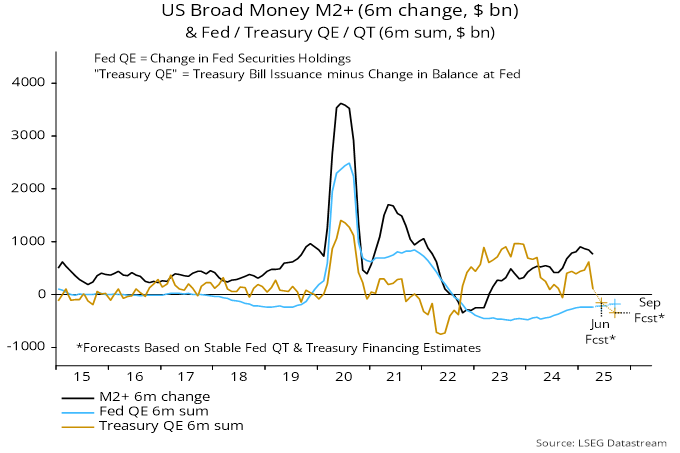

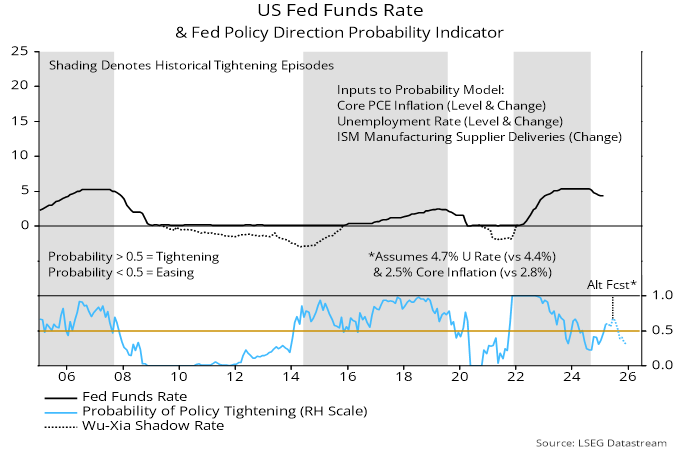

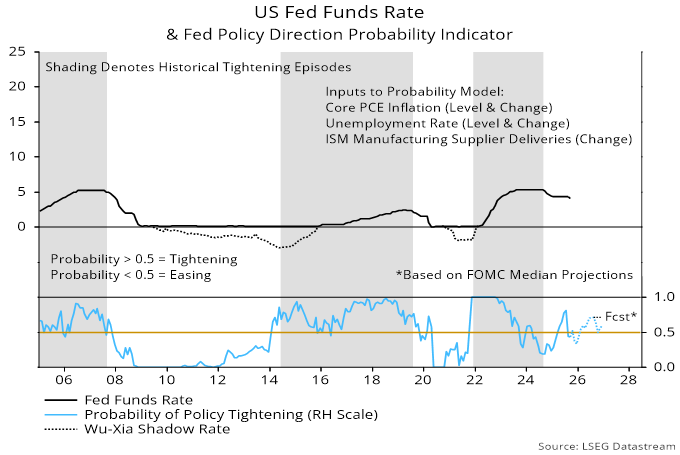

A simple model of the Fed’s historical behaviour suggests that the window for rate cuts will close in early 2026 if the economy evolves in line with the median FOMC forecast.

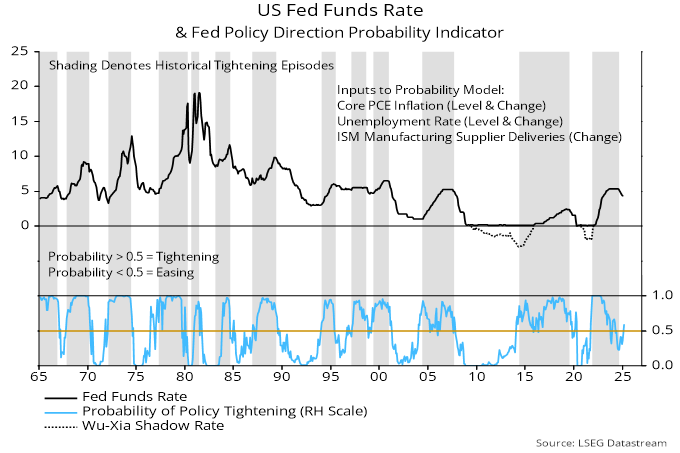

The model classifies the Fed as being in tightening or easing mode depending on whether a probability estimate is above or below 0.5. The estimate is based on currently reported and lagged values of core PCE inflation, the unemployment rate and the ISM manufacturing delivery delays indicator. Despite the small number of inputs, the model does a satisfactory job of “explaining” the Fed’s past actions*.

The probability estimate rose above 0.5 in March, confirming that the Fed was no longer in easing mode. It moved back below that level in August / September ahead of last week’s rate cut – see chart 1.

Chart 1

The September reading of 0.44 would also have been consistent with a hold, suggesting that easing was partly precautionary and / or influenced by Trump administration pressure.

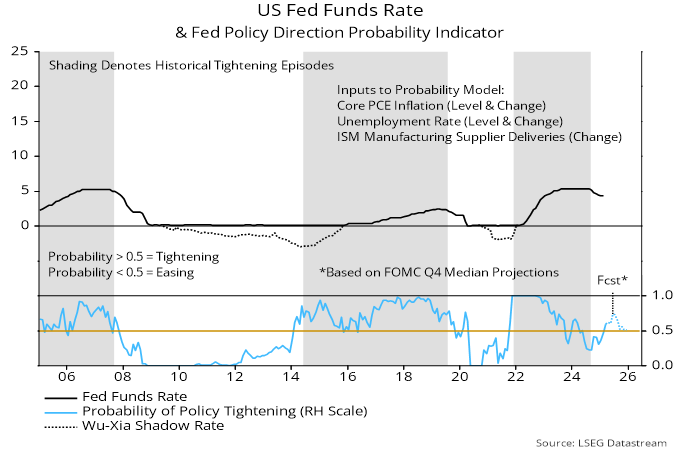

The median FOMC projections for 2026 have shifted hawkishly since June. Annual core PCE inflation is now 2.6% in Q4 2026 from 2.4% previously, while the unemployment rate declines from 4.5% to 4.4% between Q4 2025 and Q4 2026.

The model forecast shown in the chart is based on quarterly paths for core inflation and the jobless rate interpolated from the FOMC Q4 projections, along with an assumption that the ISM deliveries index stabilises at its August level.

The probability estimate edges back above 0.5 in October, returns to the easing zone over November-January but then embarks on a sustained rise above 0.5.

The shift into the tightening zone is unsurprising given the forecast of sustained above-target core inflation and a firming labour market.

The suggestion of a short window for further rate cuts is at odds with market expectations of an extended easing cycle. The market path presumably reflects a more dovish economic view but may also incorporate some probability of a change in the Fed’s reaction function under a new Chair.

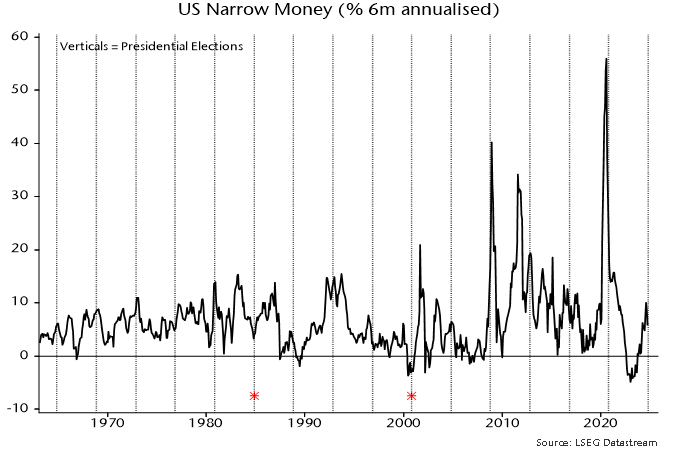

*A previous post contained a chart showing a 60-year history.