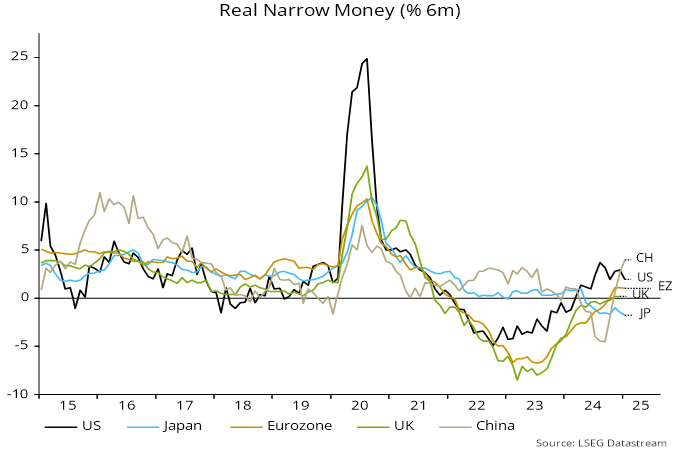

Eurozone and UK money trends have shown disappointingly small responses to policy easing, suggesting that rates remain in restrictive territory and casting doubt on hopes of stronger economic growth.

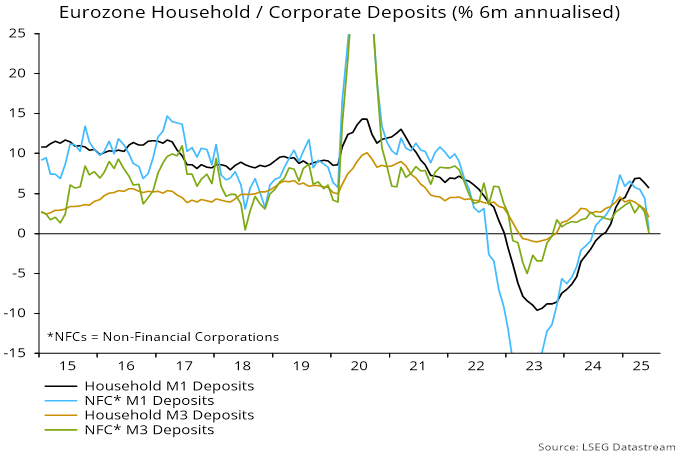

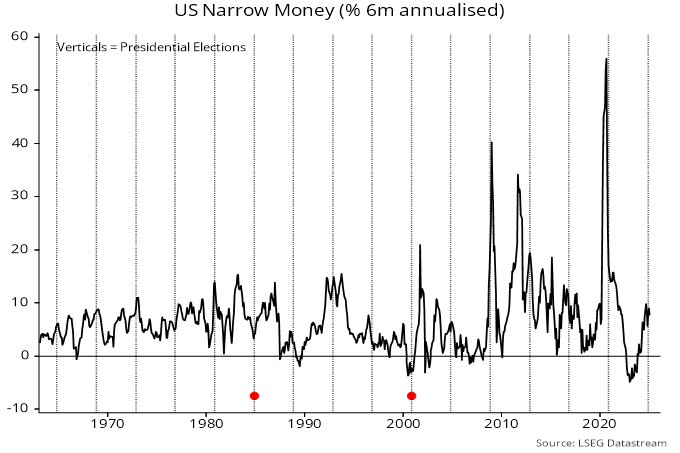

The preferred monetary aggregates here are “non-financial”, covering households and non-financial corporations. Money holdings of financial institutions are volatile and less informative about near-term economic prospects.

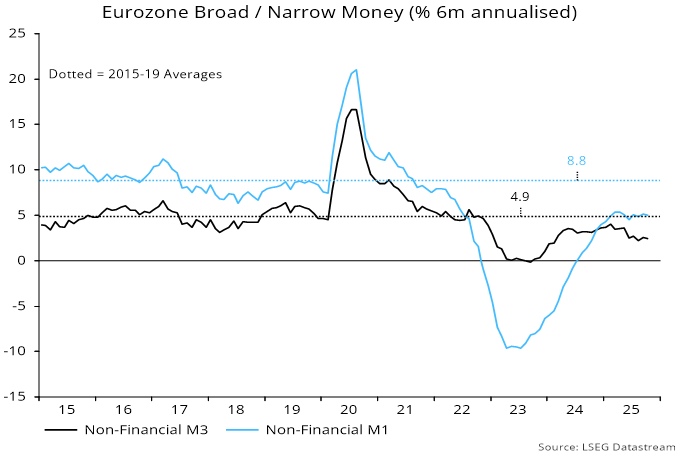

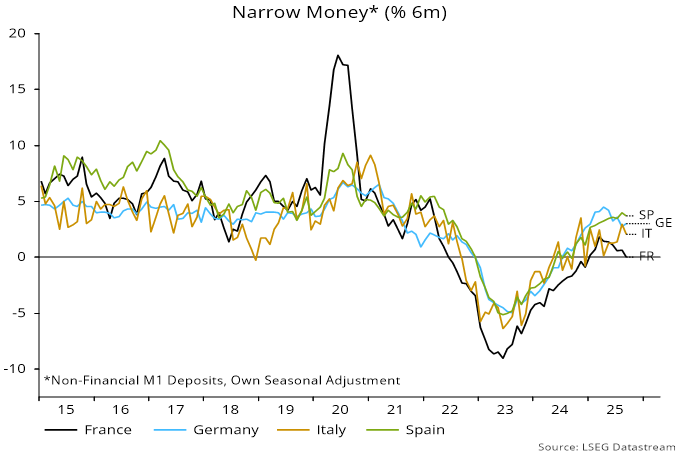

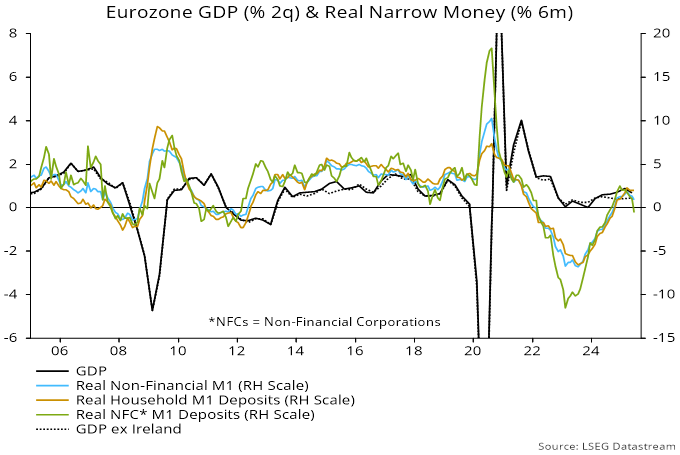

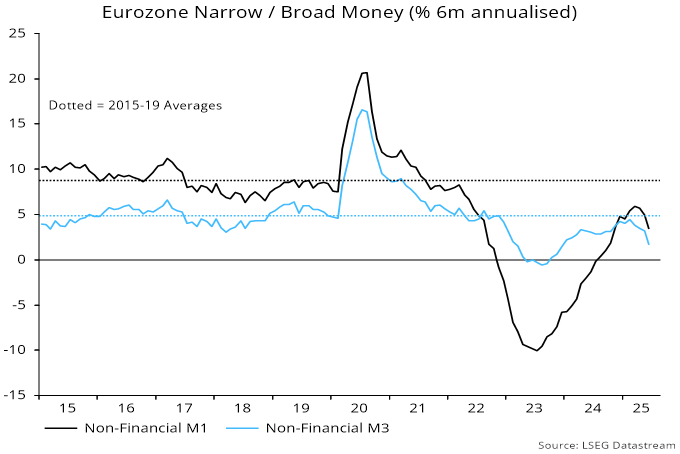

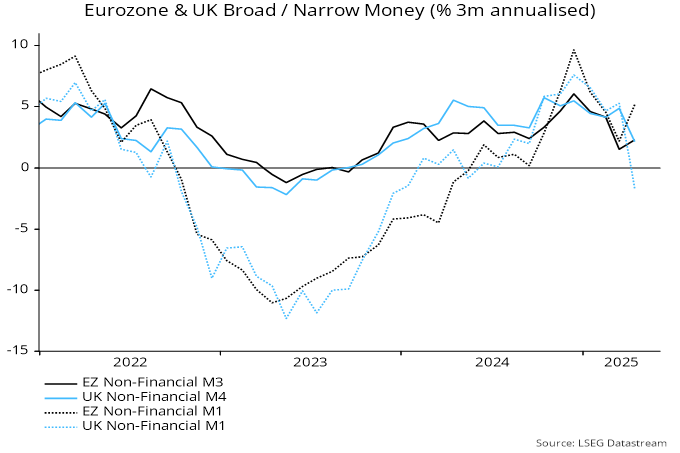

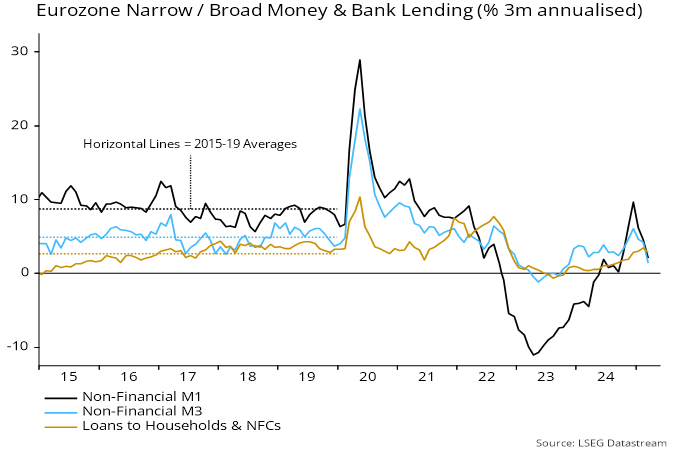

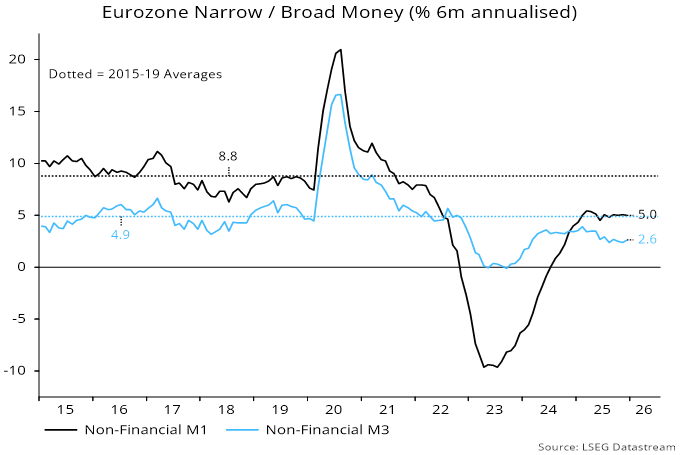

A recovery in six-month growth rates of Eurozone narrow and broad money stalled in early 2025 despite the ECB continuing to cut rates through June, with both well below pre-pandemic averages – see chart 1.

Chart 1

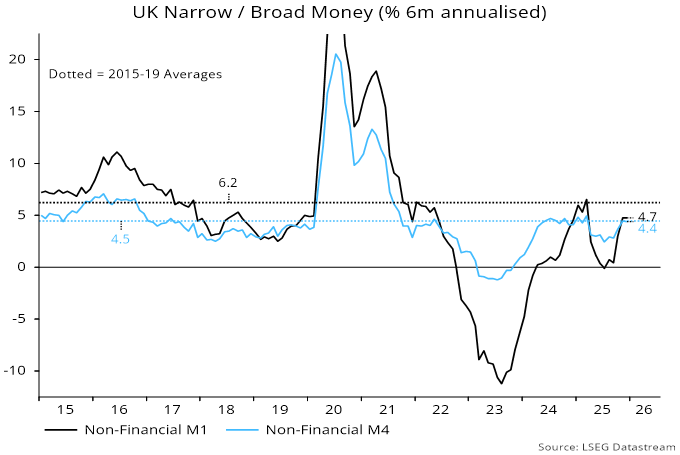

The UK profile is different. The laggardly pace of rate cuts appears to have contributed to a relapse in growth rates in H1 2025 but these recovered into November, moving sideways in December – chart 2.

Chart 2

While suggesting UK relative improvement, narrow money expansion remains beneath its pre-pandemic average (and the Eurozone level), with annual broad money growth a below-par 3.8% (versus 2.7% in the Eurozone).

One reason for the disappointing responses is that policy rate cuts have yet to translate into a decline in longer-term yields. Relatedly, UK QT has been a significant and unnecessary drag.

A hopeful scenario is that low inflation implied by weak broad money trends will allow longer-term yields to subside. Still, additional policy adjustment will likely also be required to generate a monetary response sufficient to warrant economic optimism.