The MPC’s forecast in November was that annual CPI inflation would average 3.5% in Q2 2024 (November 2023 Monetary Policy Report (MPR), modal forecast assuming unchanged 5.25% rates). April’s drop to 2.3%, therefore, might be considered cause for celebration.

The negative market response reflected stronger-than-expected services price inflation, with the Bank of England’s “supercore” index rising by an annual 5.7%, a disappointingly small drop from 5.8% in March. This measure strips out “volatile and idiosyncratic” components, namely rents, package holidays, education and air fares.

The MPC has encouraged a focus on services inflation, citing it as one of three key gauges of “domestic inflationary persistence”, along with labour market tightness and wage growth. This prioritisation, however, is questionable, as there is no evidence that supercore leads other inflation components, whereas those components appear to contain leading information for supercore.

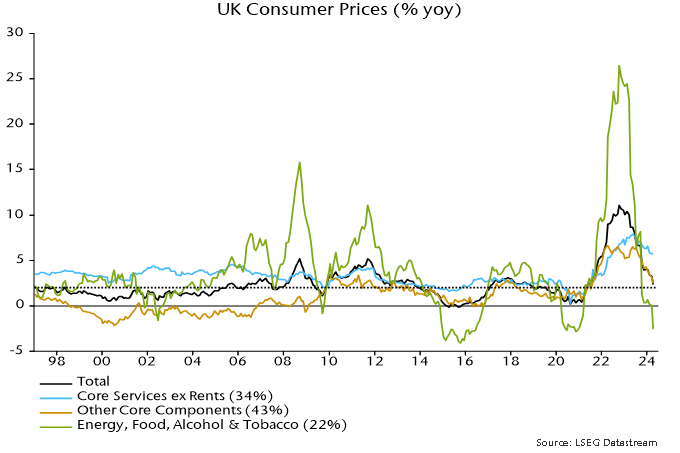

Chart 1 shows annual rates of change of three CPI sub-indices: supercore services (34% weight); other components of the core CPI index, i.e. core goods and non-supercore services (43%); and energy, food, alcohol and tobacco (22%).

Chart 1

Correlation analysis of this history suggests that supercore follows the other two series: correlation coefficients are maximised by applying a five-month lag on the other core components measure and a four-month lag on energy / food inflation.

Granger-causality tests show that inflation rates of the other core components sub-index and energy / food are individually significant for forecasting supercore. By contrast, supercore terms are insignificant in forecasting equations for the other two sub-indices*.

These results admittedly are strongly influenced by post-2019 data: supercore lagged the inflation upswing and peaked later than the other components.

A notable finding is that supercore inflation has been more sensitive to changes in energy / food prices that the rest of the core index, conflicting with the notion that it is a purer gauge of domestic inflationary pressure. This is partly explained by the one-third weight of catering services in the supercore basket: the associated price index is strongly correlated with food prices.

A forecasting equation for supercore including both other sub-indices predicts a fall in annual inflation to 4.7% in July.

The latest MPR claims that monetary trends are of limited use for inflation forecasting over policy-relevant horizons. Lagged terms in broad money growth, however, are significant when added to the above forecasting equation. The July prediction is lowered to 4.5% with this addition.

A fall in annual supercore inflation to 4.7% in July would imply a dramatic slowdown in the three-month annualised rate of change (own seasonal adjustment), from over 6% in April to below 3%.

A “monetarist” view is that aggregate inflation trends reflect prior monetary conditions, with the distribution among components determined by relative demand / supply considerations. From this perspective, supercore strength is partly the counterpart of weakness in the other sub-indices. Headline CPI momentum continues to track the profile of broad money growth two years ago, a relationship suggesting a further easing of aggregate inflationary pressure into H1 2025 – chart 2.

Chart 2

*The regressions are based on 12-month rates of change and include lags 3, 6, 9 and 12 of the dependent and independent variables.