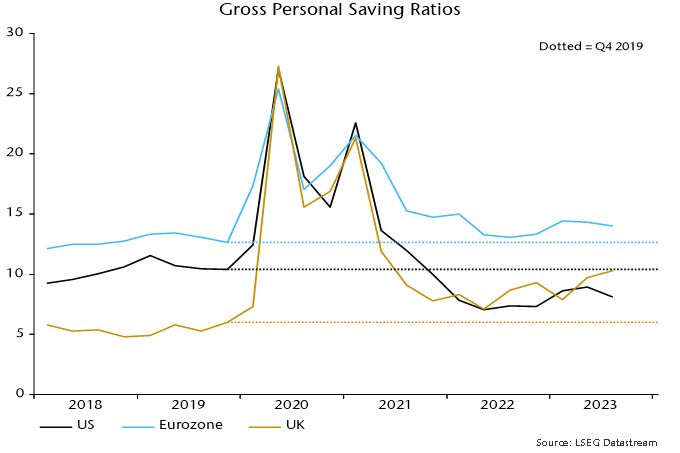

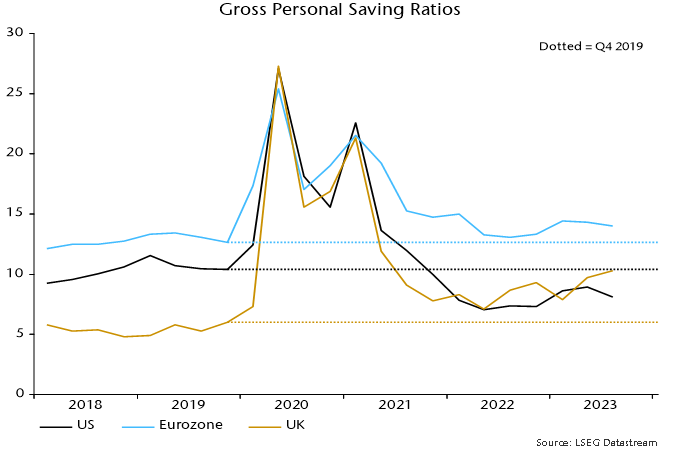

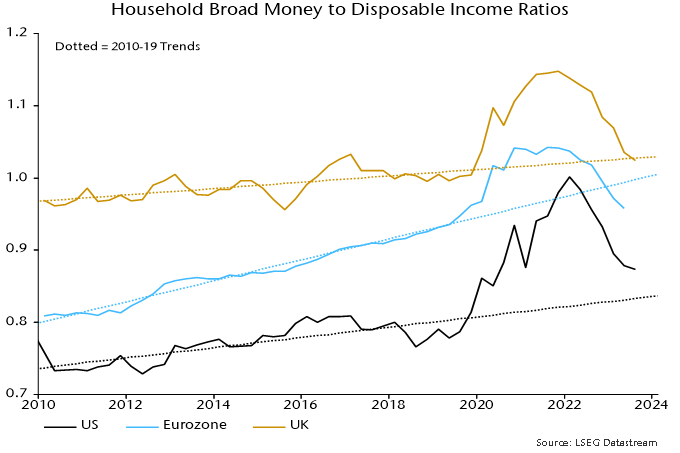

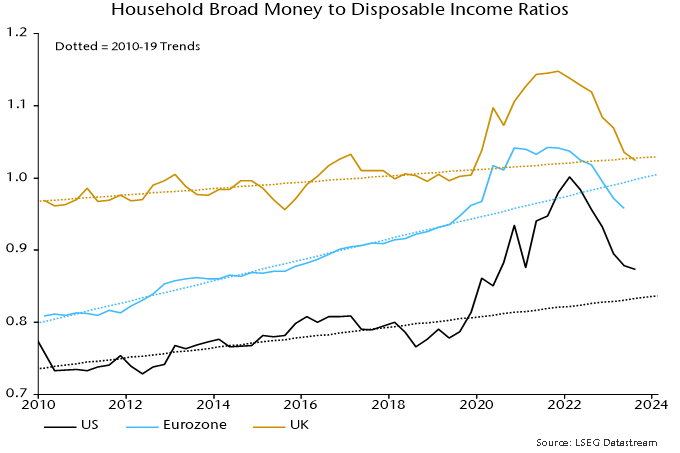

Elections and stocks: A surprising non-story

In a recent weekly update, we discussed how 2024 is an important election year worldwide. As it relates to US elections and stock returns, the data shows limited impact. Although markets can be volatile in election years, the political party in the White House has historically had minimal effect on returns. Since 1936, the 10-year annualized return of US stocks (as measured by the S&P 500 Index) at the start of an election year is 11.2% for a Democratic win and 10.5% for a Republican win. Sector performance, however, can be affected by short-term policy planning headlines.

Election rhetoric and the real story of healthcare stocks

For example, the healthcare sector often underperforms during a US election year due to the attention on drug and medical cost control. The global impact is significant, as the US is a major driver of healthcare economics. For 2024, the effect on healthcare may be less pronounced. The Biden administration’s measures for drug price control as part of the 2022 Inflation Reduction Act have already been implemented, but with only 10 high-profile drugs priced by the government under the reform, the economic impact has been muted. The pace of implementation could slow further under a Republican administration, potentially leading to positive earnings surprises.

Our Global portfolio includes a pure-play drug manufacturer, ANI Pharmaceuticals (ANIP:US), which owns a large facility in Minnesota where it produces a wide range of specialty and generic drugs and has a rapidly growing immune therapy franchise. None of its drugs have been targeted by US authorities for price negotiations.

From tariffs to technology

Recent protectionism, particularly new tariffs in sectors like semi equipment initiated during the Trump administration, may extend to medical devices and biotechnology. Don’t be alarmed if more are implemented. It’s our job to identify the tailwinds. Medical devices and biotechnology companies are likely to be the next tariff targets, especially those involving China. Over the past decade, Chinese productivity and quality have risen sharply in the fields of biotechnology, drug and device development.

Two proposed bills: the Biosecure Act and the Prohibiting Foreign Access to American Genetic Information Act of 2024 enjoy bipartisan support, with a 60% China tariff on healthcare goods proposed by Republicans in the event of their victory. This could create positive competitive tailwinds for North American and European contract drug manufacturers.

Evotec’s leap forward

Global Alpha owns Evotec SE (EVT:GR), a rapidly growing biological drug manufacturing contractor with technologies for low-cost and fast scaling of drug production. Evotec also has potential for numerous drug development partnerships and is developing a new stem cell medical device system for diabetes treatment.

Medical devices as the market’s quiet titans

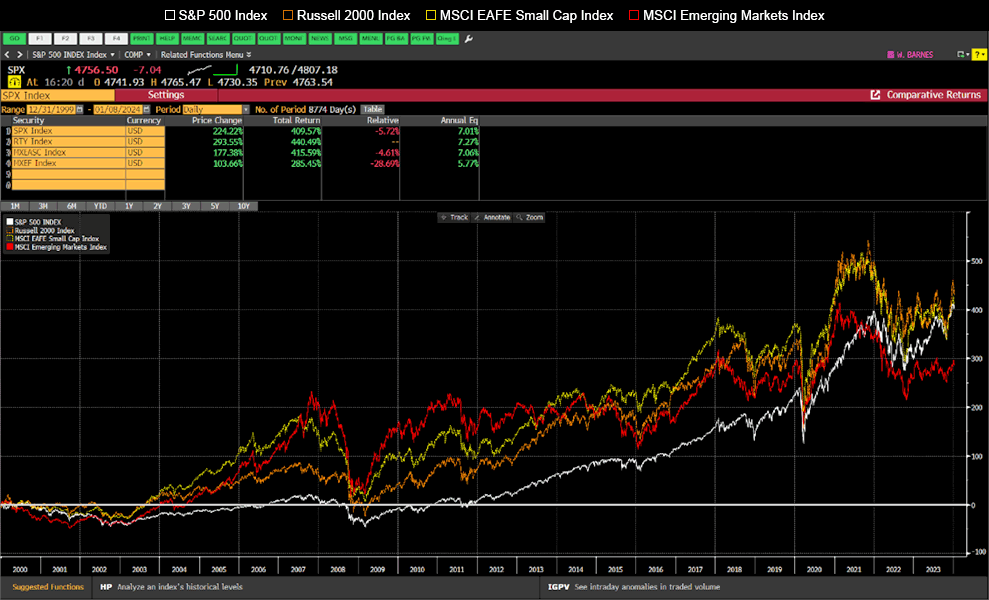

The medical device industry, known for its high barriers to entry and advanced technology, appears well-positioned for profitable growth. It tends to be less scrutinized by policymakers and therefore less affected by elections. In the last three decades, the industry has outpaced the S&P 500 by almost 15 percentage points, with stellar performance in the early 1990s, mid-2000s and late 2010s. Yet value creation has become more difficult in the past five years, especially for large, diversified companies. The top-30 largest medical device companies have underperformed the S&P 500 over one-, three- and five-year periods.

Our focus is on smaller, nimble names like Globus Medical Inc. (GMED:US), now an orthopedic powerhouse after acquiring its competitor, NuVasive. This acquisition has broadened its portfolio and enhanced its geographic reach. Globus’s expanded sales force will also support its fast-growing robotics business, a relatively new area. These robots improve the efficiency and output of orthopedic surgeons during back surgeries. Globus has also recently initiated a trauma product line that has successfully penetrated the market, further benefiting from its increased sales force. The orthopedic market is very large, valued at USD$72.3 billion and growing at a 5.3% rate.

Seeing clearly: The vision market’s rapid growth

Medical devices target a broad range of very large markets. For example, the global vision care market is projected to reach USD$192.85 billion by 2026, with a CAGR of 5.6%.

Global Alpha owns Menicon Co. Ltd. (7780:JT), Japan’s first and largest contact lens manufacturer, which now has a presence in over 80 countries. The company offers a comprehensive product lineup including disposables (daily, 2 weeks, 1 month, >3 months, silicone hydrogel), other soft contact lenses and RGP (Rigid Gas Permeable) lenses.

In China alone, myopia affects 146 million people. The condition is especially prevalent among children, creating a strong demand for corrective devices. Orthokeratology, a technique using contact lenses to reshape the cornea for long-lasting effects, had a global market value of $2.5 billion in 2023 and is expected to grow at a CAGR of 6.1% beyond 2026. Market penetration in China is only 2.0%. Menicon ranks as the second-leading company in this space.

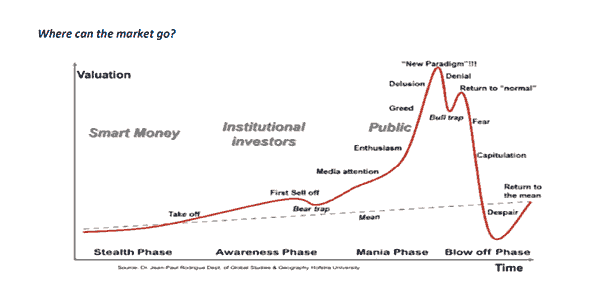

The true power of legislative winds

To sum up, it seems ineffective to predict the direction of the US stock market based on political party forecasting. However, it is important to monitor the progression of legislation from announcement through to funding and implementation. This is because bills go through phases of hype, disillusionment and reality, similar to many other events that can influence the economy.