Previous posts suggested that a recovery in US money growth would stall in Q2 / Q3 as Fed QT was no longer offset by monetary deficit financing (at least temporarily).

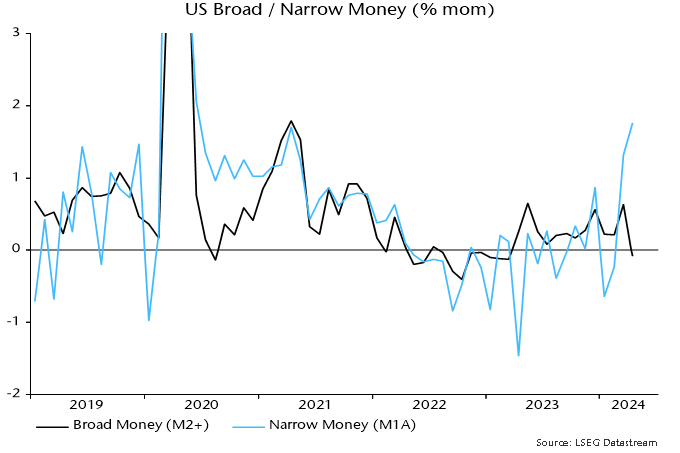

The broad M2+ measure – which adds large time deposits at commercial banks and institutional money funds to published M2 – fell by 0.1% in April, with available weekly data suggesting marginal growth in May.

Unexpectedly, however, the narrow M1A measure tracked here – comprising currency in circulation and demand deposits – rose by a bumper 1.8% in April. This follows a 1.3% gain in March – see chart 1.

Chart 1

Positive narrow money divergence typically occurs when rates are falling. Lower rates encourage a shift of money holdings from time deposits and savings accounts to demand deposits and cash. Such a shift is usually a signal of rising spending intentions.

Are money-holders front-running rate cuts? The narrow money pick-up is a hopeful signal but there is a risk that it goes into reverse if the Fed continues to delay.

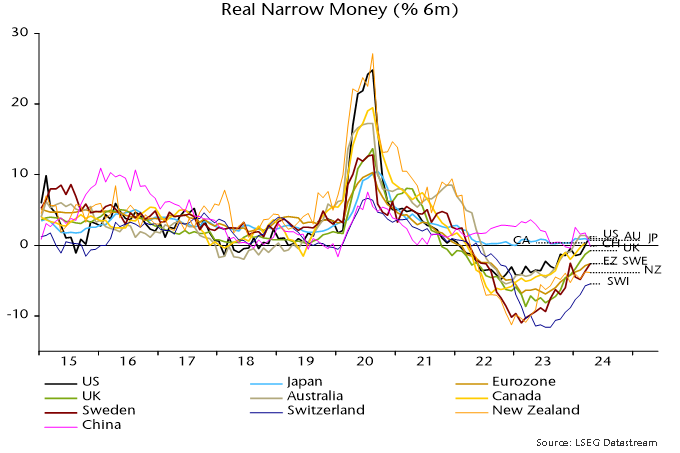

The impact of the US April rise on the global aggregate calculated here was offset by a large monthly drop in Chinese narrow money, as measured by “true M1”, which corrects for the omission of household demand deposits from official M1.

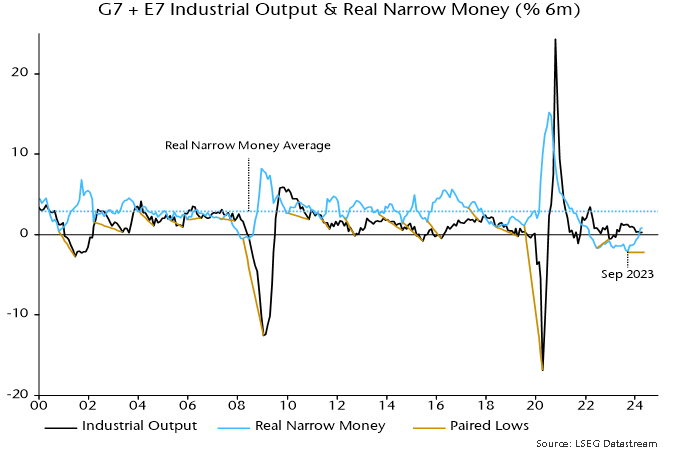

So the six-month rate of change of global real narrow money was little changed in April, following a move back into positive territory in March – see prior post for more discussion.

US six-month momentum moved to the top of the ranking across major economies in April, while China returned to negative territory – chart 2.

Chart 2

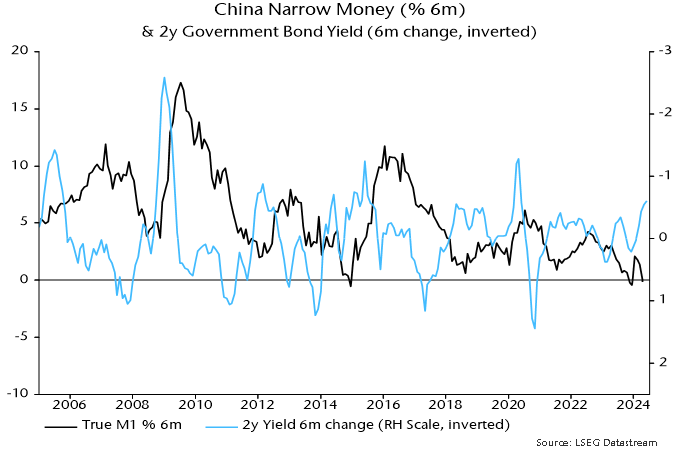

Falling interest rates suggest that the Chinese relapse will prove temporary – chart 3 – but the signal for near-term economic prospects is negative.

Chart 3

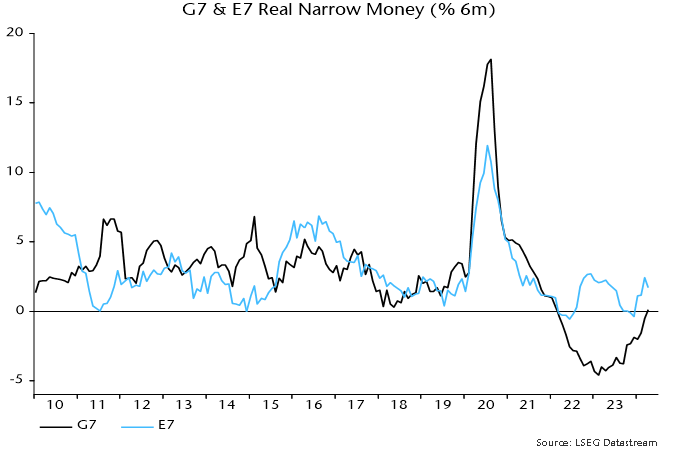

Eurozone / UK real narrow money momentum continued to recover in April but remains negative. The current UK lead may prove temporary unless the MPC follows the ECB in cutting rates soon.

The Chinese relapse resulted in E7 real money momentum falling back in April, while G7 momentum crossed into positive territory – chart 4.

Chart 4

The still-positive E7 / G7 gap coupled with a recent cross-over of global six-month real narrow money momentum above industrial output momentum could signal improving prospects for EM equities. The MSCI EM index outperformed MSCI World by 10.5% pa on average historically under these conditions.

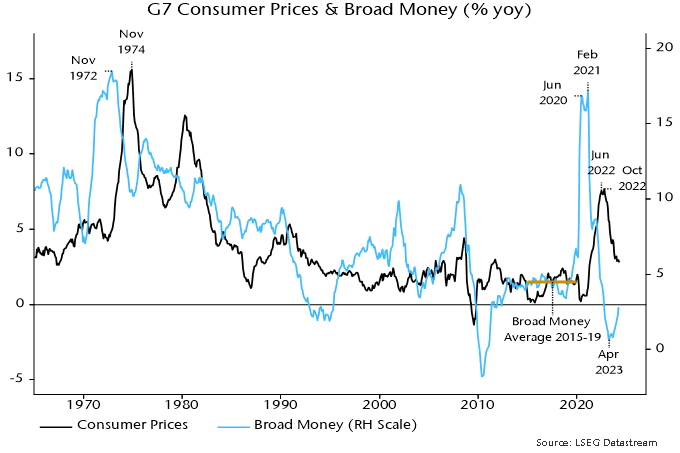

G7 annual broad money growth recovered further in April but, at 2.8%, remains well below a 2015-19 average of 4.5% – chart 5.

Chart 5

The roughly two-year leading relationship suggests that annual inflation will bottom out in H1 2025 but remain at a low level into H1 2026.