but there was a further decline in nominal money expansion – chart 2.

Chart 2

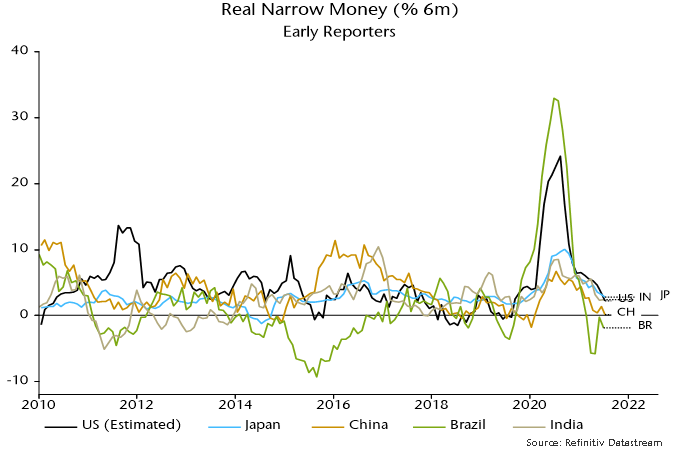

Six-month real narrow money growth is estimated to have fallen in the US, China, Japan and Brazil, with India stable – chart 3. (The US July money number is estimated from weekly data on currency in circulation and commercial bank deposits.)

Chart 3

A recovery in the global measure remains plausible in August / September. Recent commodity price stabilisation suggests a decline in six-month inflation, while Chinese money growth may pick up in lagged response to policy easing.

Global six-month real narrow money growth has led turning points in manufacturing PMI new orders by 6-7 months on average historically. The further fall in real money growth in July, therefore, suggests that PMI weakness will extend into early 2022.

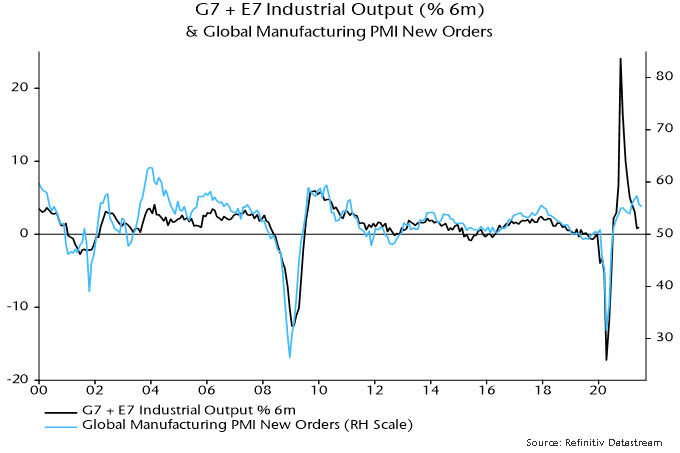

The PMI new orders index is a good indicator of underlying industrial momentum but output was held back by supply issues during H1, disrupting the normal relationship – chart 4. Output momentum could rebound temporarily in Q3 as supply constraints ease even as the PMI moderates.

Chart 4

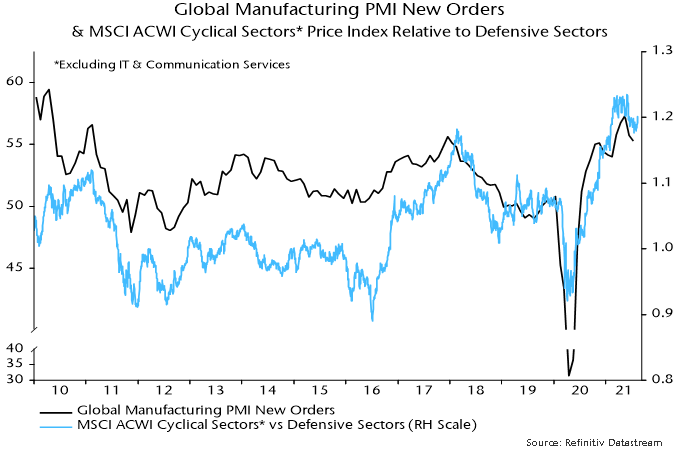

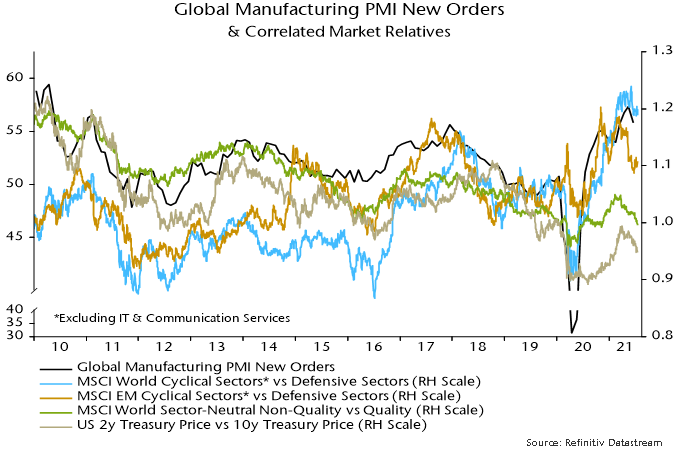

This possibility complicates market analysis. The performance of “traditional” cyclical equity market sectors (i.e. excluding IT and communication services) relative to defensive sectors has correlated better with PMI new orders than industrial output, suggesting that they will lag if the PMI slides – chart 5.

Chart 5

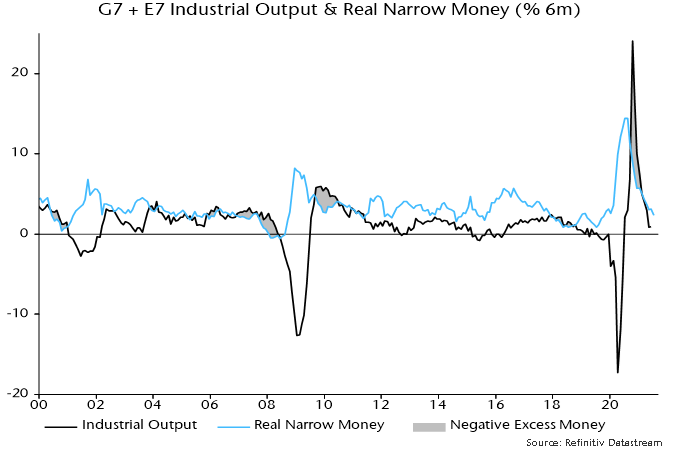

A near-term rebound in output momentum, however, could be relevant for assessing the monetary backdrop for markets. Global six-month industrial output growth fell back below real money growth in April – chart 6. The return to a positive real money / output growth gap may explain continued strength in equity market indices despite signs of economic cooling.

Chart 6

A negative cross-over, however, is possible if there is a large output catch-up effect and real money growth remains weak.

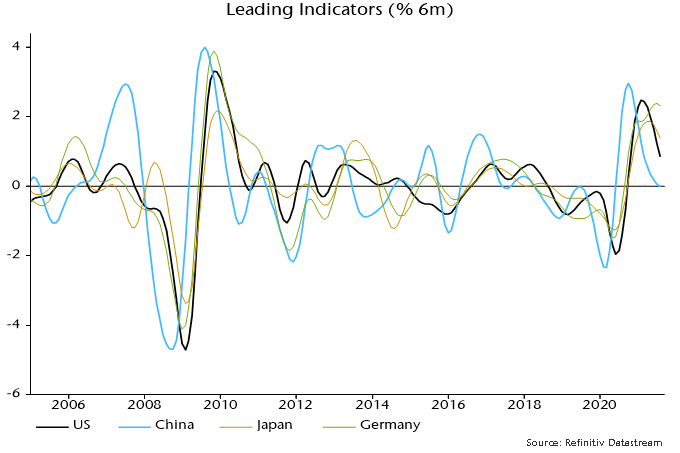

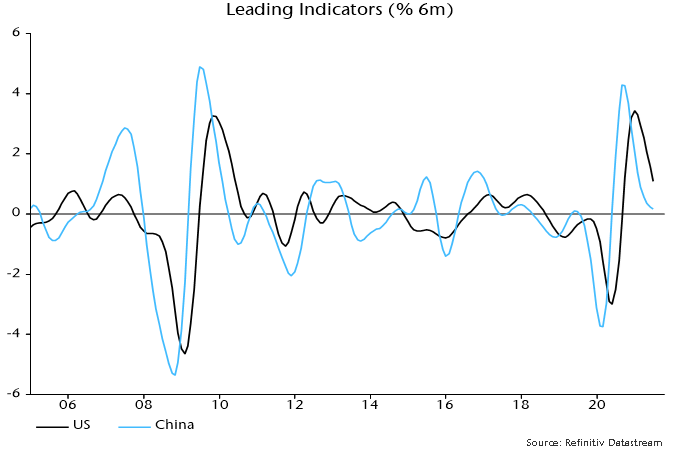

The monetary signal of an economic slowdown is starting to be confirmed by non-monetary leading indicators. Chart 7 shows six-month rates of change of composite indices based on the OECD’s methodology but calculated independently. The suggestion is that the loss of economic momentum now clearly visible in China will be mirrored in the US and the rest of the G7 in H2 2021.

Chart 7

The economic / market view here remains cautious based on 1) an expected slowdown in global industrial momentum through H2 (already apparent in Chinese data) and 2) recent less favourable “excess” money conditions.

Global six-month real narrow money growth, however, may have bottomed in May / June. A Q3 rebound would signal a stronger economy in H1 2022. An associated improvement in excess money could reenergise the reflation trade in late 2021.

The issue can be framed in cycle terms: does the recent top in the global manufacturing PMI new orders index mark the peak of the stockbuilding cycle (implying a shortened cycle) or will the peak be delayed until H1 2022?

Possible drivers of a real money growth rebound include Chinese policy easing, a slowdown in global consumer price momentum and a pick-up in US / Eurozone bank loan expansion.

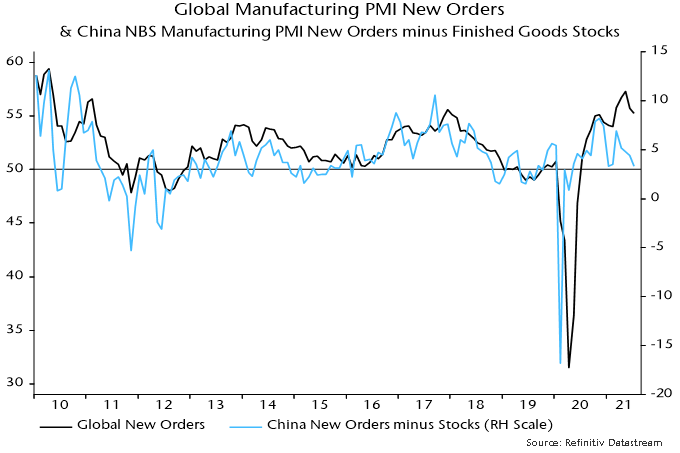

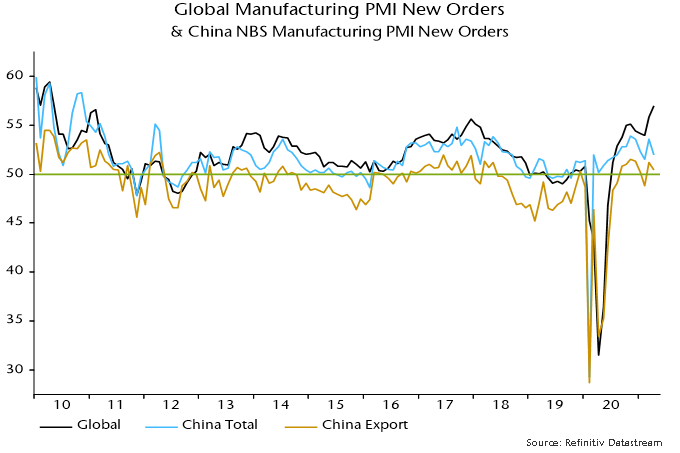

The H2 industrial slowdown view remains on track. The global manufacturing PMI new orders index fell further in July, confirming May as a top. Chinese orders were notably weak and have led the global index since the GFC – see chart 1.

Chart 1

Global six-month real narrow money growth fell steadily between July 2020 and May but a stabilisation in June has been confirmed by additional monetary data released over the last week – chart 2.

Chart 2

Will PBoC policy easing drive a recovery in Chinese / global money growth? The hope here was that the 15 July cut in reserve requirements would be reflected in an early further fall in money market interest rates and easier credit conditions. Three-month SHIBOR, however, has moved sideways while corporate credit availability is little changed, judging from the July Cheung Kong Graduate School of Business survey – chart 3. July money data, therefore, could show limited improvement.

Chart 3

Global six-month real money growth should receive support from a slowdown in consumer price momentum as commodity price and bottleneck effects fade. Eurozone six-month CPI inflation eased on schedule in July, with further moderation suggested and the move lower likely to be mirrored in other countries (Tokyo July numbers also showed a slowdown) – chart 4.

Chart 4

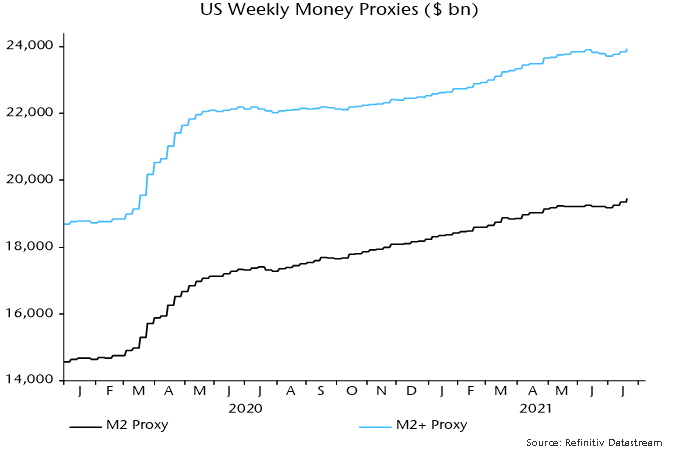

US monetary prospects are foggy. Disbursement of stimulus payments boosted nominal money growth over March-May but there was a sharp slowdown in June. Weekly data indicate a reacceleration in July as the Treasury ran down its cash balance at the Fed to comply with debt ceiling legislation – chart 5. This effect, however, will be temporary and an improving fiscal position suggests a reduced contribution from monetary financing during H2 and into 2022.

Chart 5

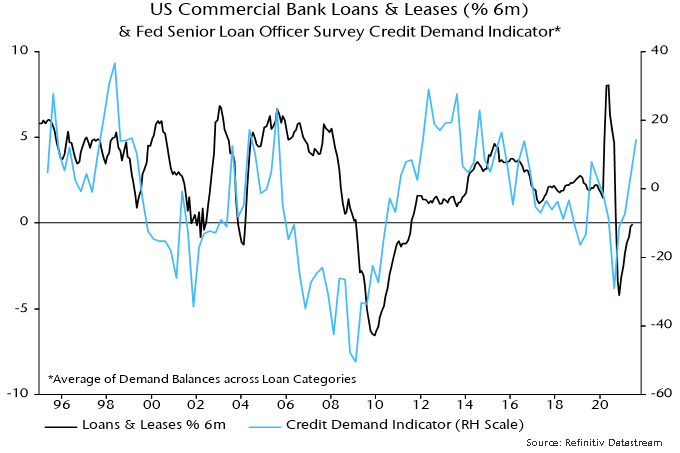

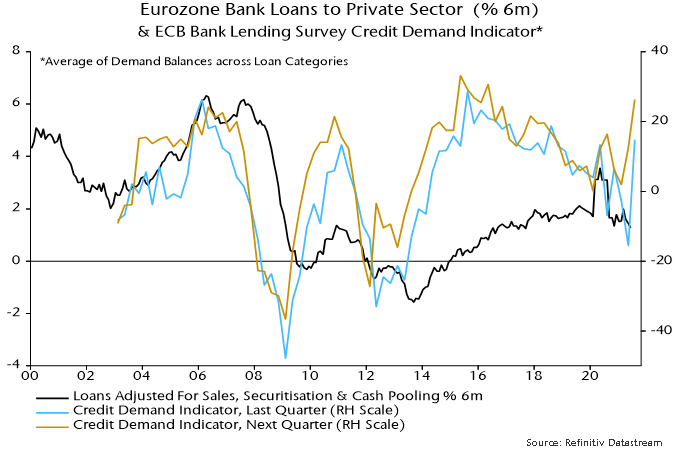

Stable or higher US money growth, therefore, may require a pick-up in bank loan expansion. The Fed’s July senior loan officer survey, released yesterday, is hopeful, showing a further improvement in demand balances across most loan categories (not residential mortgages) – chart 6. The ECB’s July lending survey gave a similar message – chart 7. The survey indicators, however, are directional and the magnitude of a likely loan growth pick-up is uncertain. Actual lending data remained soft through June.

Chart 6

Chart 7

Failure of global real money growth to recover in Q3 – and especially a further slowdown – would suggest that the stockbuilding cycle is already at or close to a peak. The cycle bottomed in Q2 2020 and – based on its average historical length of 3.33 years – might be expected to reach another low in H2 2023, in turn implying a peak no earlier than H1 2022. As previously discussed, however, the current upswing could be short to compensate for a long (4.25 years) prior cycle.

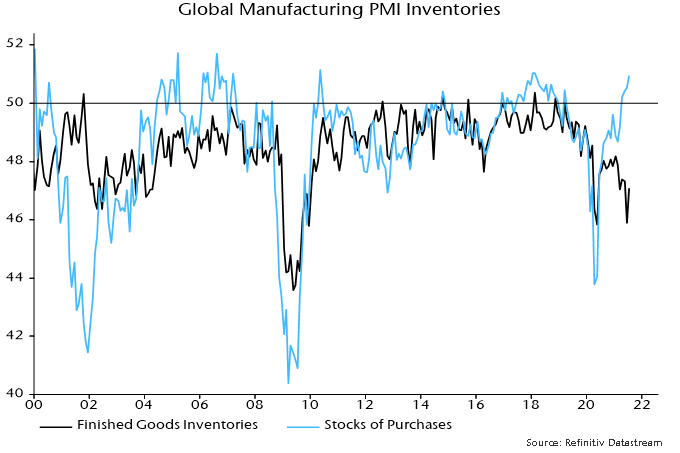

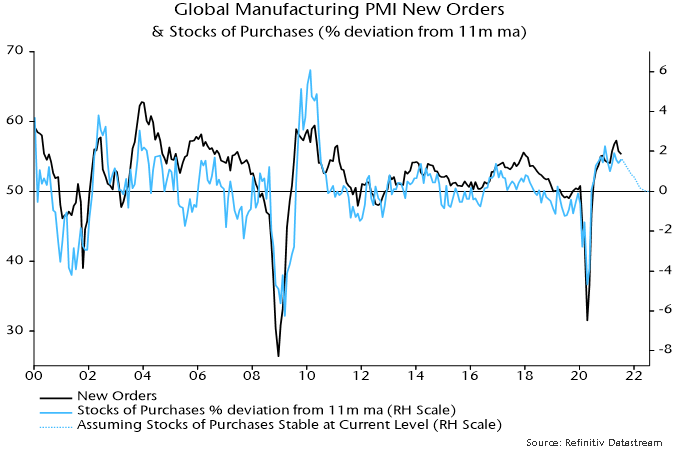

Proponents of the consensus view that replenishment of stocks will underpin solid industrial growth in H2 cite the still-low level of the global manufacturing PMI finished goods inventories index – chart 8. Research conducted here, however, indicates that the stocks of purchases index (i.e. raw materials / intermediate goods) is a better gauge of the stockbuilding cycle and tends to lead the finished goods index. The former index is already at a level consistent with a cycle top and the rate of change relationship with the new orders index is another reason for expecting orders to weaken significantly during H2 – chart 9.

Chart 8

Chart 9

Global six-month real narrow money growth appears to have moved sideways in June and could be bottoming after a 10-month slide. If confirmed, and allowing for the usual lead time, this would suggest a stabilisation of industrial momentum in early 2022 following a H2 2021 slowdown.

The June real narrow money growth estimate is based on monetary data covering 70% of the G7 plus E7 aggregate tracked here and near-complete inflation numbers. The prior fall in real money growth is expected to be reflected in “surprising” weakness in global PMI manufacturing new orders and other coincident indicators of industrial momentum during H2 2021 – see chart 1.

Chart 1

Global stabilisation conceals a June recovery in Chinese six-month real narrow money growth offset by further slowdowns in the US and Japan, with European data yet to be released – chart 2.

Chart 2

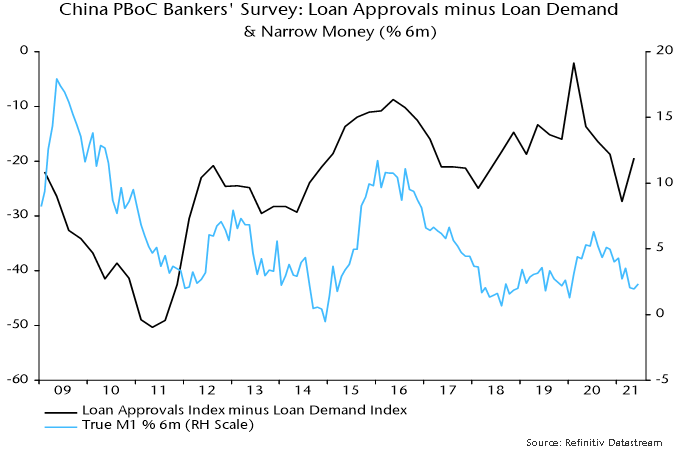

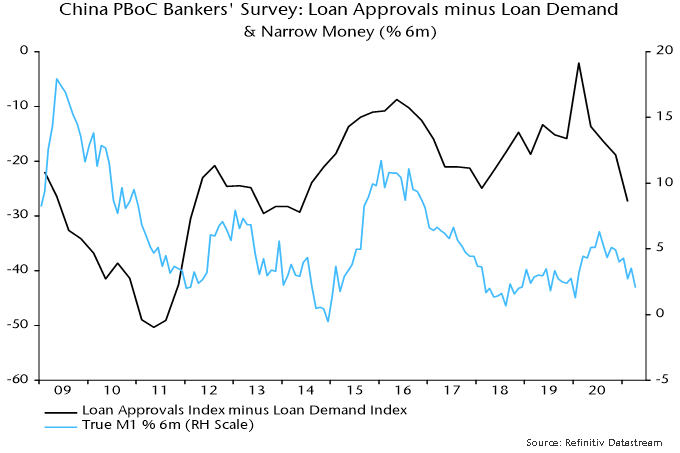

The recent cut in reserve requirements is judged here to confirm a trend shift in Chinese monetary policy, probably heralding a sustained rebound in money growth. Another indication of a policy turn is a rise in the differential between the loan approvals and loan demand indices in the PBoC Q2 bankers’ survey, suggesting that banks have been instructed to loosen credit – chart 3.

Chart 3

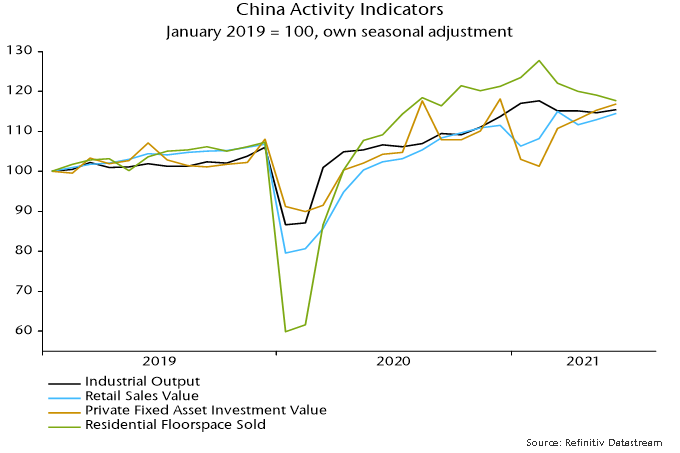

Street claims that last week’s Chinese activity data were solid, implying no need to adjust policy settings, are puzzling. GDP grew by only 3.4% annualised between Q4 and Q2. Monthly indicators are stagnant in real seasonally adjusted level terms – chart 4.

Chart 4

The view here is that the economy faced a “hard landing” without a policy change but the authorities have recognised the risk and will act to avert it.

Support to global real money growth from Chinese easing should be supplemented by a slowdown in global six-month CPI inflation in H2, assuming stable commodity prices – chart 5. Commodity prices could weaken as industrial activity decelerates.

Chart 5

China continues to lead US / global economic momentum. The six-month rate of change of the OECD’s US leading indicator peaked four months after that of a Chinese indicator – chart 6*. This fits with a four-month interval between peaks in 10-year government bond yields – November in China, March in the US.

Chart 6

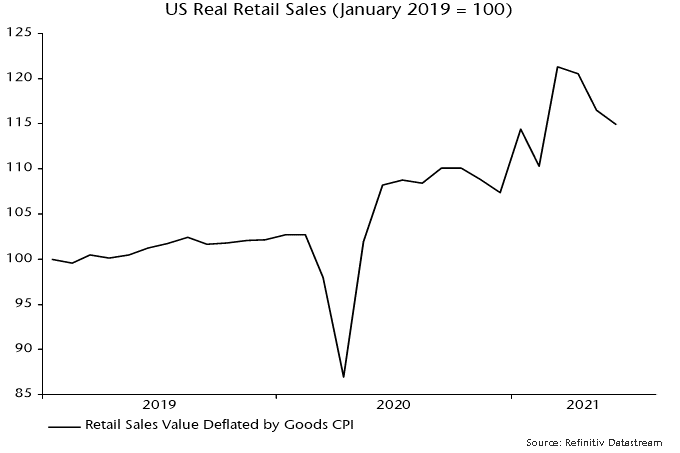

Street descriptions of US June retail sales as “robust” are also questionable. With prices surging, sales fell for a third month in real terms, consisent with a fading boost from March / April stimulus payments – chart 7.

Chart 7

Markets have already partially discounted a H2 economic slowdown, with quality stocks outperforming and bullish flattening of yield curves. Non-tech cyclical sectors of developed equity markets have so far held up against defensive sectors and could be the next shoe to drop – chart 8.

Chart 8

*The indicators shown use the OECD’s methodology but are calculated independently.

Monetary trends continue to suggest a slowdown in global industrial momentum in H2 2021, with a rising probability that weakness will be sustained into H1 2022 – contrary to the prior central view here that near-term cooling would represent a pause in a medium-term economic upswing. Pro-cyclical trends in markets have corrected modestly but reflationary optimism remains elevated, indicating potential for a more significant setback if economic data disappoint. Chinese monetary policy easing is judged key to stabilising global prospects and reenergising the cyclical trade.

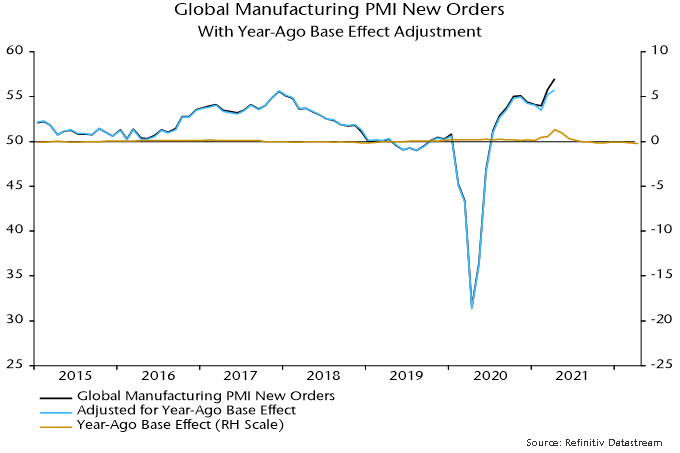

Global six-month real narrow money growth – the “best” monetary leading indicator of the economy – peaked in July 2020 and extended its fall in May, dashing a previous hope here of a Q2 stabilisation / recovery. This measure typically leads turning points in the global manufacturing PMI new orders index by 6-7 months but a PMI peak was delayed on this occasion by a combination of US fiscal stimulus and economic reopening. A June fall in new orders, however, is expected to mark the start of a sustained decline, confirming May as a significant top – see chart 1.

Chart 1

The magnitude of the fall in global real narrow money growth and its current level suggest a move in the manufacturing new orders index at least back to its long-run average of 52.5 during H2 (May peak = 57.3, June = 55.8).

China continues to lead global monetary / economic trends, as it has since the GFC. A strong recovery in activity through 2020 prompted the PBoC to withdraw stimulus in H2, resulting in a money / credit slowdown that has fed through to weaker H1 2021 economic data. The central bank, however, has been reluctant to change course, partly to avoid fuelling house and commodity price speculation, and six-month real narrow money growth has now fallen to a worryingly low level, suggesting rising risk of a “hard landing” in H1 2022 – chart 2.

Chart 2

Real narrow money growth remains above post-GFC averages in other major economies but has also fallen significantly, reflecting both slower nominal expansion and a sharp rise in consumer price inflation. Six-month inflation is likely to fall back during H2 but nominal trends could weaken further in response to higher long-term rates and as money-financed fiscal stimulus moderates.

The suggestion from monetary trends of a deeper and more sustained economic slowdown could be argued to be inconsistent with cycle analysis. In particular, the global stockbuilding or inventory cycle bottomed in Q2 2020 (April) and, based on its 40-month average length, might be expected to remain in an upswing through early 2022, at least. This understanding informed the previous view here that a cooling of industrial momentum in mid-2020 would prove temporary.

A reassessment, however, may be warranted to take account of the distorting impact of the covid shock, which stretched the previous cycle to 50 months. A compensating shortening of the current cycle to 30 months would imply a cycle mid-point – and possible peak – in July 2021.

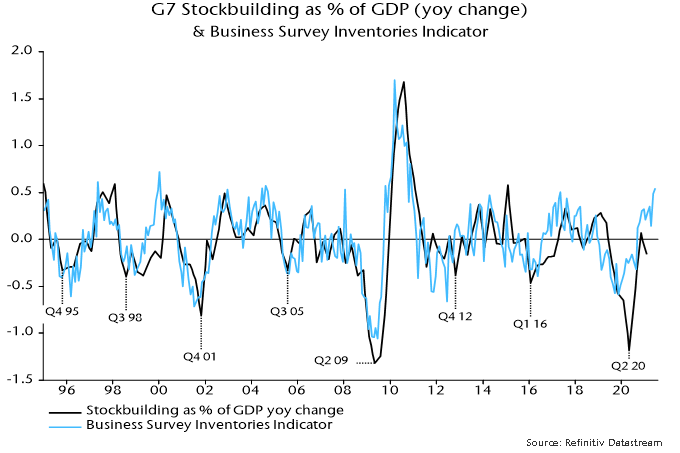

This alternative assessment is supported by a rise in the business survey inventories indicator monitored here to a level consistent with prior cycle peaks – chart 3.

Chart 3

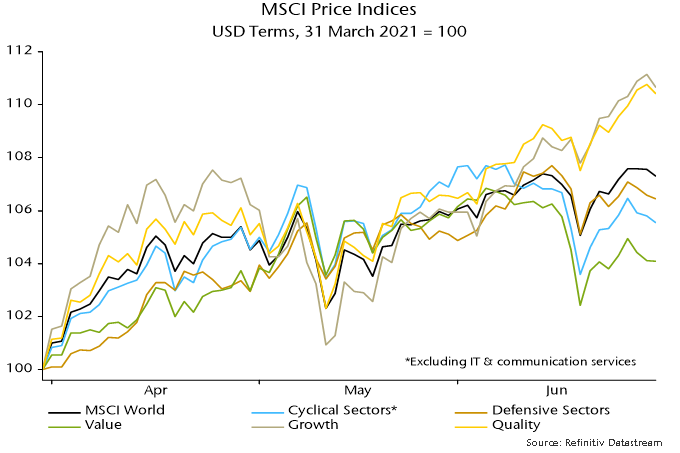

The previous quarterly commentary suggested that cyclical equity market sectors and value were less attractive in the context of an approaching PMI peak, while quality stocks had potential to rally. MSCI World non-tech cyclical sectors lagged defensive sectors during Q2, with quality and growth outperforming value – chart 4. These trends could extend if the slowdown scenario described above plays out. Chinese policy easing would support the cyclical / value trade but the impact could prove temporary unless the Chinese shift resulted in an early rebound in global real narrow money growth.

Chart 4

Counter-arguments to the relatively pessimistic economic view outlined above include the following:

1. Fiscal policy remains highly expansionary and will offset monetary weakness.

Response: Economic growth is related to the change in the fiscal position and deficits, while large, are falling in most countries. Even in the US, President Biden’s stimulus package served mainly to neutralise a potential drag as earlier measures expired. The US fiscal boost peaked with the disbursement of stimulus cheques in March / April.

2. Household saving rates and money balances are high, implying pent-up consumer demand.

Response: Savings rates have been temporarily inflated by government transfers and will normalise as these fall back and consumption recovers to its pre-covid level. High money balances probably reflect “permanent” savings. US households planned to spend only 25% of the most recent round of stimulus checks, according to the New York Fed, using the rest to increase savings and reduce debt. The implied spending boost has already been reflected in retail sales, which may fall back in Q3.

3. Services strength as economies reopen will offset any industrial slowdown.

Response: The services catch-up effect is temporary and momentum is likely to reconnect with manufacturing in H2. Industrial trends dominate economic fluctuations and equity market earnings.

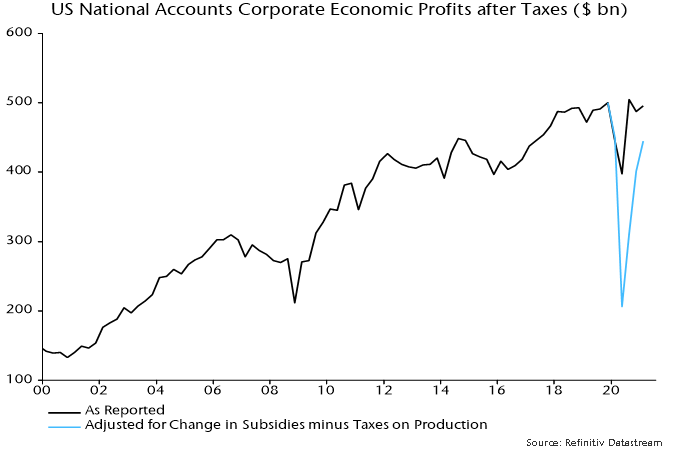

4. Profits are rising strongly, with positive implications for business investment and hiring.

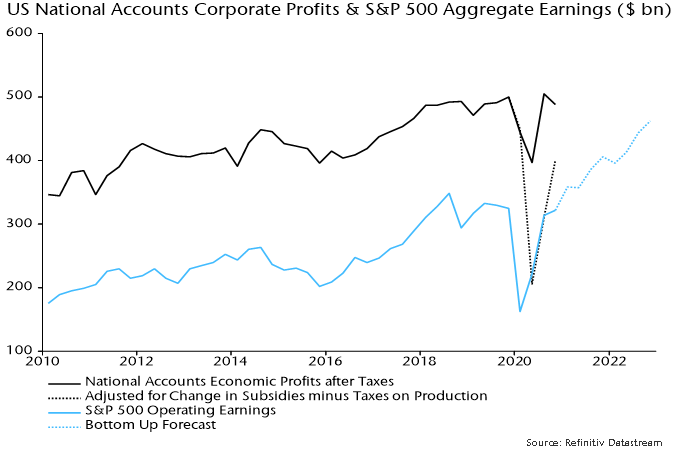

Response: Profits are still receiving substantial support from government subsidies, withdrawal of which will offset much of the additional boost from economic normalisation. An increase in net subsidies relative to their Q4 2019 level accounted for 10% of US post-tax corporate economic profits in Q1, according to national accounts data – see chart 4.

Chart 5

5. Inventories to shipments ratios remain low, implying that the stockbuilding cycle is far from peaking.

Response: Economic growth is related to the change in stockbuilding, not its level. Stockbuilding is highest when inventories are low – the subsequent fall is a drag on growth even though stockbuilding usually remains high until inventories normalise. Low inventories to shipments ratios, therefore, are consistent with a cycle peak.

6. Industry has been held back by supply constraints – output and new orders will surge as these ease.

Response: Supply difficulties have probably resulted in firms placing multiple orders for inputs, inflating PMI readings – this effect will unwind as bottlenecks ease. Historically, manufacturing PMI new orders have fallen, not risen, following a peak in supply constraints.

7. Rising inflation will boost bond yields, supporting cyclical / value outperformance.

Response: Last year’s global money surge was expected here to be reflected in high inflation in 2021-22 but six-month broad money growth has moved back towards its pre-covid average, suggesting that medium-term inflation risks are receding. Bond yields usually track industrial momentum more closely than inflation data so would probably remain capped in a slowdown scenario even if inflation news continues to surprise negatively.

A case can be made that the most pressing monetary policy issue globally is the timing not of Fed tightening but rather of PBoC easing.

The mainstream view at the start of the year was that China would continue to lead a global economic recovery, resulting in a further withdrawal of monetary and fiscal policy support.

Chinese economic data have disappointed consistently – including May activity numbers this week – but the consensus has maintained a forecast of policy tightening, albeit later than originally expected.

The “monetarist” view, by contrast, is that the PBoC had already moved to a restrictive monetary stance during H2 2020. This was reflected in a money / credit slowdown late last year, which has fed through to a loss of economic momentum in H1 2021.

The PBoC was judged likely to recognise rising downside risks by easing policy by mid-year. Money market rates have been allowed to drift lower since February but May monetary data suggest that policy adjustment has been “too little, too late”.

Six-month growth rates of money and credit fell further last month, signalling likely continued nominal GDP deceleration through year-end, at least – see chart 1.

Chart 1

Weakness is more pronounced in real terms: narrow money has barely kept pace with consumer prices over the last six months and has fallen by 5.5% relative to producer prices – chart 2.

Chart 2

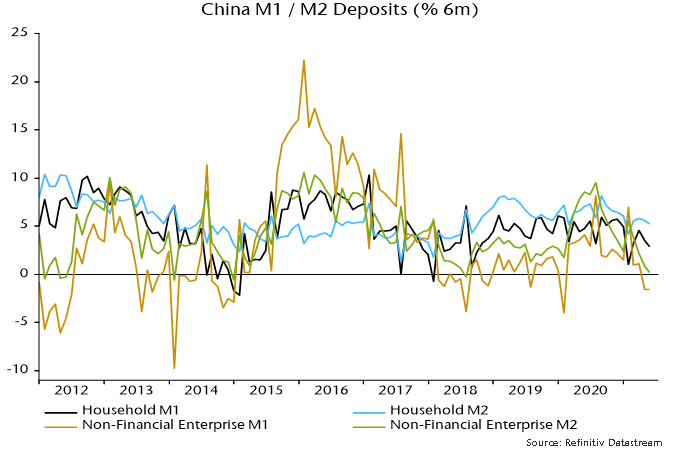

The liquidity squeeze is focused on companies. M2 deposits of non-financial enterprises have stagnated over the last six months, while M1 deposits have fallen – chart 3. Nominal weakness is comparable with 2014 and 2018 – ahead of major economic slowdowns – but real money balances are under greater pressure now, reflecting surging input costs.

Chart 3

The bias here has been to give the PBoC the benefit of the doubt and assume that easing would occur early enough to head off serious economic weakness. Increased pessimism is warranted unless action is forthcoming soon.

Additional country releases in recent days confirm that global six-month real narrow money growth fell further in April, to its slowest pace since January 2020 – see chart 1. The decline from a peak in July 2020 is the basis for the forecast here of a significant cooling of global industrial momentum during H2 2021.

Chart 1

The April fall reflected both slower nominal money growth and a further pick-up in six-month consumer price momentum – chart 2. The latter is probably at or close to a short-term peak and the central scenario here remains that real money growth will stabilise and recover into Q3. The risk is that nominal money trends continue to soften – the boost to US numbers from disbursement of stimulus payments may be over and this year’s rise in longer-term yields may act as a drag.

Chart 2

Six-month growth of real broad money and bank lending also moved down in April, with the former close to its post-GFC average and the latter considerably weaker – chart 3. Forecasts last year that government guarantee programmes would lead to a lending boom have so far proved wide of the mark; monetary financing of budget deficits, mainly by central banks, remains the key driver of broad money expansion.

Chart 3

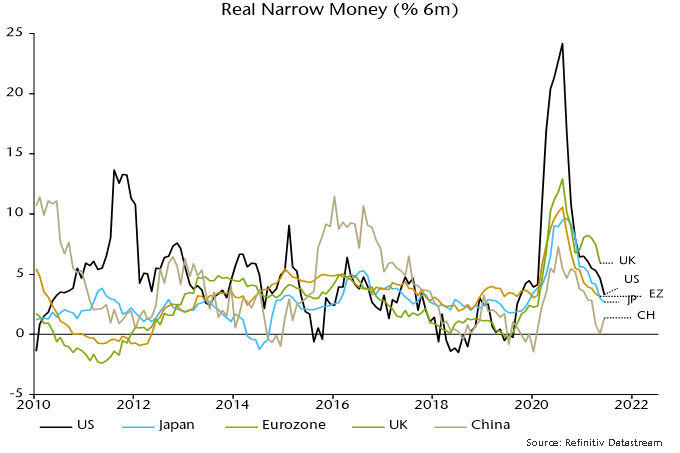

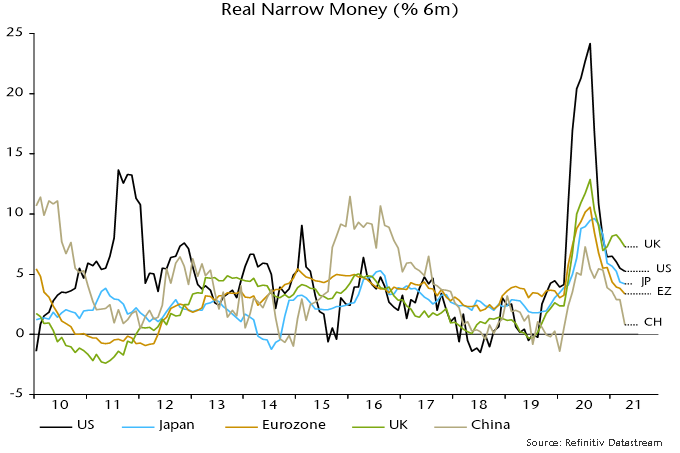

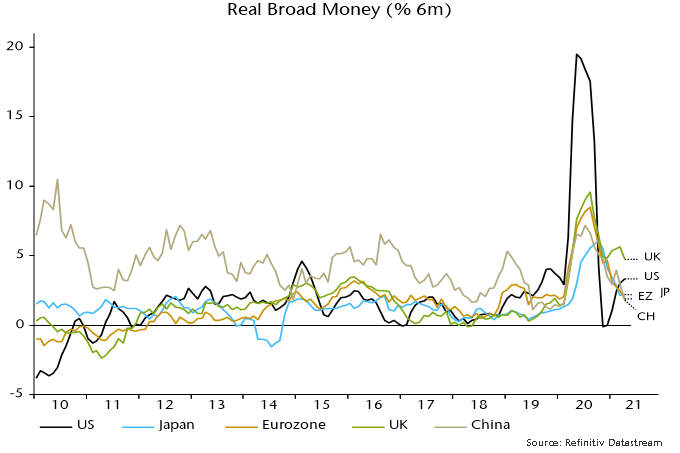

Charts 4 and 5 shows six-month growth rates of real narrow and broad money in selected major economies. The UK remains at the top of the range on both measures, supporting optimism about near-term relative economic prospects, although slowing QE and a sharp rise in inflation promise to erode the current lead.

Chart 4

Chart 5

Eurozone real money growth, by contrast, is relatively weak: monetary deficit financing has been on a smaller scale than in the US / UK, while six-month inflation is higher than in the UK / Japan. Bank lending has been expanding at a similar pace in the Eurozone and UK. The recent step-up in ECB PEPP purchases could lift Eurozone broad money growth although the change is modest and could be offset by an increased capital outflow – see previous post.

China remains at the bottom of the ranges and monetary weakness was expected here to trigger PBoC easing by mid-year. Policy shifts usually proceed “under the radar” via money market operations and directions to state-run banks. The managed decline in three-month SHIBOR continued this week, while the corporate financing index in the Cheung Kong Graduate School of Business survey stabilised in April / May after falling over October-March, which could be a sign that banks have been instructed to increase loan supply.

The PBOC’s quarterly bankers’ survey, due for release later this month, could provide further corroboration of a policy shift: the differential between loan approval and loan demand indices leads money growth swings – chart 6. Monetary reacceleration in China remains the most likely driver of a rebound in global six-month real narrow money growth – required to support a forecast that H2 industrial cooling will represent a pause in an ongoing upswing rather than a foretaste of more significant weakness in 2022.

Chart 6

The forecast here at the start of the year was that the global manufacturing PMI new orders index – a key indicator of industrial momentum – would reach a peak in early 2021 and fall into the summer. The index declined slightly between November and February but rose to a new recovery high in March, with flash data last week and today’s Chinese results indicating a further significant increase in April. What has gone wrong?

The expectation of an early 2021 peak and subsequent relapse was based on a fall in global six-month real narrow money growth from an extreme peak in July 2020 – real money growth has led turning points in PMI new orders by 6-7 months on average historically. Six-month real narrow money momentum continued to weaken into March, so the monetary signal for PMI direction remains negative – see first chart.

Chart 1

There was meaningful variation around the 6-7 month historical average lead time. An April PMI new orders peak, were it to be confirmed, would imply a nine-month lead, which would be within one standard deviation of the average. So the further rise into April is not yet an unusual departure from the norm.

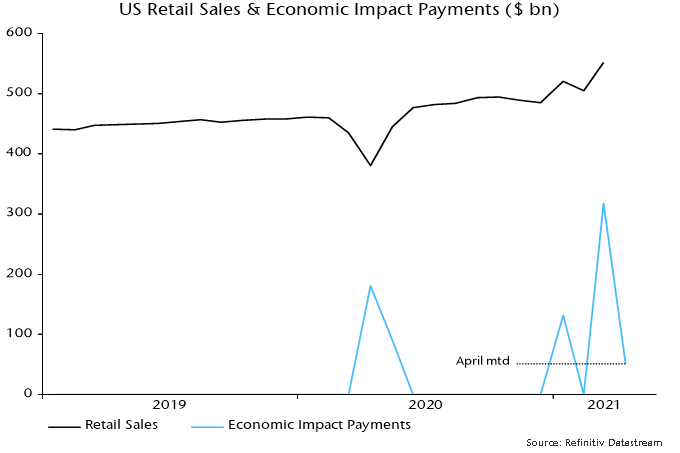

The most likely explanation is that the PMI upswing has been extended by US fiscal stimulus – particularly the third round of payments to households – along with initial moves towards economic reopening in the US, UK and other countries showing progress in virus containment. A 9.3% monthly surge in US retail sales in March may have been a key driver of stronger March / April new orders.

“Economic impact payments” authorised by the American Rescue Plan Act were $318 bn in March and $51 bn through 28 April for a total $369 bn, representing the bulk of a programme costed at $411 bn by the Congressional Budget Office.

New York Fed analysis of data collected in its monthly survey of consumer expectations indicates that households have spent or plan to spend 25% of the windfall, similar to the proportion in the first and second rounds, with remainder used to increase savings (42%) or pay down debt (34%). Rounding the $369 bn received to date up to $400 bn, this suggests additional consumer outlays of about $100 bn.

Assume that half of this amount is spent on goods, which could be an overestimate given that services account for two-thirds of total consumption. That would suggest additional retail sales – a rough proxy for goods spending – of about $50 bn. Monthly sales jumped by $47 bn between February and March. The suggestion is that the bulk of the boost to goods spending has already occurred and sales will fall back sharply into the summer.

Chart 2

An additional technical explanation for the March / April rise in PMI new orders is a positive base effect from the slump in the index to a low in April 2020. Survey respondents are asked to draw a comparison with the previous month but there is evidence that some replies take into account the level of business in the same month a year earlier – understandable in cases where there is a strong seasonal pattern in demand.

Specifically, a regression of the global manufacturing PMI new orders index on its one- and 12-month lagged values finds a small but statistically significant negative coefficient on the latter*. The coefficient suggests that a 13.7 point plunge in the index in March / April 2020 contributed 0.8 of a point to the estimated 3.0 point increase in March / April 2021 – third chart. This boost will reverse by June, reflecting the recovery in the index after April last year.

Chart 3

With global real narrow money growth still moderating, the US fiscal boost probably passing its maximum and China still on a slow growth path pending PBoC easing, the forecast here of a PMI pullback through late Q3 is maintained.

Chart 4

*The same result is obtained using US ISM manufacturing new orders data over a much longer sample.

The consensus has swung from pessimism about prospects for corporate profits in 2020 to likely excessive optimism now. Analysts, in particular, may underappreciate the contribution to recent profits resilience of government subsidies, withdrawal of which may offset much of the benefit of economic normalisation.

Posts here last year suggested that global profits would mirror V-shaped rebounds in retail sales and industrial output. S&P 500 aggregate operating earnings are likely to have risen above their pre-pandemic peak in Q1 2021, based on results to date and analyst estimates, according to S&P. Analyst forecasts imply growth of 29% between Q1 and Q4 2022 – see first chart.

Chart 1

S&P 500 operating earnings are equivalent to about 60% of corporate post-tax economic* profits in the national accounts and the two series follow a similar path. An attribution analysis, however, is available for the national accounts measure, allowing the recent contribution of higher subsidies and reduced taxes on production to be separated out.

As of Q4 2020, national accounts profits were 2.4% below their pre-pandemic peak in Q4 2019. If subsidies / production taxes had remained unchanged, the shortfall would have been 19.8%. Put differently, the rise in subsidies accounted for 17.8% of the level of profits in Q4 2020.

This direct contribution of government to profits will normalise as the economy reopens and emergency programmes are withdrawn. Assuming that the rise in subsidies since Q4 2019 is reversed, “underlying” profits – excluding the recent additional support – would need to grow by 21.7% from their Q4 2020 level to maintain overall stability. The consensus forecast of a 29% increase in S&P 500 operating earnings between Q1 2021 and Q4 2022, therefore, could require underlying growth of more than 50%.

Data later this week will show that GDP almost regained its pre-pandemic level in Q1 2021 and the FOMC’s median projection implies a further increase of more than 8% by Q4 2022. Adding in inflation at 2-3% pa suggests nominal GDP growth of about 13% – unlikely to support profits expansion of 50%.

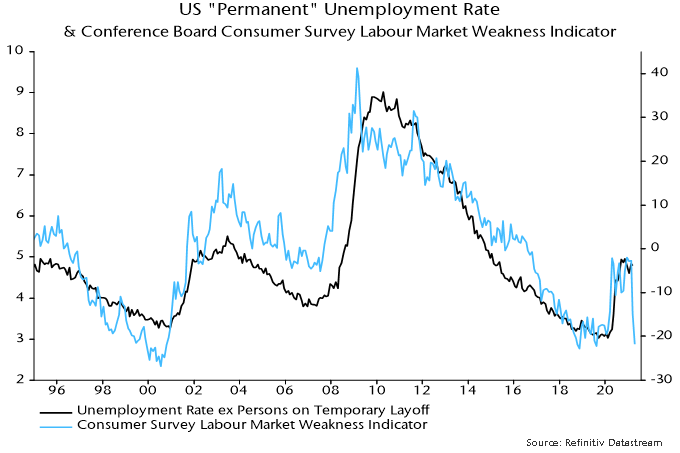

Profit margins, indeed, could be squeezed by rising labour costs. The view here has been that the labour market would return to pre-pandemic levels of tightness by late 2021, resulting in upward pressure on wage growth. Labour market responses in the April Conference Board consumer survey support the view that conditions are normalising rapidly – second chart.

Chart 2

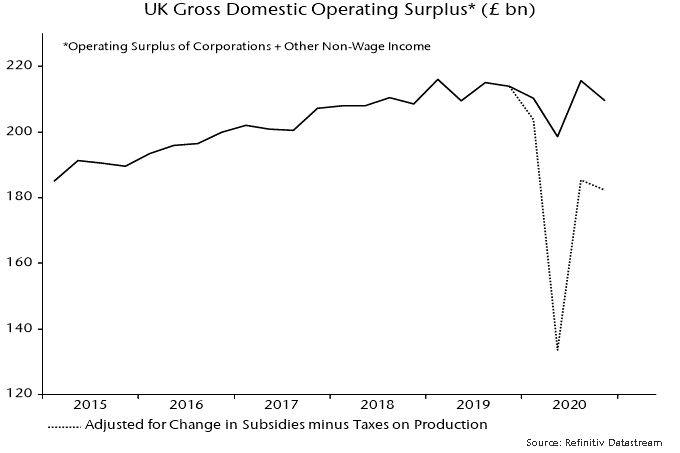

National accounts data for other G7 countries are less detailed / timely than for the US but government subsidies are likely to have provided similar or larger-scale support for profits. In the UK, the economy-wide gross operating surplus** would have been 13.0% lower in Q4 2020 without additional government subsidies / lower production taxes – third chart. The extra support amounted to 5.0% of GDP in Q4, double the equivalent in the US, reflecting the “generosity” of the UK’s furlough scheme.

Chart 3

*”Economic” = including inventory valuation and capital consumption adjustments. **This is not comparable with the US national accounts profits measure – it is gross of depreciation, interest and income taxes and includes non-corporate business income.