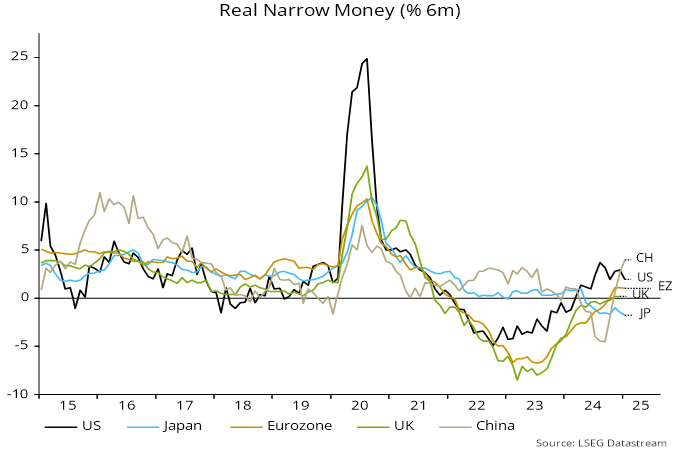

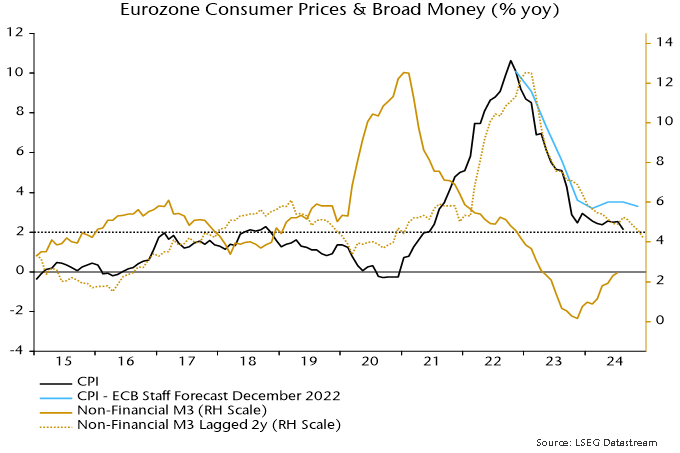

Eurozone / UK money growth has weakened despite rate cuts, suggesting that central banks – particularly the MPC – have more work to do to sustain economic expansion and prevent inflation undershoots.

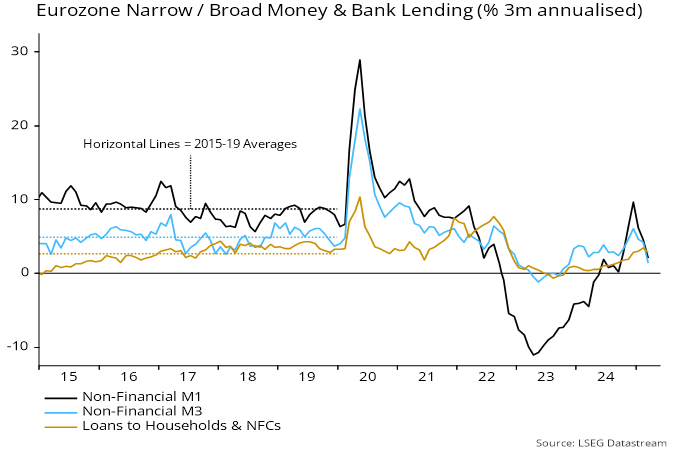

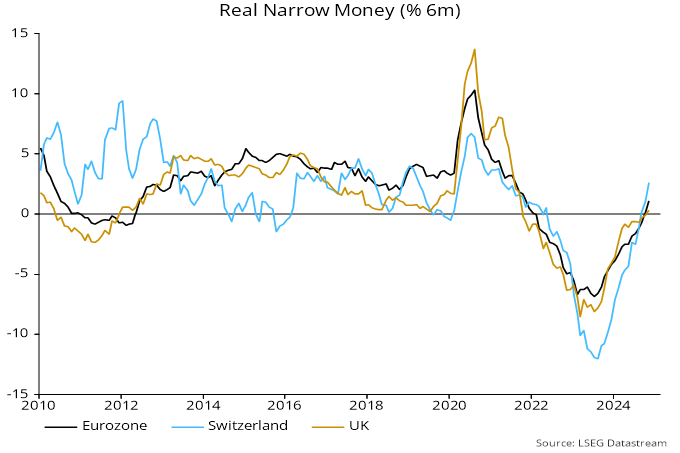

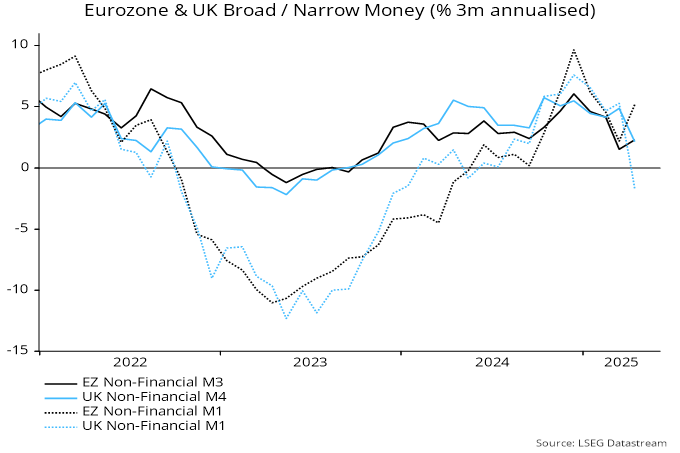

Preferred broad money aggregates – Eurozone non-financial M3 and UK non-financial M4 – grew by 2.3% and 2.1% annualised respectively in the three months to April, down from 4.6% and 4.4% in the prior three months – see chart 1.

Chart 1

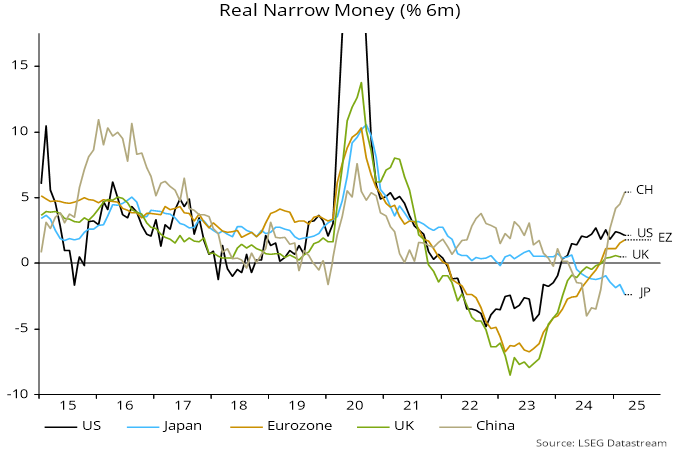

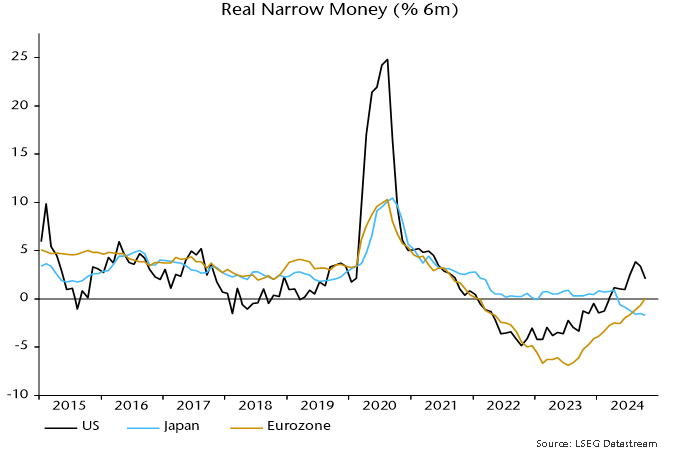

Concern about the Eurozone slowdown is tempered by still-respectable narrow money growth – non-financial M1 rose by 5.2% annualised between January and April versus 6.2% in the prior three months.

UK non-financial M1, by contrast, contracted by 1.7% annualised in the latest three months, following 6.5% growth in the three months to January.

The slump in UK momentum was driven by a month-on-month fall of 1.0% (not annualised) in April, mostly due to the household component. This may have been related to the end of the stamp duty holiday on 31 March – a bunching of transactions and mortgage borrowing ahead of the deadline may have been associated with a temporary rise in demand for sight deposits, which reversed in April as activity normalised.

An additional possibility is that individuals who sold assets in anticipation of tax rises in the October Budget delayed reinvesting the proceeds until the start of the 2025-26 tax year.

Household broad money rose by 0.2% in April despite the big fall in sight deposits, reflecting a record £14.0 billion inflow to cash ISAs.

Still, the movement of money out of current accounts is a negative signal for the economy, suggesting low spending intentions and a preference for saving.

UK corporate broad money, meanwhile, resumed a decline in the latest three months, suggesting that firms remain under financial pressure to cut jobs and investment.