Investors globally have embraced global small cap equities as a source of equity diversification. Despite the name, the universe is largely comprised of companies with a market capitalization greater than US $1 billion and includes a growing number of household names in many of the local markets and some having a global brand recognition.

Key merits of global small cap

| Not that small | Over 2,600 global small cap companies have a market capitalization greater than US $1 billion |

|---|---|

| Breadth and depth | Largest stock is only 0.2% of the index and there is broader sector diversification compared to other major market indices |

| Alpha opportunities | Global small cap markets are less researched by the analyst community compared with large cap developed equity markets, which creates added value opportunities for independent research by active managers |

Background to global small cap

Global small cap stocks offer investors the ability to benefit from a unique opportunity set. The MSCI World Small Cap Index captures small cap representation across 23 developed market countries. Compared to a domestic context, the global small cap opportunities are not that small; there are 2,643 companies with a market capitalization greater than US $1 billion at December 31, 2022. There were only 209 such companies in the S&P/TSX Composite Index.

The largest individual stock in the global small cap index represents only 0.2% of the index. In contrast, the largest individual stock at the end of 2022 in the S&P/ TSX Composite Index represented 6.3% of the index.

Moreover, the largest 15 stocks in the Canadian equity market index account for 45% of the index, while the largest 15 stocks in the global small cap index represent less than 3%. It would require the largest 627 stocks to achieve 45% index representation in the global small cap index, highlighting the much broader investment opportunity set offered by the global small cap universe.

Many of the stocks in the global small cap universe are household names in their local market, and some have a global brand recognition. For example, L’Occitane, the manufacturer, marketer, and retailer of natural and organic skincare and beauty products; Samsonite, the world’s best-known and largest travel luggage company; and IWG, which offers short-term (and long-term) workspace solutions around the world, including well-known brands such as Regus.

The diversification benefits of global small cap go beyond individual stocks. While the major Canadian indices are heavily skewed to the financial, energy, and material sectors (see Figure 1), the global small cap markets provide representation across a broader range of sectors, including higher exposure to consumer discretionary (e.g., companies in the restaurant, luxury goods and travel industries) and health care.

Figure 1 – Small Cap Sector Diversification Merits

| MSCI Global Small Cap Index (%) | S&P/TSX Composite Index (%) | |

| Energy | 5.0 | 18.1 |

| Materials | 7.6 | 12.0 |

| Industrials | 19.4 | 13.3 |

| Consumer Discretionary | 12.5 | 3.7 |

| Consumer Staples | 4.7 | 4.2 |

| Health Care | 10.7 | 0.4 |

| Financials | 14.3 | 30.8 |

| Information Technology | 10.8 | 5.7 |

| Communication Services | 2.8 | 4.9 |

| Utilities | 3.2 | 4.4 |

| Real Estate | 8.9 | 2.6 |

| Total | 100 | 100 |

Source: MSCI and Thomson Reuters Datastream. Data as at December 31, 2022

Over the last 10 years, the global small cap index has achieved the strongest return, albeit with greater volatility (Figure 2). As with all markets, it is important to understand the investment risks.

Figure 2 – 10-Year Risk and Return (Ending Dec. 31, 2022)

Source: MSCI and Thomson Reuters Datastream. Note: Index returns are in Canadian dollars.

Understanding the risks

While active managers can mitigate some of the risks through research and careful selection of individual stocks, when it comes to global small caps, investors should recognize the following:

- Liquidity risk: It can take longer to trade a small cap stock compared to large cap stocks.

- Information flow: While higher insider ownership associated with small cap stocks aligns with the interests of investors, it can also lead to less transparency and flow of information common with global large cap investments.

- Credit access: Small companies do not have the same access to credit markets as larger companies, which can sometimes limit a small company from realizing its potential.

Recognizing the potential benefits

Offsetting the risks are a number of potential benefits of global small cap investments:

- Growth opportunity: For investors who can identify the next generation of small companies that grow faster and graduate into the large cap segment, the reward is significant.

- Greater alignment of interest: Global small cap companies tend to have a more focused line of business and higher insider ownership, resulting in greater alignment of interests between the owners and shareholders.

- Sector opportunity: Investors can benefit from the higher consumer discretionary and health care sector representation offered by the global small cap index. For example, consumer-spending patterns indicate the consumer discretionary sector is likely to perform well over the long term. The health care sector should also benefit from demographic aging in the developed world.

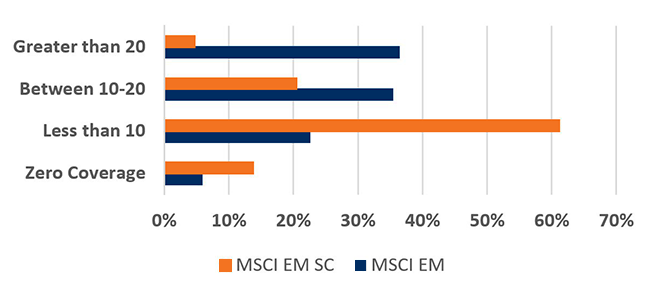

- Added value opportunity: Small cap companies also tend to be less externally researched by the analyst community. As a result, active managers have a greater opportunity to outperform their index benchmark by identifying companies whose share price does not fully reflect their intrinsic value or growth prospects. Based on the eVestment database, 71% of managers in the active global small cap universe outperformed the MSCI World Small Cap Index over the 5 years ended December 31, 2022.

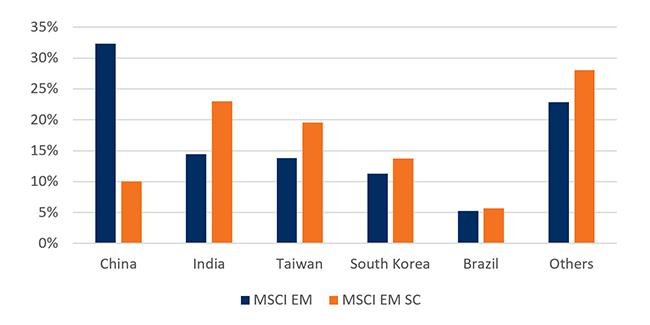

- Style offset opportunity: At the end of 2022, over 4,425 companies were in the MSCI World Small Cap Index. The broader opportunity set has led to an increased number of global small cap strategies offered by systematic (quantitative) investment managers. With a systematic approach, an investment manager is able to benefit from a breadth of understanding on a large universe of companies, compared to the depth of understanding associated with fundamental managers, who are focused on selecting a smaller number of companies to invest in. As for other equity markets, investors who can accommodate multiple managers in an asset class can benefit from the complementary systematic and fundamental styles.

Case for global small cap equities

The last several years has witnessed increased concentration in the global large cap developed equity market index. Introducing a global small cap equity component to portfolios can provide a complimentary source of diversification, a broader opportunity set of less externally researched companies, and thereby offering the potential for delivering returns above the index through active management.