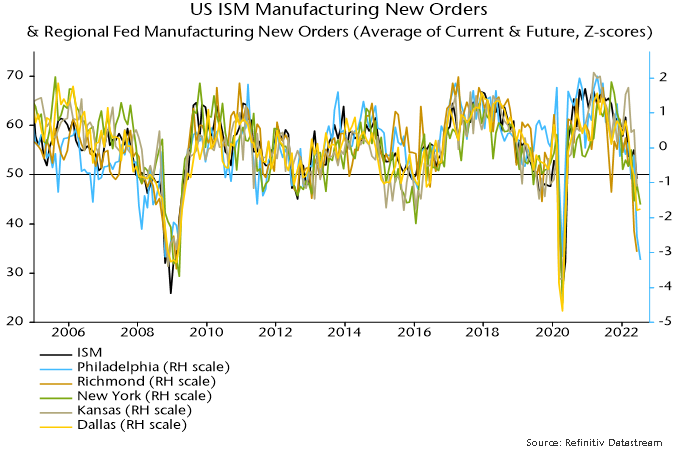

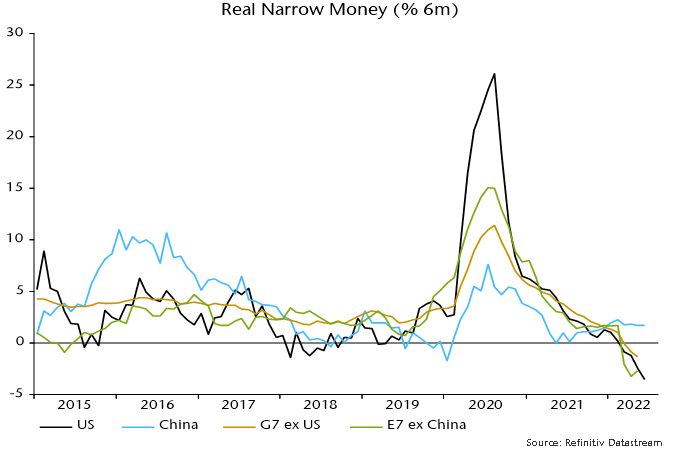

A fall in global six-month real narrow money momentum below zero in March signalled a shift in the economic outlook from slowdown to recession. A subsequent further decline in momentum to its weakest since 1980 suggests a deep recession extending into Q1 2023, at least. Economic contraction will release liquidity for markets, with “safe” bonds and quality stocks possible beneficiaries. Chinese real money momentum is diverging positively, supporting relative economic / equity market prospects.

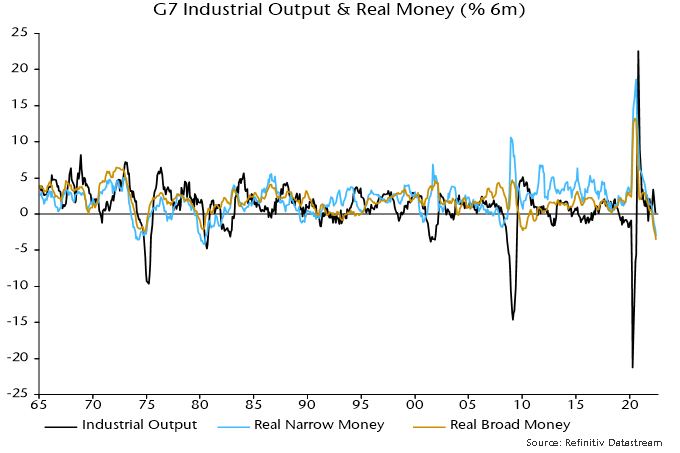

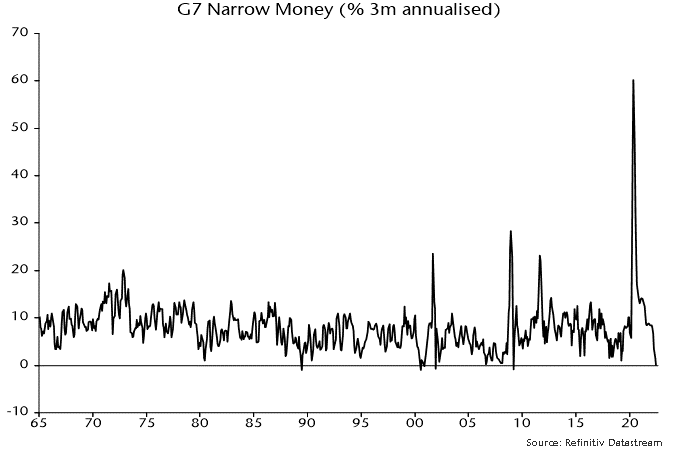

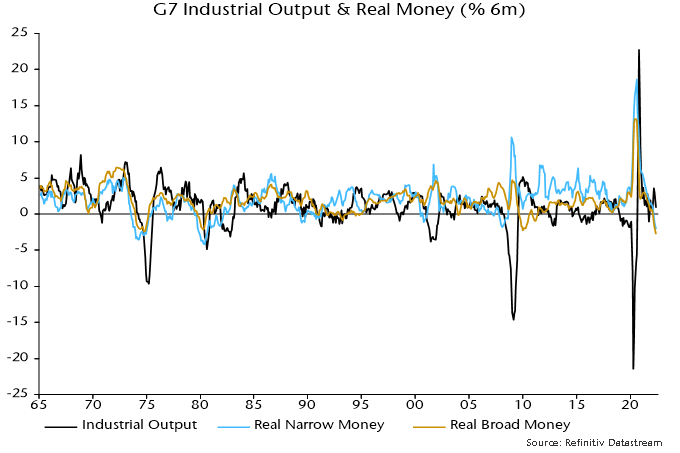

Global (i.e. G7 plus E7) six-month real narrow money momentum in May was below its GFC low and the weakest on record in data extending back to 1995. In longer-run G7-only data, the current rate of contraction was matched in 1973 and 1979 before severe recessions – see chart 1.

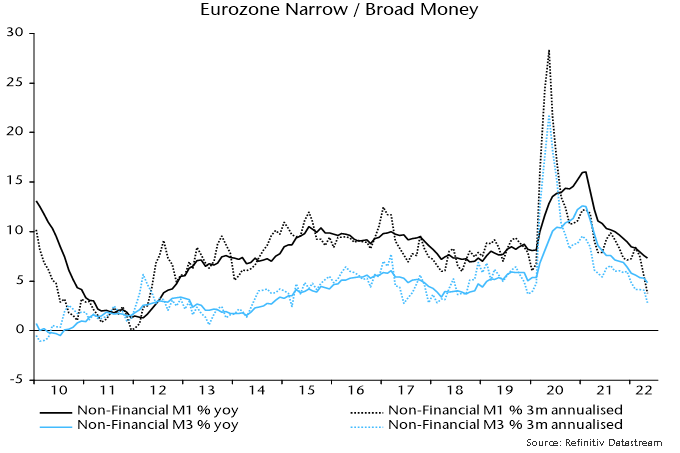

Chart 1

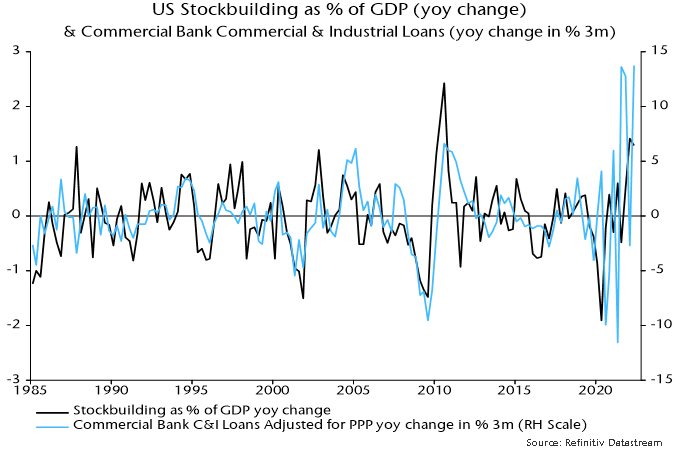

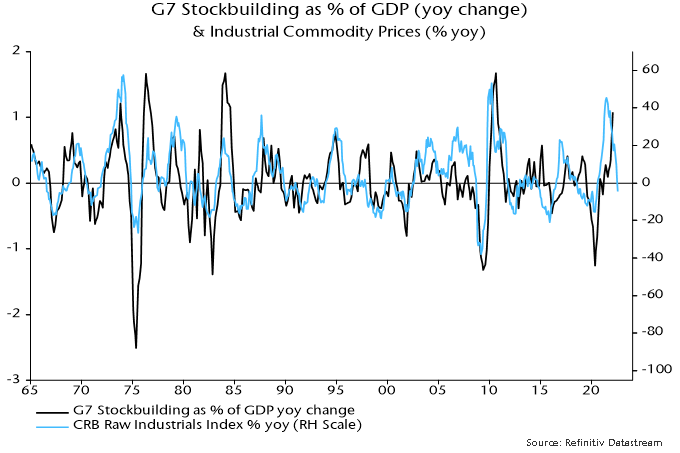

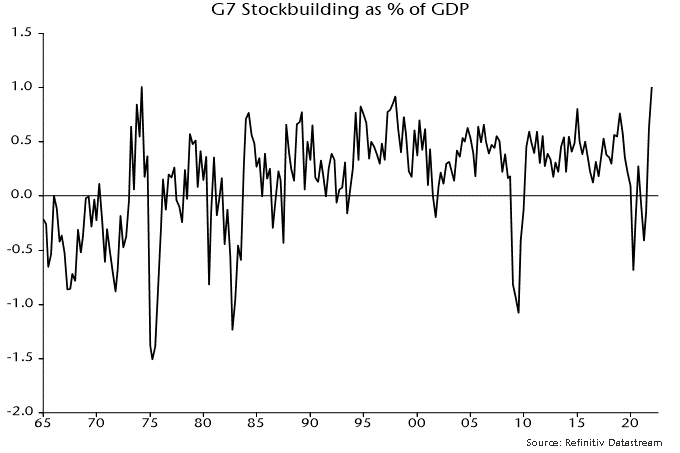

A further recessionary consideration is the recent pace of stockbuilding: the G7 stockbuilding share of GDP matched a 1974 high in Q1 – chart 2. The cycle upswing was supercharged by firms overordering inputs because of supply shortages. With final demand falling away, a liquidation of inventories will be amplified back through supply chains – the “bullwhip” effect.

Chart 2

The assessment of market prospects here is informed by two measures of global “excess” money: the gap between six-month real narrow money and industrial output momentum; and the deviation of 12-month real money momentum from a slow moving average. Both measures were negative by end-January, a condition historically associated with weak equity markets – table 1.

Table 1

The expected recession and a likely sharp fall in six-month consumer price momentum suggest that the first measure – the real money / output momentum gap – will return to positive territory in H2, possibly in Q3. The second measure may remain negative: 12-month real money momentum is currently far below its moving average and will be slower to recover. The implication is a possible shift from the bottom right quadrant in the table to top right – still an unfavourable backdrop for equities but less grim than during H1.

The excess money indicators are informative about sector and style performance. Recent outperformance of defensive sectors and underperformance of tech accords with the historical pattern under “double negative” readings – table 2. A switch to the upper right quadrant would suggest a tech recovery but further outperformance of defensive vs. non-tech cyclical sectors. Within the defensive basket, however, energy has historically performed poorly under this regime.

Table 2

Style-wise, recent outperformance of high dividend yield stocks accords with the historical pattern in the bottom right quadrant but quality has not on this occasion proved defensive, probably reflecting its inverse correlation with Treasury yields and the magnitude of the H1 rise in the latter – table 3. This suggests that quality will stage a come-back if yields reverse, with a potential shift to the upper right quadrant an additional positive – this was the best regime for quality and growth historically.

Table 3

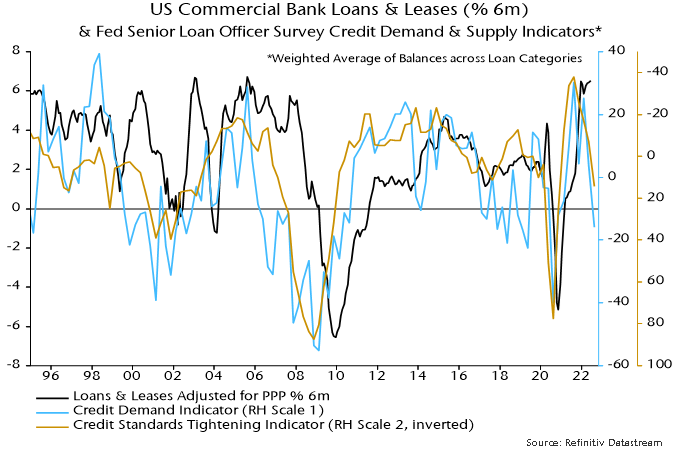

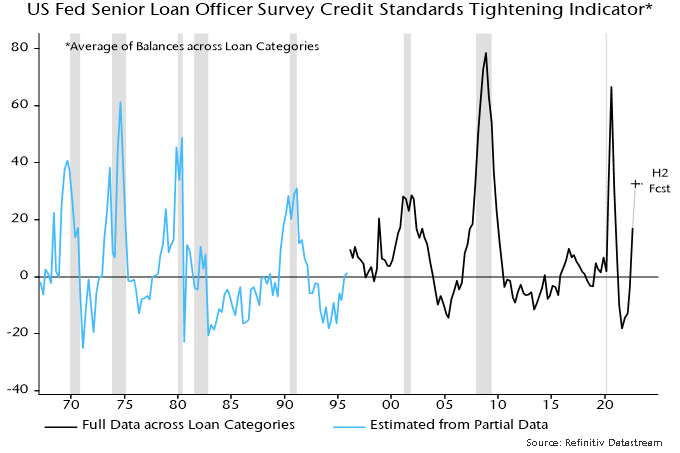

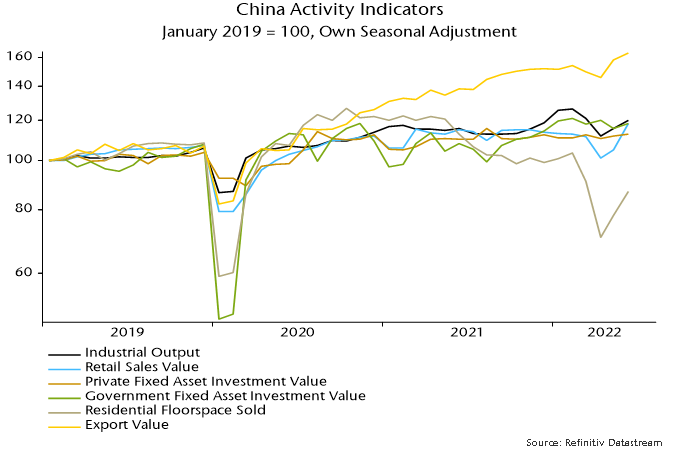

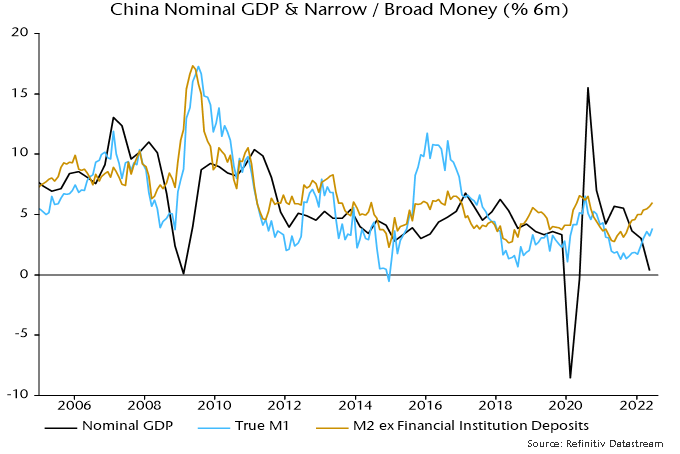

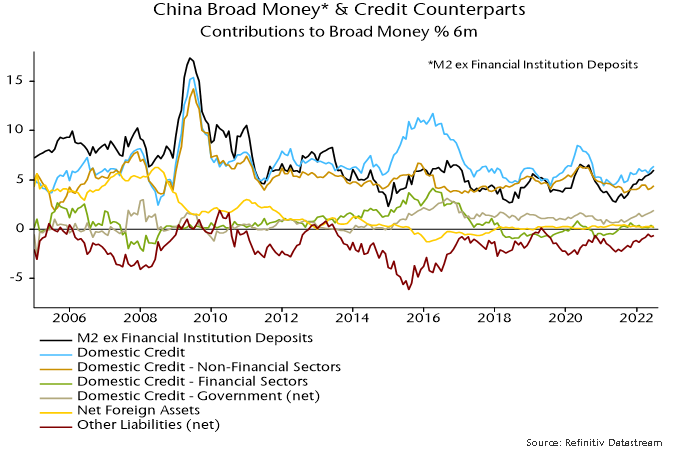

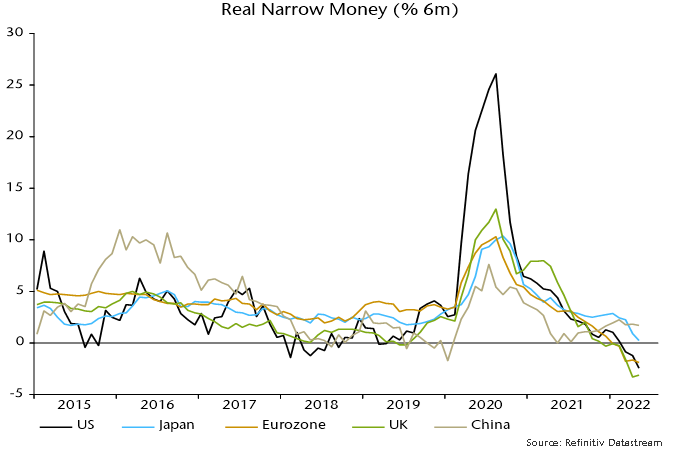

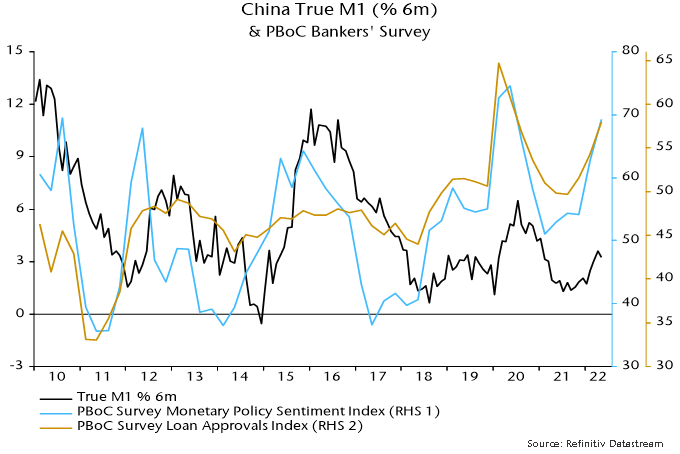

Six-month real narrow money momentum is similarly weak in the US and Europe but China and, to a lesser extent, Japan are diverging positively – chart 3. A further pick-up in China would support a forecast of economic recovery despite an export drag from recessions elsewhere. The latest PBoC bankers’ survey is consistent with monetary acceleration, indicating substantial policy easing and an increase in loan supply – chart 4.

Chart 3

Chart 4

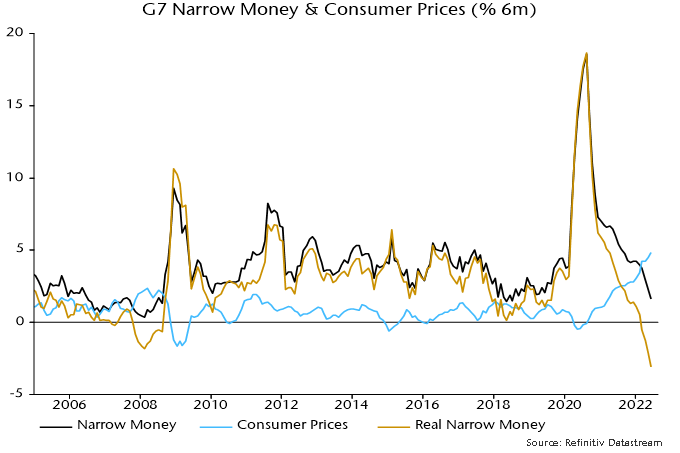

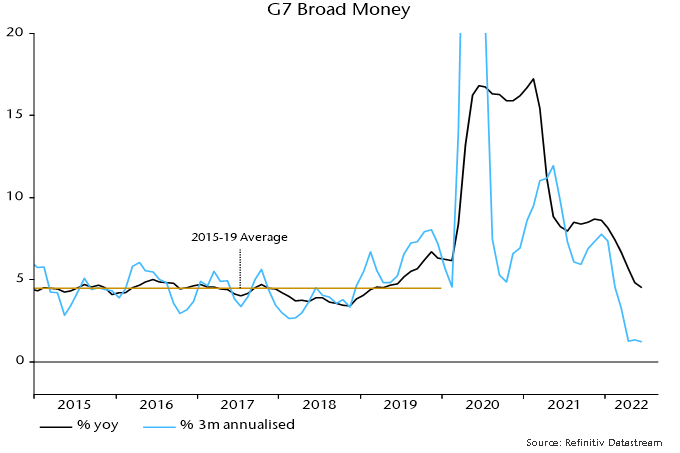

Global inflation prospects have improved dramatically. Having warned of the current overshoot, monetary trends are now consistent with inflation rates returning to target. G7 annual broad money growth was down to 4.9% in May from a peak 17.3% and is on course to move below its 2015-19 average of 4.5%: the money stock expanded at an annualised pace of only 1.3% in the latest three months.

The monetarist rule of thumb is that money growth leads inflation with a long and variable lag averaging two years. G7 annual broad money growth peaked in February 2021 so this average would suggest no inflation relief before early 2023. Some monetarist economists argue that the 2020-21 money growth surge has left a large monetary overhang, raising the possibility of a longer-than-average lag.

The view here is that the historical variability of the money growth / inflation lag partly reflects the position of the stockbuilding cycle, which is a key driver of commodity prices. The assessment that the cycle has peaked and will be in a strong downswing in H2 2022 suggests that recent commodity price weakness will be sustained, in which case their current large positive impact on annual CPI inflation rates will moderate through H2 and turn negative by early 2023.

Core inflation is widely expected to remain high into 2023, reflecting labour market tightness. Recession and monetary weakness, however, suggest that firms will lack pricing power to pass on increases in labour costs, which may, instead, squeeze historically generous margins and trigger early job cuts. Labour markets could weaken surprisingly sharply, with signs of an imminent unemployment reversal appearing recently in a range of sensitive indicators.