MENA equity markets had a strong third quarter of 2024 with returns of 6.7% (for the S&P Pan Arabian Index Total Return) but trailed the MSCI Emerging Markets Index, which was up 7.8% in the same period. For the first nine months of 2024, MENA equity markets are up 5.4% compared to 14.4% for the MSCI EM Index.

Our team spent time in Saudi Arabia recently and came back feeling positive about the Kingdom’s medium-term prospects. The impact of the bold socioeconomic reforms that the country pursued in the last few years is visible not just in economic activity (and bad Riyadh traffic), but also in the sentiment expressed and captured in interactions we had with company executives, government officials, Uber drivers and hotel and restaurant staff. One can make the case that Saudi women have been the group that benefited the most from the country’s reform program. The elimination of the religious police establishment and lifting of the driving ban led to freedoms and mobility that Saudi women had not experienced before in their own country. This resulted in remarkable growth in their labour force participation, with data from the World Bank showing it had increased from 20% in 2018 to 35% in 2023. Much has been written about the changes that have been taking place in the Kingdom in the last few years, and we will not expand further on that here. However, we believe Saudi Arabia is in the early innings of a major societal and economic transformation project that will generate multi-year growth in profit pools in certain sectors like financial services, healthcare, education, entertainment, tourism, real estate and technology. Some of the profit pool growth will come at the expense of sectors that are not prioritized under the government’s Vision 2030 program or are not as geared to the evolution in consumer behaviour and evolving regulatory environment. These include brick and mortar retailers or companies that over-earned on government contracts, and which can be found in several sectors including construction and engineering.

Of course, not all is rosy in the Kingdom. While significant progress was made on diversifying the economy, nearly three quarters of the budget is still funded from oil revenue. If it stays, the current combination of low oil prices, production curtailment and high government spending is likely to weigh on growth or raise the risk of fiscal imbalances in the long term. The economic viability of some of the giga projects is difficult to determine and so poses additional capital allocation and fiscal risk. Positively, the country is preparing for this reality and has been actively diversifying its sources of funding from debt and equity capital markets. According to Fitch Ratings, Saudi Arabia was the largest US dollar debt issuer in emerging markets (ex-China) in 1H 2024. The listing of Saudi Aramco and the dividends that the government will receive from that will also continue to support the budget.

Additionally, inflationary pressures are building up in the system – specifically in Riyadh as demand- and supply-side factors collide in areas of housing and transport. This is resulting in downward pressure on household disposable incomes and is manifesting itself in downtrading and increased household debt. Unsurprisingly, many consumer companies are observing down trading in their revenue mix, and many are reacting through aggressive discounting to preserve market and wallet share. Consumers are embracing buy-now-pay-later financing to maintain or extend their purchasing power and this channel is becoming increasingly more prominent in the revenue of many consumer-facing businesses. Furthermore, consumer pressure in Saudi Arabia has the potential to delay further necessary reforms and regulations that can open new profit pools as the government looks to strike a balance between diversifying the economy and protecting consumer purchasing power.

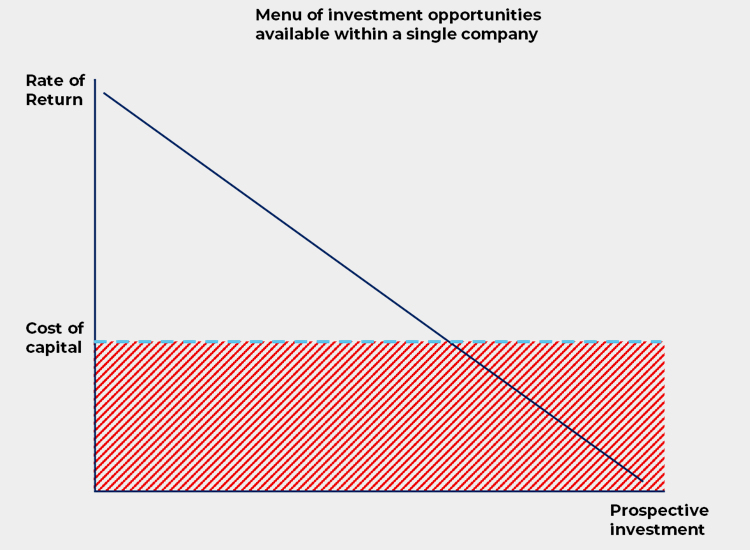

The strategy has had good success investing in Saudi Arabia from identifying growing profit pools early on and investing in companies that were best positioned to grow their share of them. Those include companies we have previously discussed in our letters such as Saudi Dairy & Foodstuff Co. (SADAFCO) in 2018, National Company for Learning and Education (NCLE) in 2019, and The Company for Cooperative Insurance (TAWUNIYA) in 2023. However, there are several challenges that have impeded our ability to express a fuller position in some of the sectors mentioned above. Firstly, we view the quality of certain companies in sectors like real estate and tourism as relatively poor and place some of those in the over-earners group we describe above. The other dynamic that has been increasingly challenging to navigate is the valuation environment, especially with regards to growth stocks. In the last two years, the market moved well ahead of earnings expectations, creating an unfavourable risk-reward set-up for companies the strategy owned and prospected. Using the MSCI Midcap Saudi Index to proxy growth companies in Saudi Arabia, we find that the price-to-earnings (P/E) ratio in 2023 was 38 times, more than double the 2022 levels and above levels we believe reflect cost of capital and growth dynamics on the majority of stocks in that index. Of course, we have made exceptions where we maintain ownership of a few high P/E ratio companies only when we believe their quality and growth potential justify such valuations. While we strongly believe in momentum as a factor for driving returns and outperformance, valuation is the ultimate determinant of our capital allocation reflexivity.

Fortunately, there are three factors working for the strategy at the moment. Firstly, there are growing profit pools resulting from reforms and demographics which is critical to our investing style – growth. Secondly, in the last two months, the market has begun the long-awaited process of recalibrating its expectations of earnings to levels that we deem realistic and interesting – reasonable valuations. Lastly, the strategy has already begun shifting the portfolio to areas where there is a healthy combination of growth, risk-reward and low investor positioning. One particular area where the strategy has been net buying in is the Saudi conventional banks, where we believe technical overhangs have largely suppressed price discovery year-to-date. The set-up for next year looks particularly attractive as those headwinds become less pronounced and bank earnings continue to compound.

We look forward to continuing to update you on the strategy in the next letter.