The forecast of global manufacturing acceleration into H1 2025 is playing out but lagged money trends suggest that the pick-up will stall over the spring / summer before resuming in late 2025. A trade war could turn a stall into a more serious set-back.

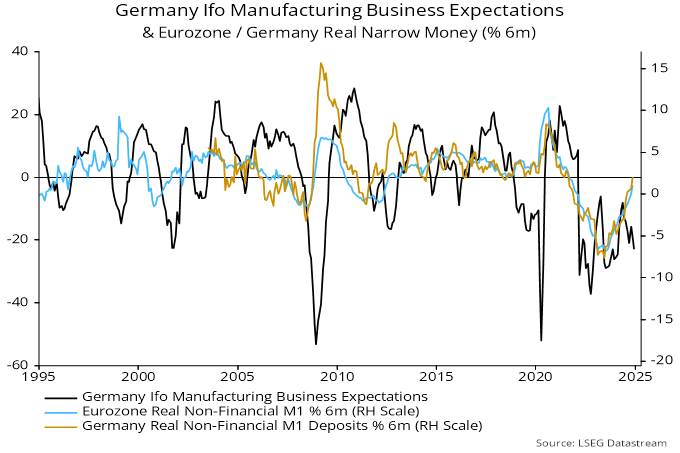

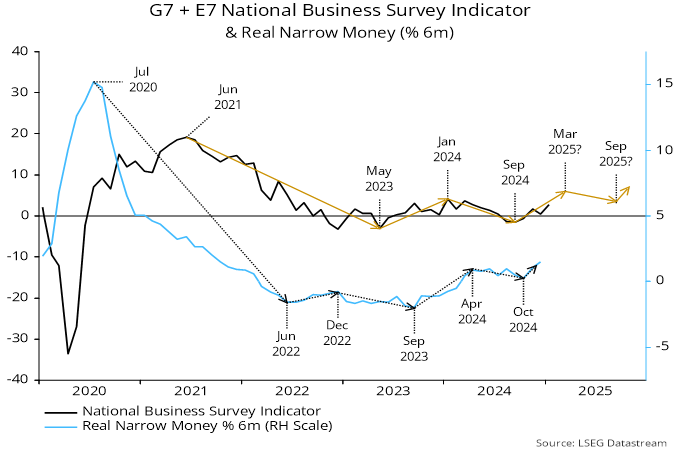

The global manufacturing PMI new orders index crossed back above the 50 level in January, reaching its highest level since May. An alternative indicator combining new orders or output expectations components of national business surveys (ISM for the US, Ifo for Germany, CBI for the UK etc) mirrored the PMI increase – see chart 1.

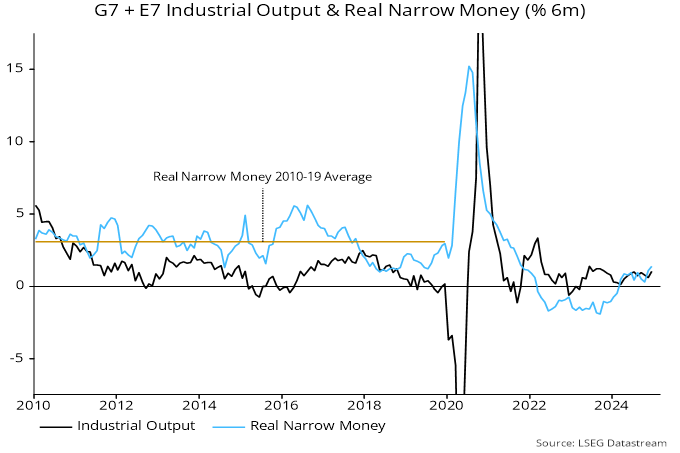

Chart 1

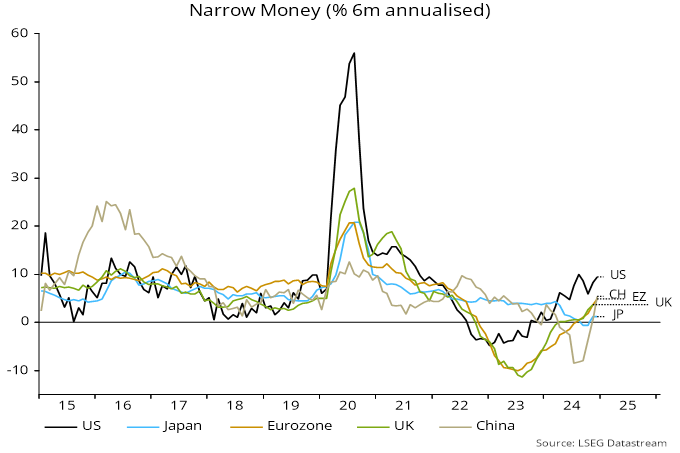

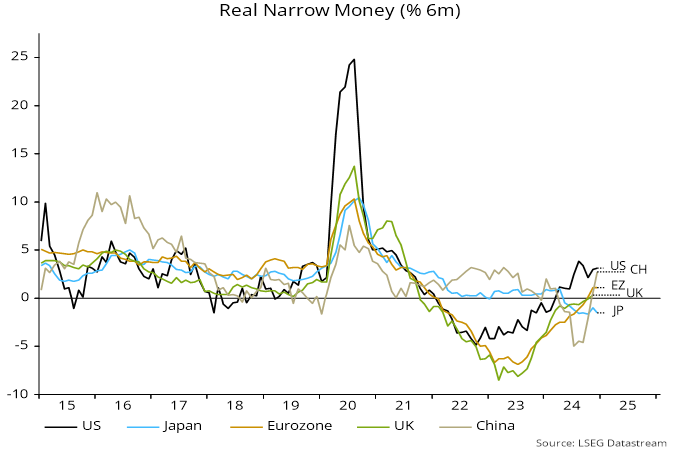

The forecast of a pick-up was based on a rise in global six-month real narrow money momentum from September 2023 through April 2024. Turning points in real money momentum have led survey turning points by 11-13 months in recent years. The survey lows in September 2024 arrived on schedule – chart 2.

Chart 2

The leading relationship had been the basis for an earlier forecast of a “double dip” in the survey indicators into H2 2024.

The upswing in six-month month real narrow money momentum, however, stalled between April and October 2024, before resuming in November / December. Based on recent lead times, this suggests a local peak in PMI new orders / the alternative indicator around March 2025 and a minor fall through Q3.The latest money numbers are giving a positive signal for late 2025.

This profile, of course, takes no account of possible trade disruption from a US-led global tariff war, which could accentuate mid-year weakness and might also affect monetary prospects (to the extent that negative confidence effects cause households and firms to defer spending, reducing their demand to hold narrow money).

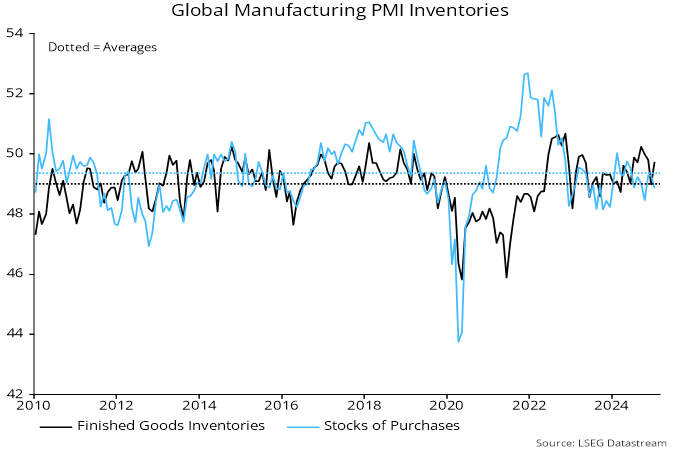

An alternative explanation for the recent manufacturing pick-up is that demand / production has been pulled forward as importers stockpile ahead of new or higher tariffs. Inventories components of business surveys, however, don’t currently suggest unusual behaviour – chart 3.

Chart 3

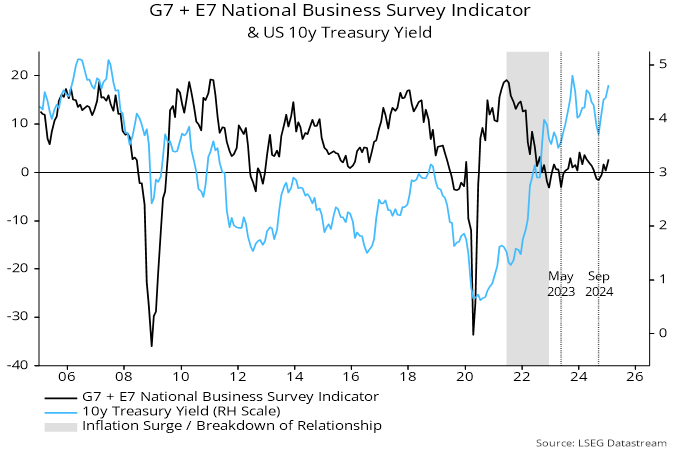

The forecast of a minor peak in global manufacturing momentum this spring could imply relief for US Treasuries.

The low / stable inflation environment of the 2010s was associated with a strong positive correlation between Treasury yields and economic momentum. This broke down in 2021-22 as surging inflation became the dominant driver of yields – chart 4.

Chart 4

With inflation normalising, the 2010s relationship may be returning. Lows in the business survey indicator in May 2023 and September 2024 were reflected in nearby lows in Treasury yields.

An approaching local peak in the survey indicator coupled with expected further favourable inflation news could open up downside for yields into H2.